The Nuclear Renaissance

AI, electrification, and geopolitics are driving an unprecedented surge in power demand, forcing a global return to nuclear as the only scalable solution

Twice a week, I will release deep dives into stocks and sectors that fit into the three themes that I see winning in this age of tariffs and deglobalization: resilience, sovereignty & reshoring, China. I also dive into the opportunities in the AI data center value chain, Electrification, Healthcare, Software and many other themes and sectors.

Take advantage of this once in a generation opportunity to build long term wealth by investing in great stocks that will deliver returns for your portfolio for years to come.

Nuclear energy are at the intersection of many of the most important megatrends reshaping our world:

The electrification of the world (electricity going from 24% to 40% of our energy mix by 2040)

Reshoring & sovereignty (nuclear power being essential for energy sovereignty in an electrifying world with a nuclear renaissance being underway globally, nuclear power is essential for AI infrastructure to scale but requires the West to reshore the nuclear fuel value chain)

The AI revolution (AI and nuclear energy are more and more tied together every day as hyperscalers sign deals with nuclear utilities and AI drives the historical load growth inflection we are seeing)

The rise of China (China being by far the biggest growth driver in nuclear power).

Before this deep dive, I recommend reading some of omyur other write ups on the Electrification megatrend:

This deep dive will help you understand why we are just entering a nuclear renaissance, what is uranium, how it is turned into nuclear fuel, how it is priced, how the demand and supply outlook stack up, why the outlook is so bullish for this unique commodity, how to get exposure to uranium and the stocks to monitor as we enter this upcycle.

Discover one of the defining megatrends of our generation, the coming boom in electricity demand and grid investment supercycle, and how to play this decade long structural opportunity. This megatrend is completely intertwined with the AI data center buildout, making it crucial to understand Electrification.

The Age of Copper: Riding the Electrification, AI Data Center and Grid Investment Supercycles: Understand why copper is uniquely positioned at the heart of the electrification and AI data center supercycles, what is means for the metal’s price and how to get exposure to copper.

Understand how to invest in the $3-4tn AI Supercycle, a once in a lifetime investment opportunity.

Overview

The Nuclear Renaissance: The Collision of AI, The Age of Electrification, and Sovereignty

Nuclear 101: The Fuel Cycle & The Reactor

The Current State of Nuclear Energy

Phase I of the Renaissance: The AI Catalyst & The Monopoly of Time

Phase II of the Renaissance: Building the Future & The Rise of SMRs

Phase III of the Renaissance: The Holy Grail of Nuclear Fusion

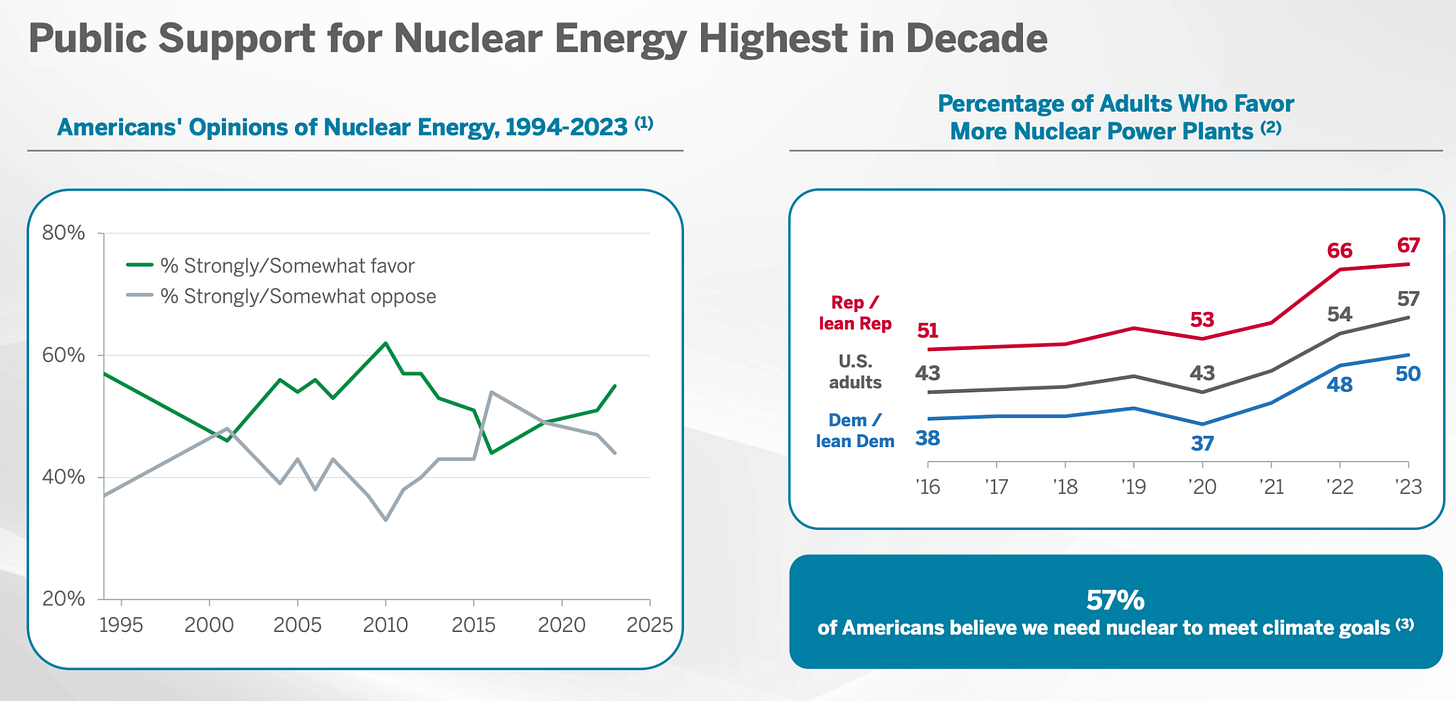

The Tension: Public Support, Nuclear Safety and Buildout Speed

The Bottlenecks & The Battle for the Electron

State Capitalism: The Government Steps In & The US vs China Race for Energy Supremacy

The Investment Playbook: How to Play the Nuclear Value Chain

Summary

Today, commercial nuclear energy, produced within a nuclear reactor, is powered by fission: the splitting of large uranium atoms into smaller ones. Currently, the US dominates nuclear energy production, maintaining the largest plant fleet. However, China is the driver behind new reactor construction.

We are entering a Nuclear Renaissance as a wall of electricity demand brought on by the AI revolution, coupled with growing electrification creates the perfect conditions for nuclear power. Compared with other energy sources, it offers reliable baseload power, a smaller carbon footprint, and a higher energy return on investment.

This deep dive into nuclear energy explores: Why we are entering a Nuclear Renaissance. What is nuclear energy? The current state of nuclear power production. The three phases of the Nuclear Renaissance. The bottlenecks. The return of state capitalism and the race for energy supremacy between the US and China. How investors can play the nuclear value chain.

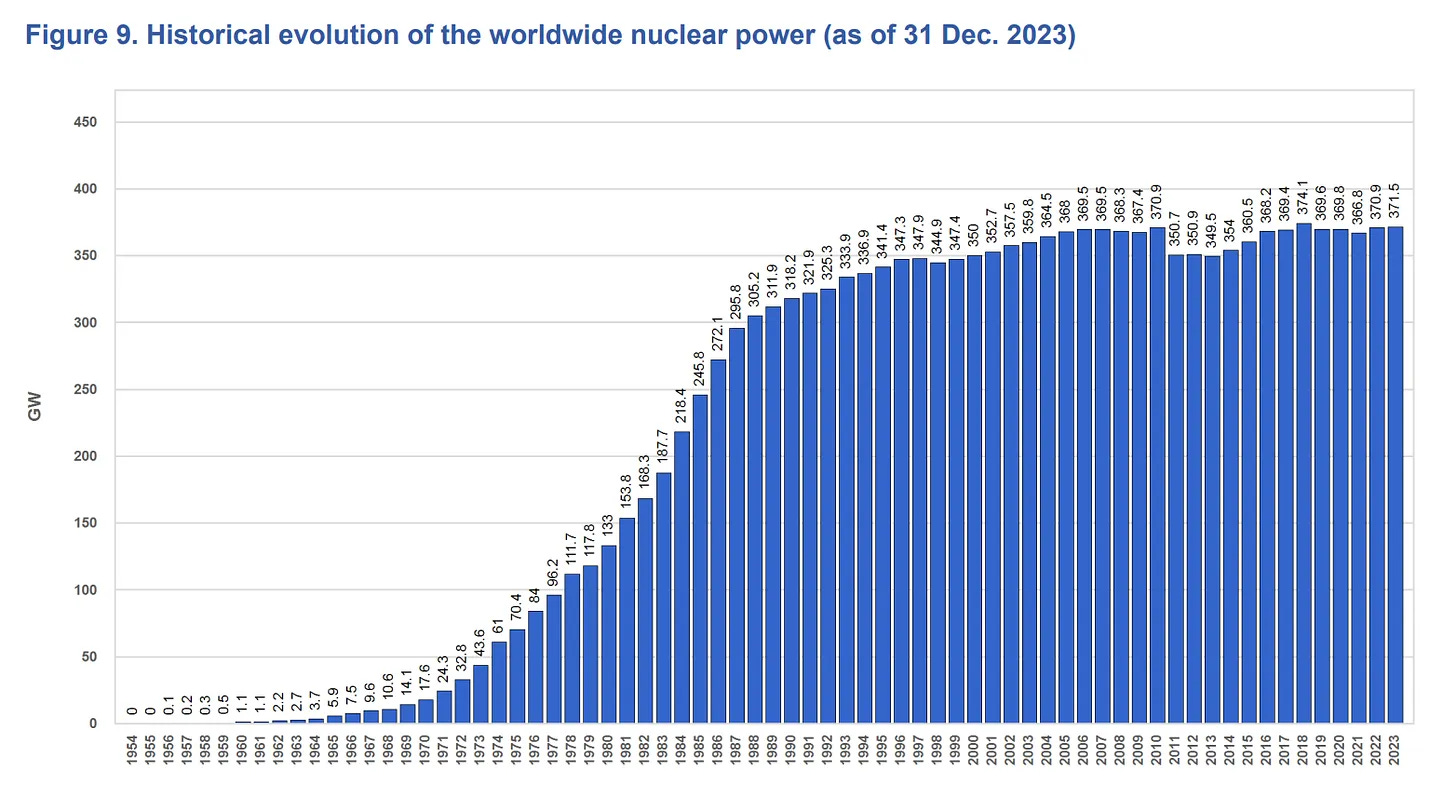

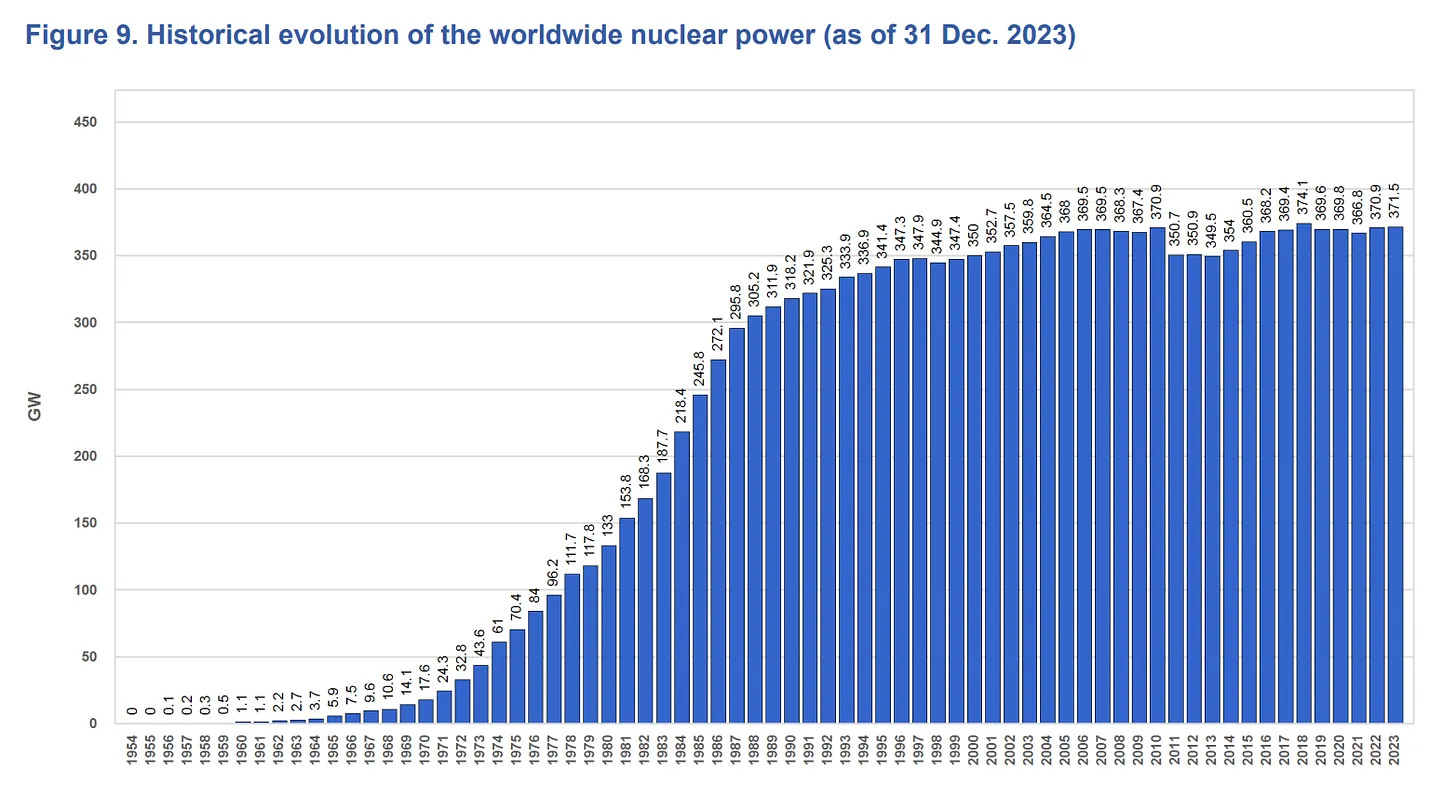

A Nuclear Renaissance: In the last few months, driven by AI data center needs for clean dispatchable power, the world has seen a slew of announcements for nuclear power in the US and many other countries across the world. IEA estimates for installed nuclear long term have increased by 40% in the last 5 years. The US alone is now targeting 400GW of nuclear power by 2050, India 100 GW by 2047 (for reference, the total global installed base of nuclear power at present is 420 GW).

1. The Nuclear Renaissance: The Collision of AI, The Age of Electrification, and Sovereignty

Power demand and prices in the US are rising and fast

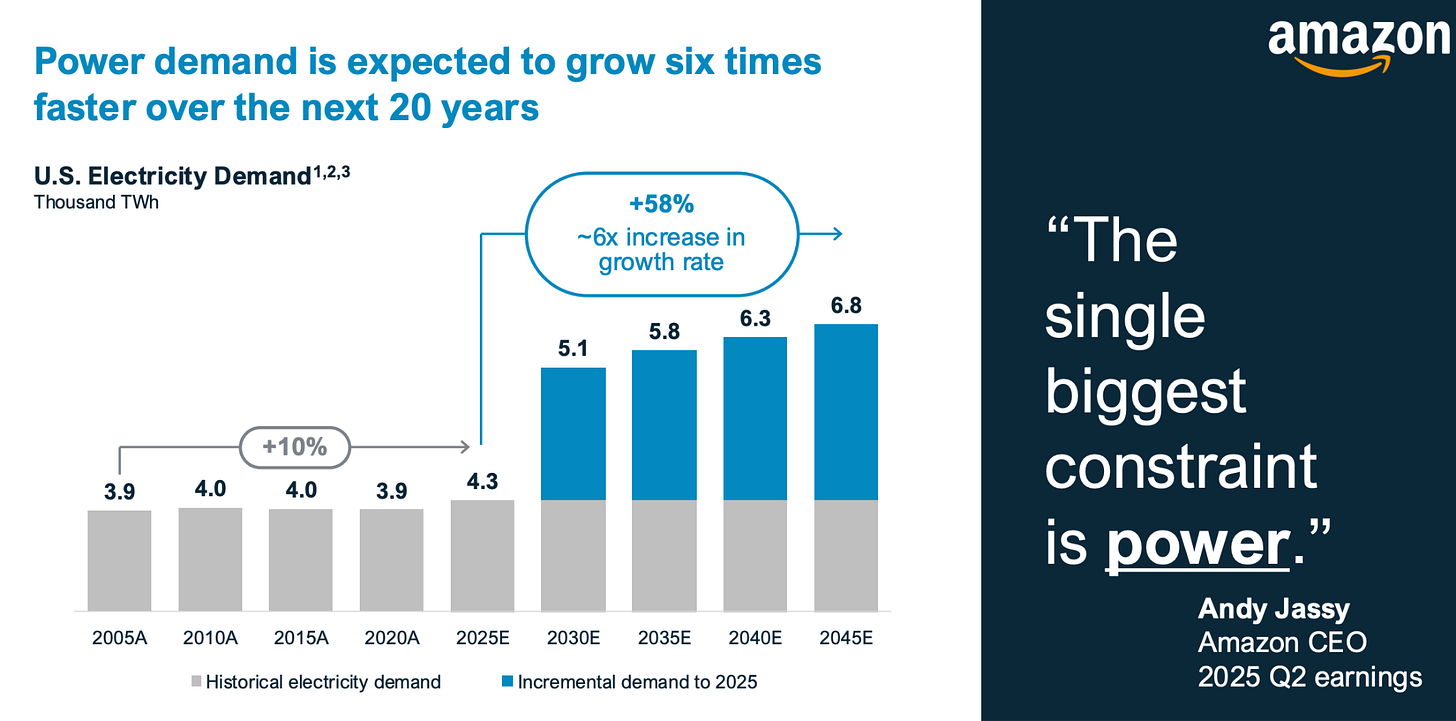

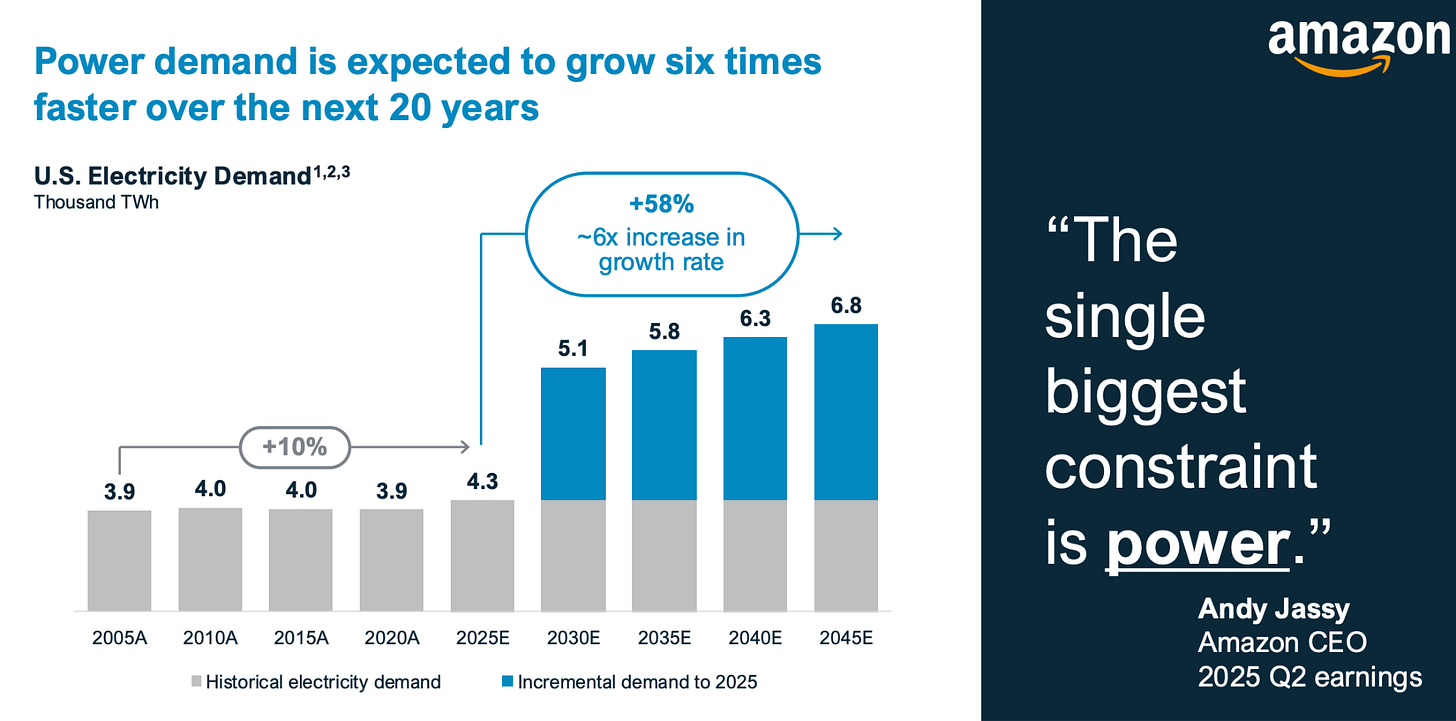

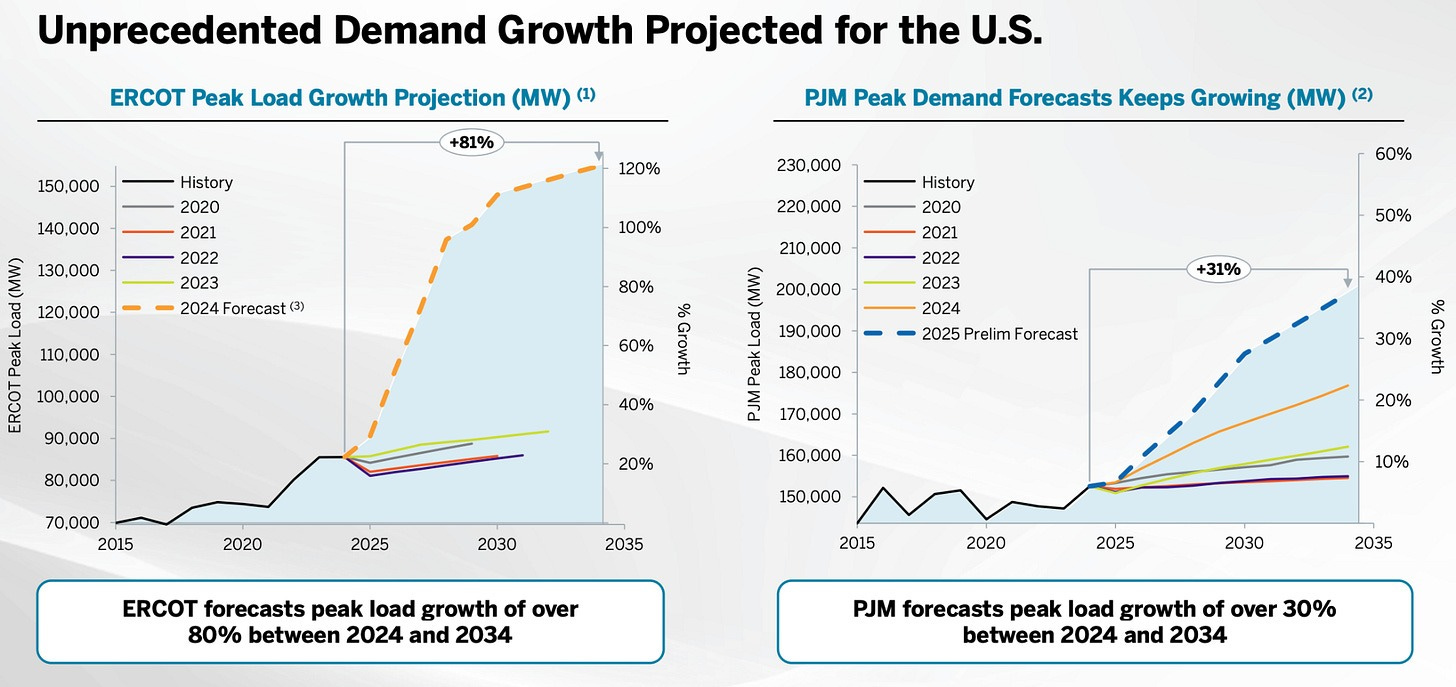

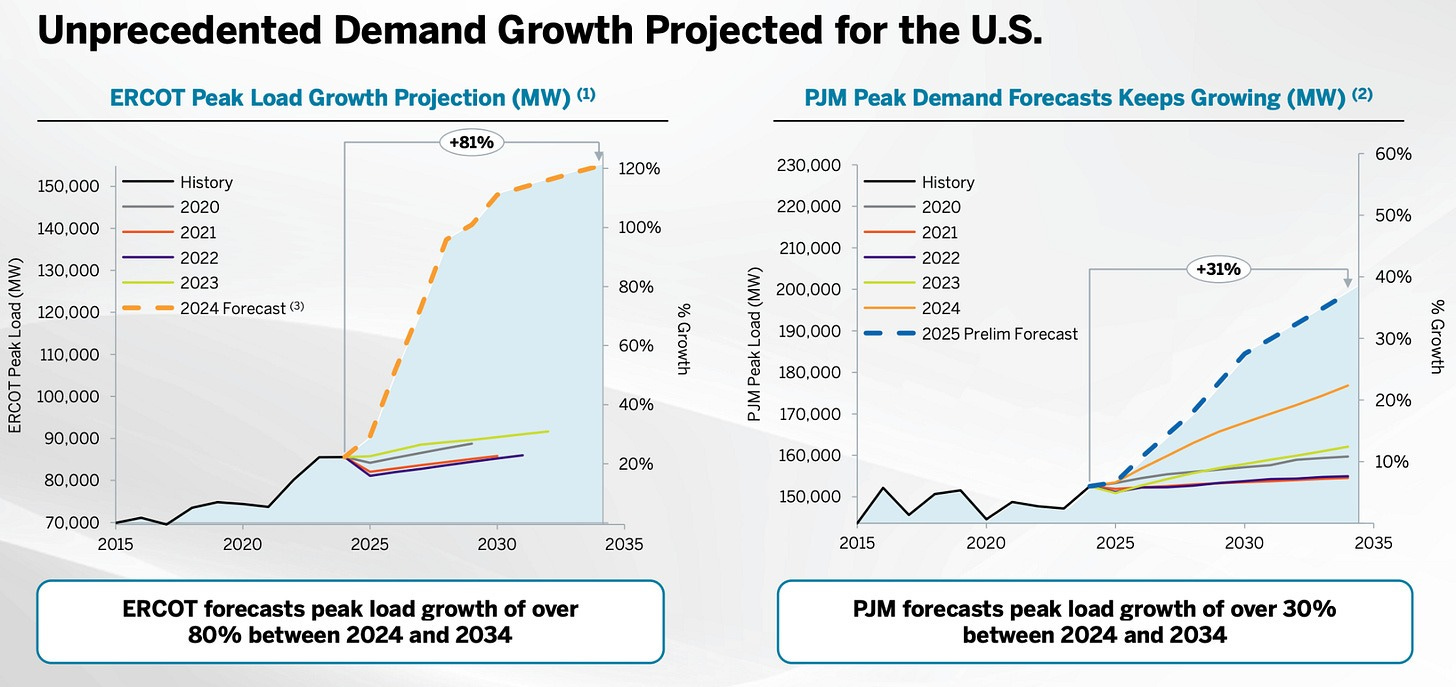

Electricity demand in the US is rising 6x faster than before (from 4,300 TWh in 2025 to 6,800 TWh in 2045): According to the IEA, US annual electricity consumption will increase between 2025 and 2026 (around 4,400 TWh), surpassing the all-time high reached in 2024, going towards 5,600 TWh by 2032. After relatively flat electricity demand between 2005-2020, EIA points to +1.7% 2020-2026 US electricity consumption growth, largely stemming from growth in the commercial sector, which includes data centers, and the industrial sector, which includes manufacturing reshoring. The DOE’s September 2024 Advanced Nuclear report notes that US electricity demand could more than double by 2050 from 4,000 TWh in 2025 to >8,000 TWh in 2050.

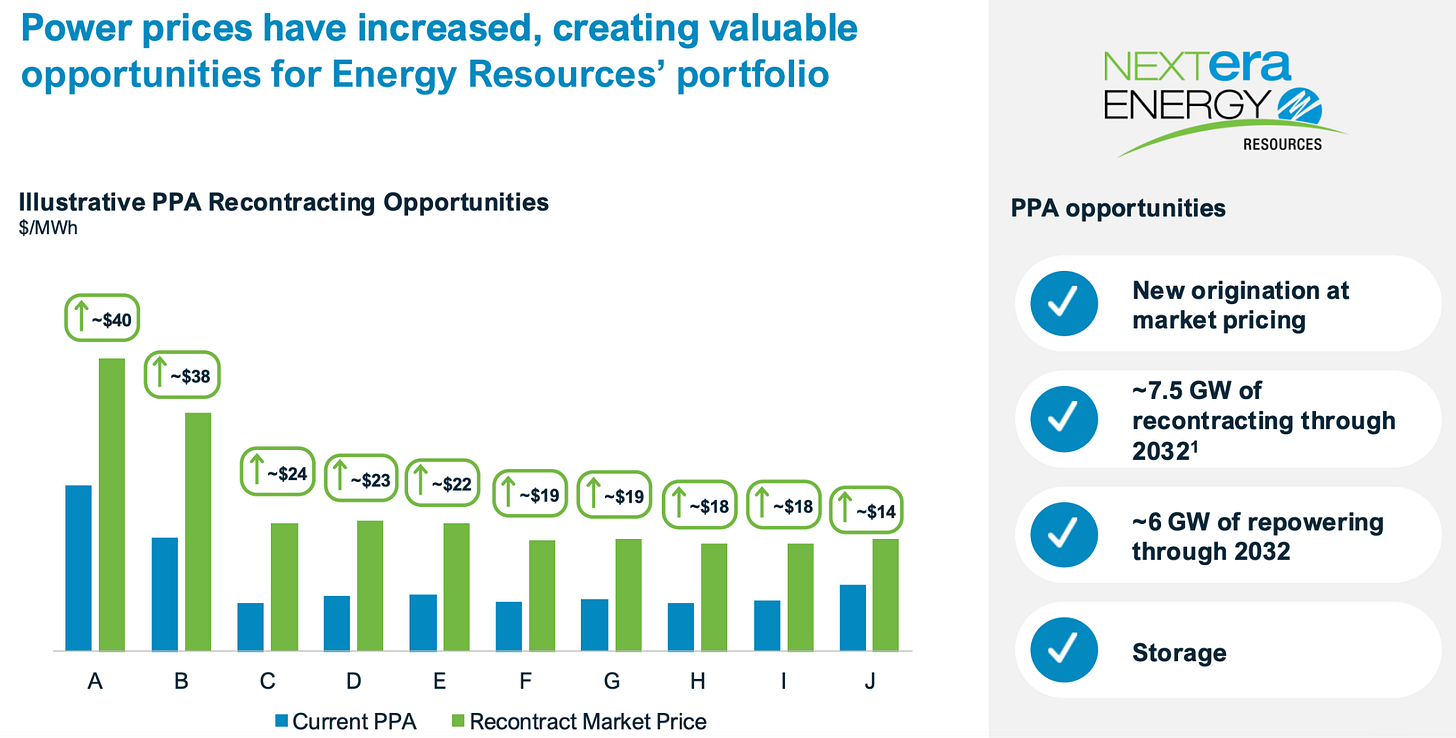

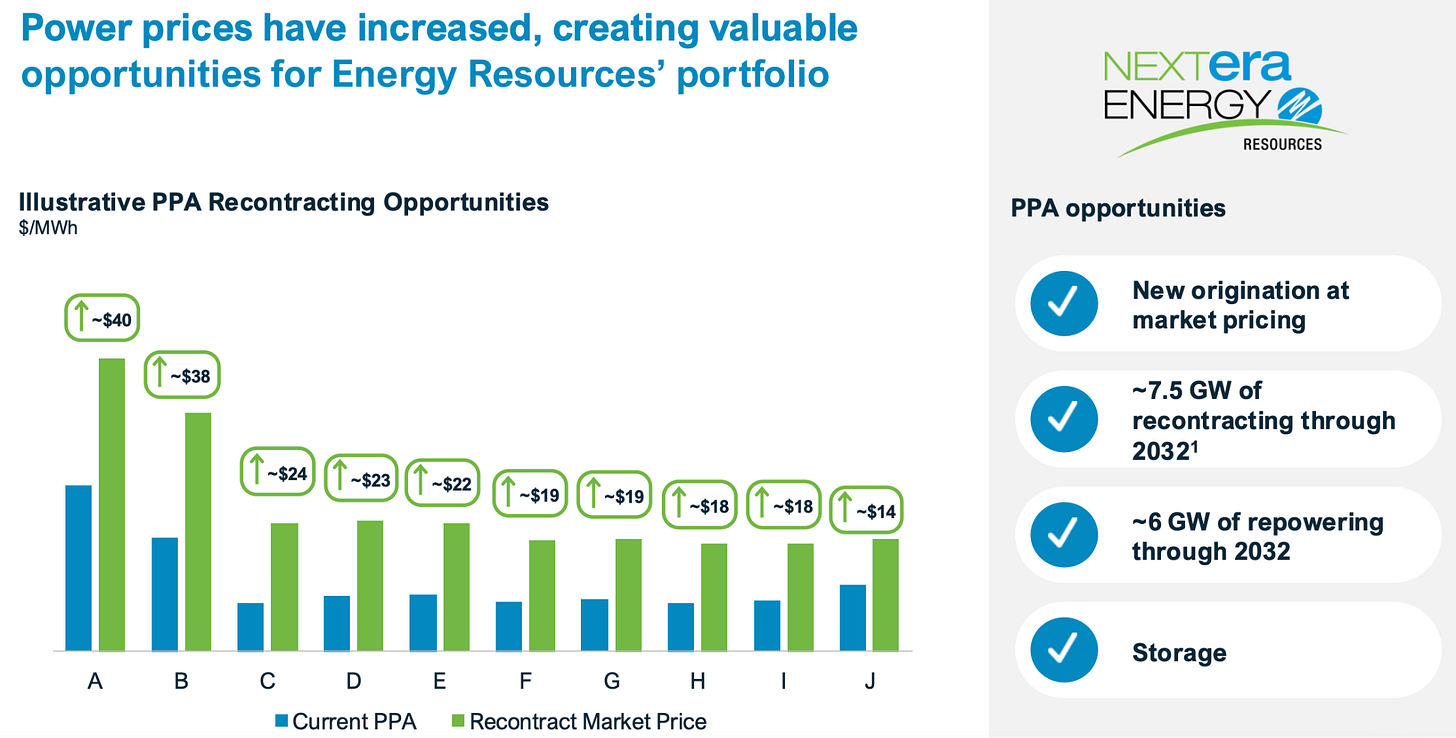

Power prices are moving up and fleet utilization is increasing: In recent years U.S. electricity prices, especially wholesale power prices, have moved higher as demand has resumed and structural supply constraints have emerged. After a period of relatively modest prices in 2023-24, the U.S. Energy Information Administration (EIA) projected average wholesale power prices of around $40/MWh for 2025, up roughly 7% year-over-year, with notable regional variation from about $30/MWh in parts of Texas (ERCOT) to $55/MWh in regions like New England and the Northwest. This year, PJM West and East 2026 ATC power prices have risen $6/MWh, with 2027 ATC power prices up $4/MWh. While 2026 ATC ERCOT prices have landed relatively flat, in part given weather headwinds and data center interconnection delays, 2027 ATC prices have remained resilient, stepping up $5/MWh. Electricity prices are seeing an upward as load growth becomes increasingly reflected in the curves. PJM projects net energy load growth to average 4.8% annually over the next 10-year period, and 2.9% over the next 20 years. ERCOT forecasts 145GW of peak summer load by 2031, representing a 59GW increase versus the 85GW forecasted 2025 levels. While CCGTs offer a long-term solution for rising energy needs, generator commentary has pointed to batteries and higher peaker utilization as key tools to solve the current situation through shaving demand peaks, though more energy will be needed to fix the upcoming supply/demand gap.

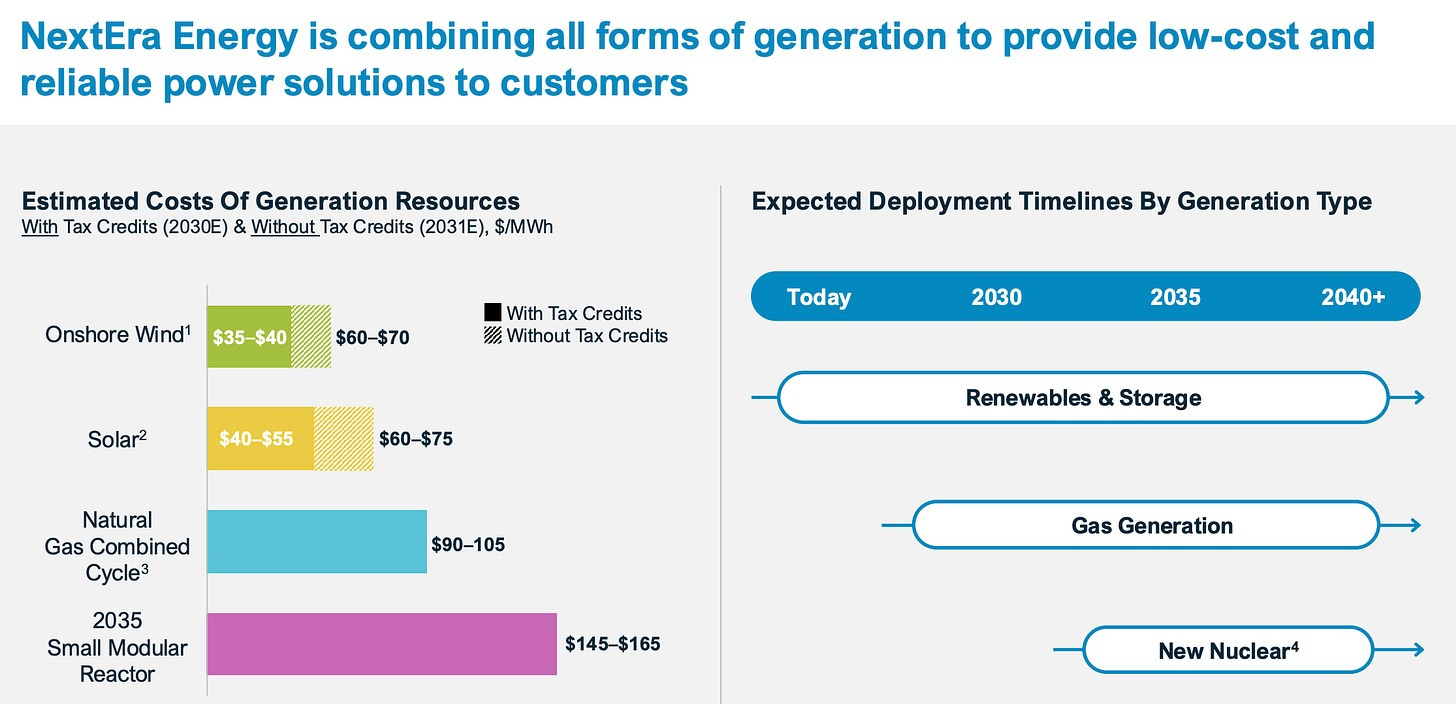

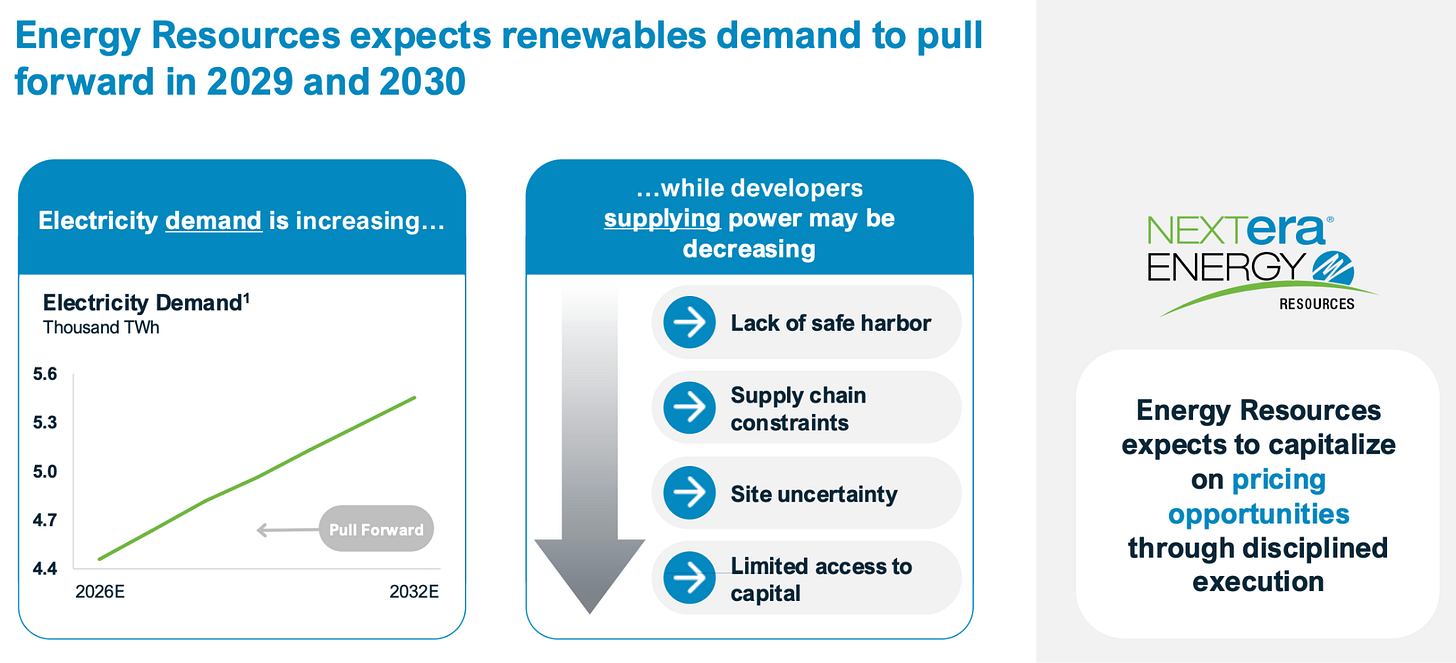

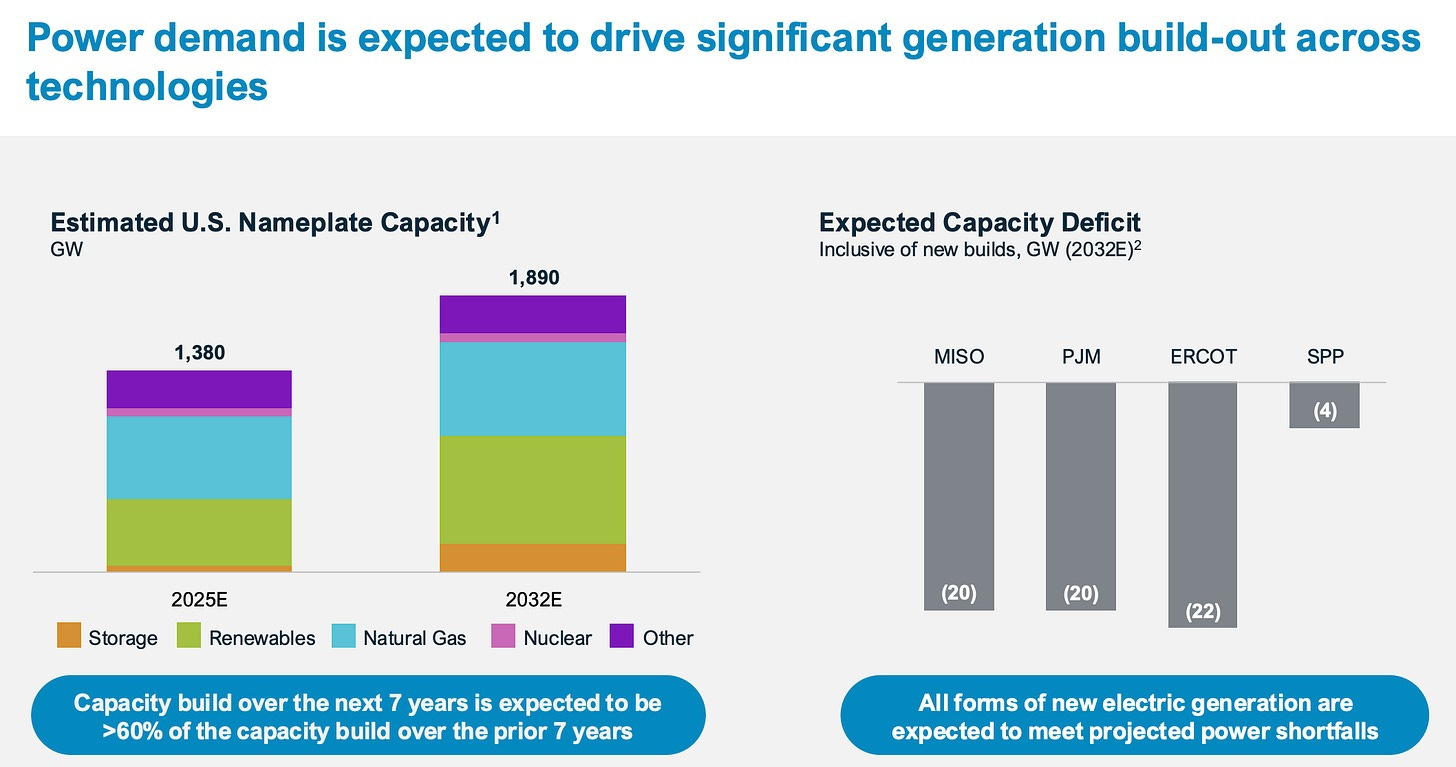

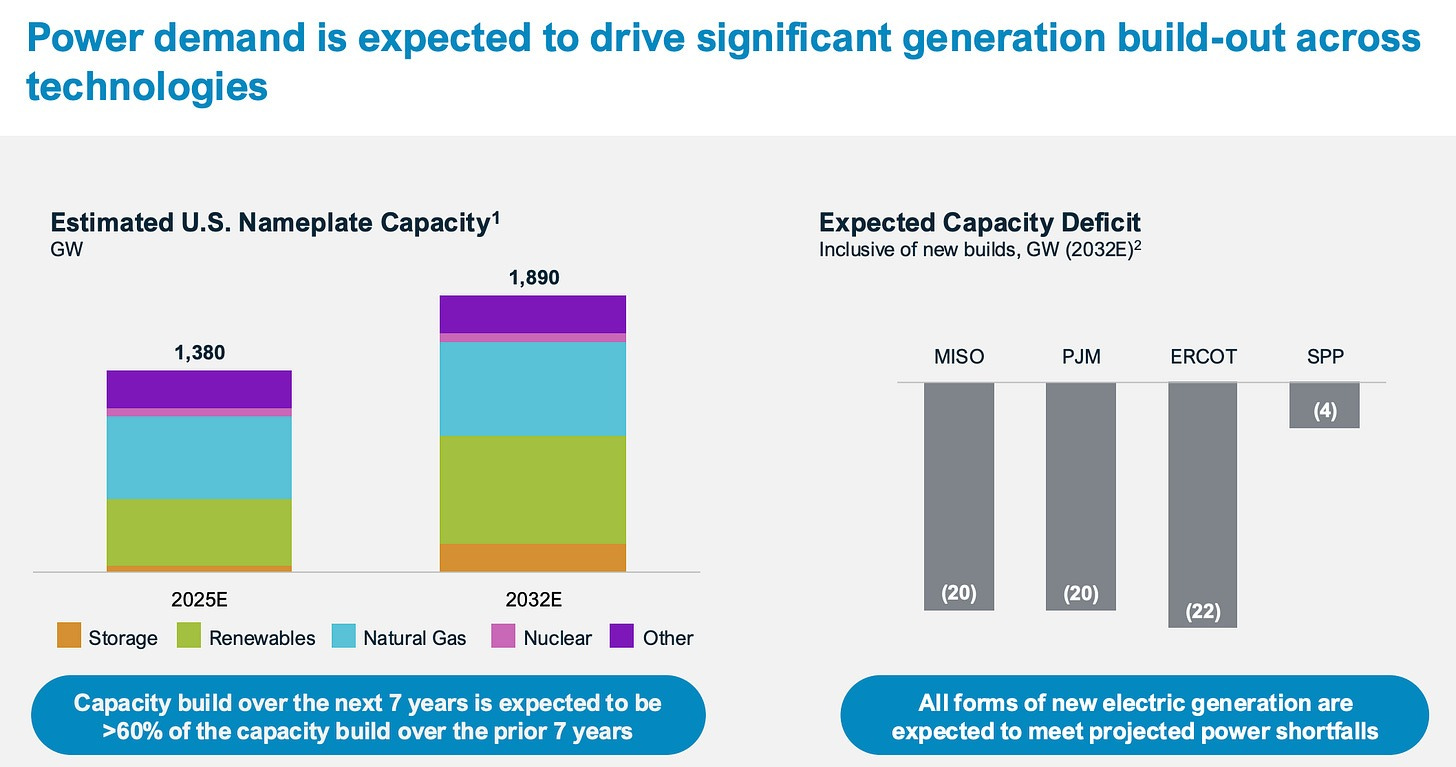

Looking forward, structural growth drivers such as AI data center build-outs, electrification of transport and industry, and reshoring of manufacturing are expected to sustain upward pressure on both wholesale and retail electricity prices. This demand surge could require an additional 500 GW (from 1,380 GW in 2025 to 1,890 GW in 2032) in generation capacity by 2032, which explains why every technology needs to be scaled up. As demand for power grows faster than new capacity and transmission infrastructure can be built, this environment should create optional repricing tailwinds for long-term power purchase agreements (PPAs). For a company like Nextera Energy with a vast generation and contracted sales portfolio, higher underlying market prices enhance the potential to renegotiate contracts or capture incremental value through rate mechanisms and large-load tariffs, especially where contracts reset in tighter markets.

The collision of AI, the Age of Electrification and Sovereignty

For decades, the technology and energy sectors existed in parallel universes with little overlap. For the tech giants of the world, energy was simply a passive operating expense (opex) on a P&L statement. Today, that dynamic has been completely inverted. We are witnessing a violent collision between Moore’s Law and the laws of thermodynamics, driven by the exponential power density required by the artificial intelligence revolution.

As a result, reliable power generation is no longer just a utility bill, it is becoming a strategic balance sheet asset, transitioning rapidly from opex to capex. We are watching the real-time merger of the computing and energy sectors.

This AI supercycle is colliding with what is already the Golden Age of Electrification. The rapid electrification of society, the rise of renewables, and desperately aging infrastructure are collectively fueling a historic electricity boom. The entire global electricity ecosystem is being restructured and heavily invested in to meet this unprecedented surge in demand.

However, this demand shock is running headfirst into a new macroeconomic reality: the age of tariffs, deglobalization, and a fierce focus on national sovereignty and reshoring. Western nations are urgently looking to secure energy independence and replace their reliance on imported fossil fuels.

This convergence of forces has created a rare political safe harbor in the United States. Some want decarbonization, whilst others want energy dominance, nuclear energy is the only technology that delivers both.

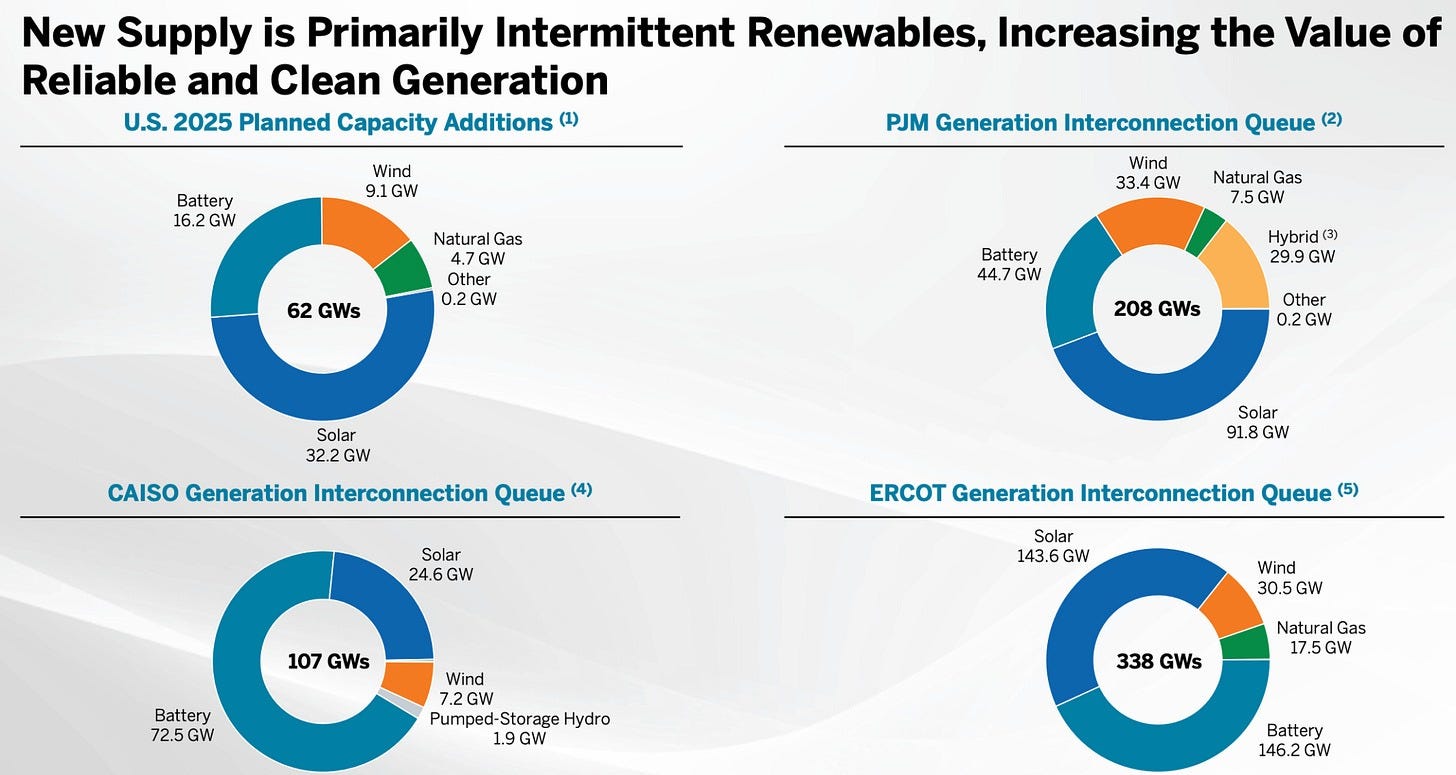

For decades, nuclear energy was viewed as problematic by investors, utilities, and regulators, but that sentiment has rapidly reversed. Nuclear is now being positioned as the ultimate all-of-the-above solution to the interconnected issues of soaring electricity demand and climate change. While intermittent renewable sources like solar and wind have grown, they fail during extreme weather, as a result, grid operators are now paying a massive premium for the sheer reliability of nuclear baseload power.

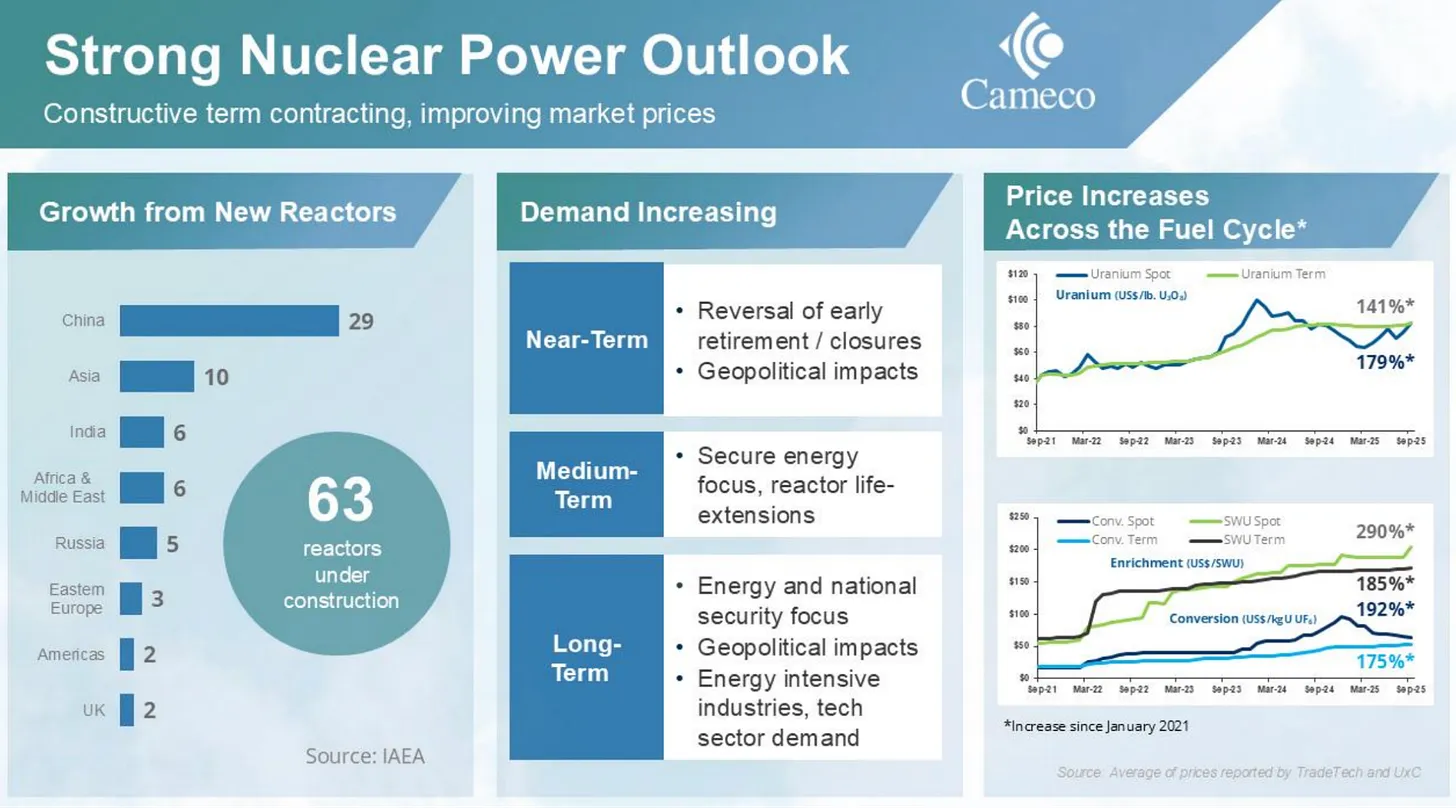

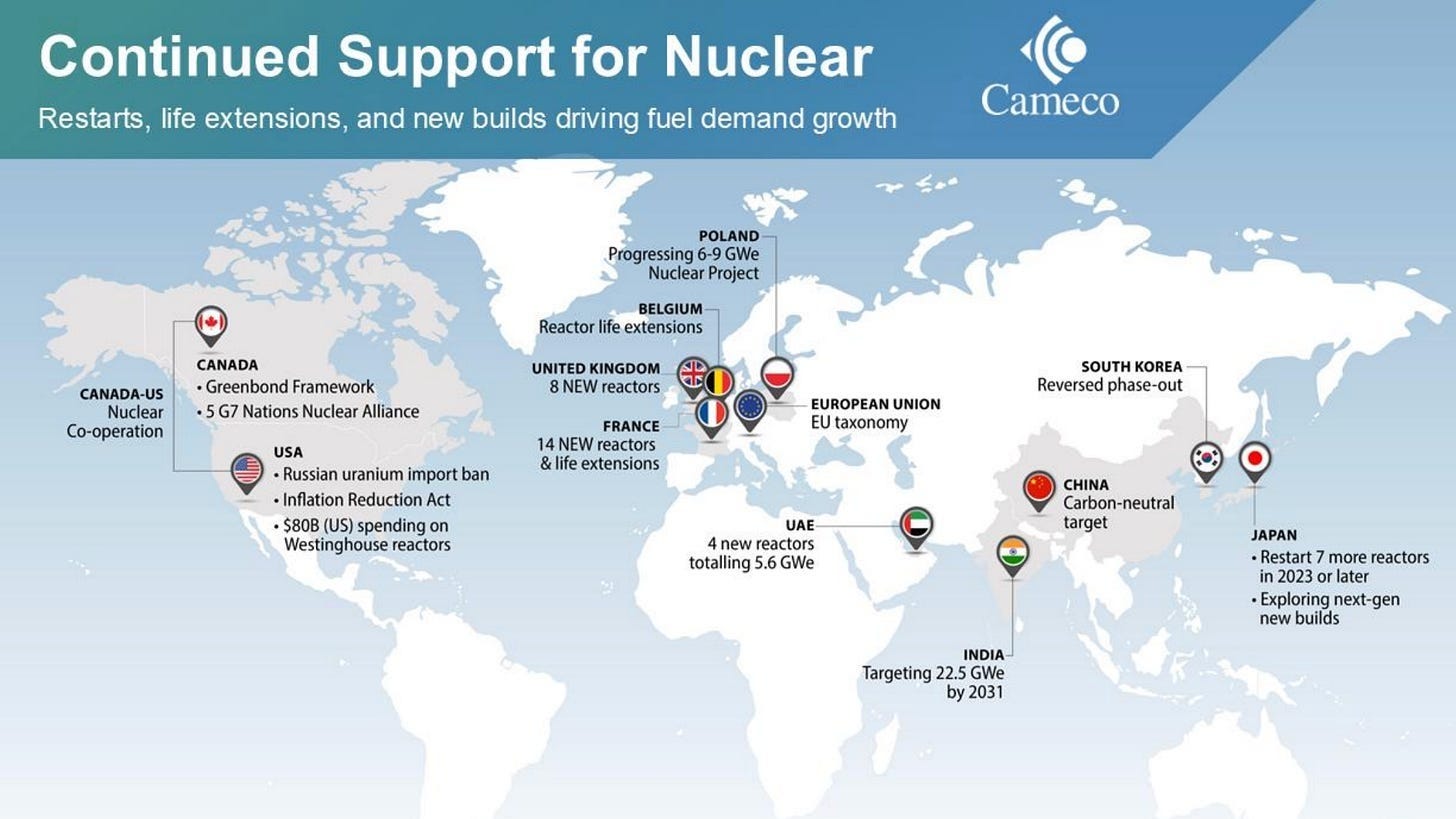

The global momentum behind this renaissance is undeniable. Following the COP28 pledge setting a global aspirational goal to triple nuclear energy capacity by 2050, the industry is hitting historic milestones. In 2025, global nuclear generation is set to reach an all-time high, with more than 410 reactors operating across over 30 countries. Even more telling for the future: there are currently 63 reactors representing over 70 GW of capacity under construction globally, the highest level of new nuclear build-out since 1990.

The COP28 commitment to triple nuclear capacity by 2050 has driven a new sense of urgency, paving the way for public policy U-turns as well as private sector commitments.

We are entering a Nuclear Renaissance.

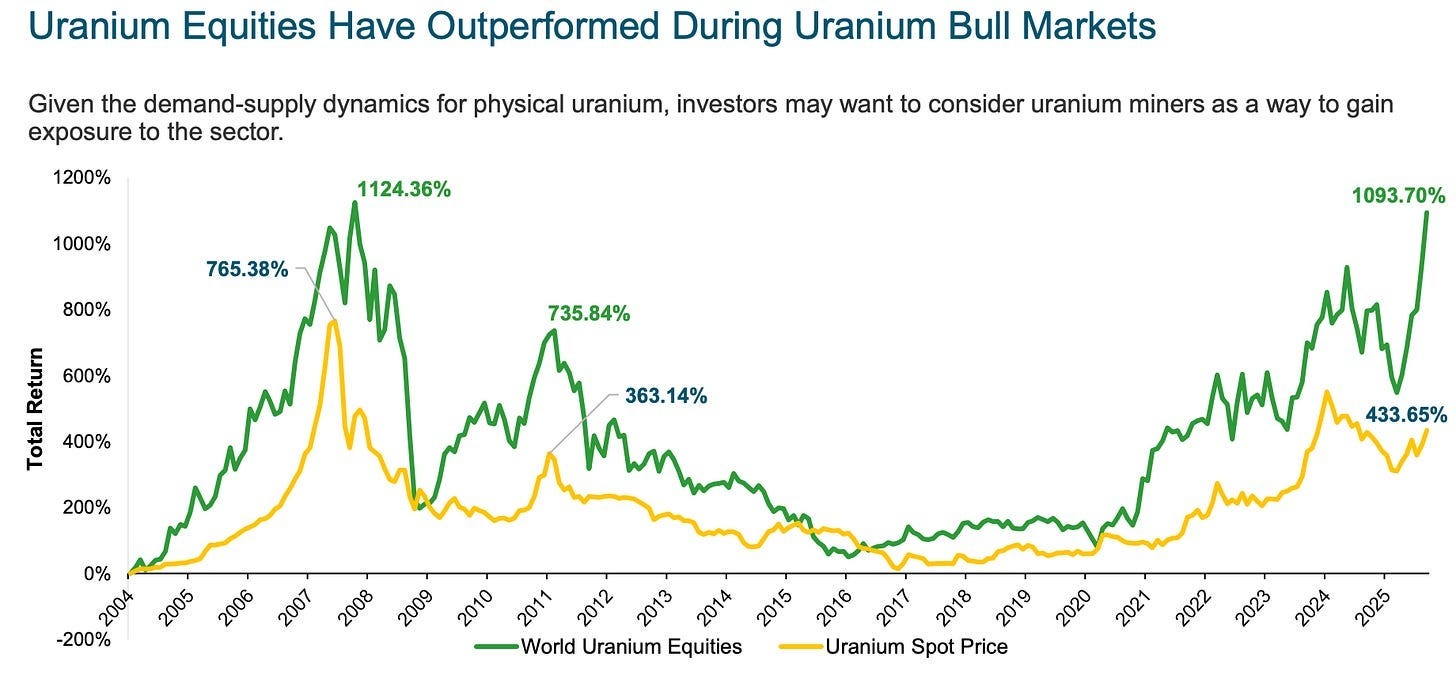

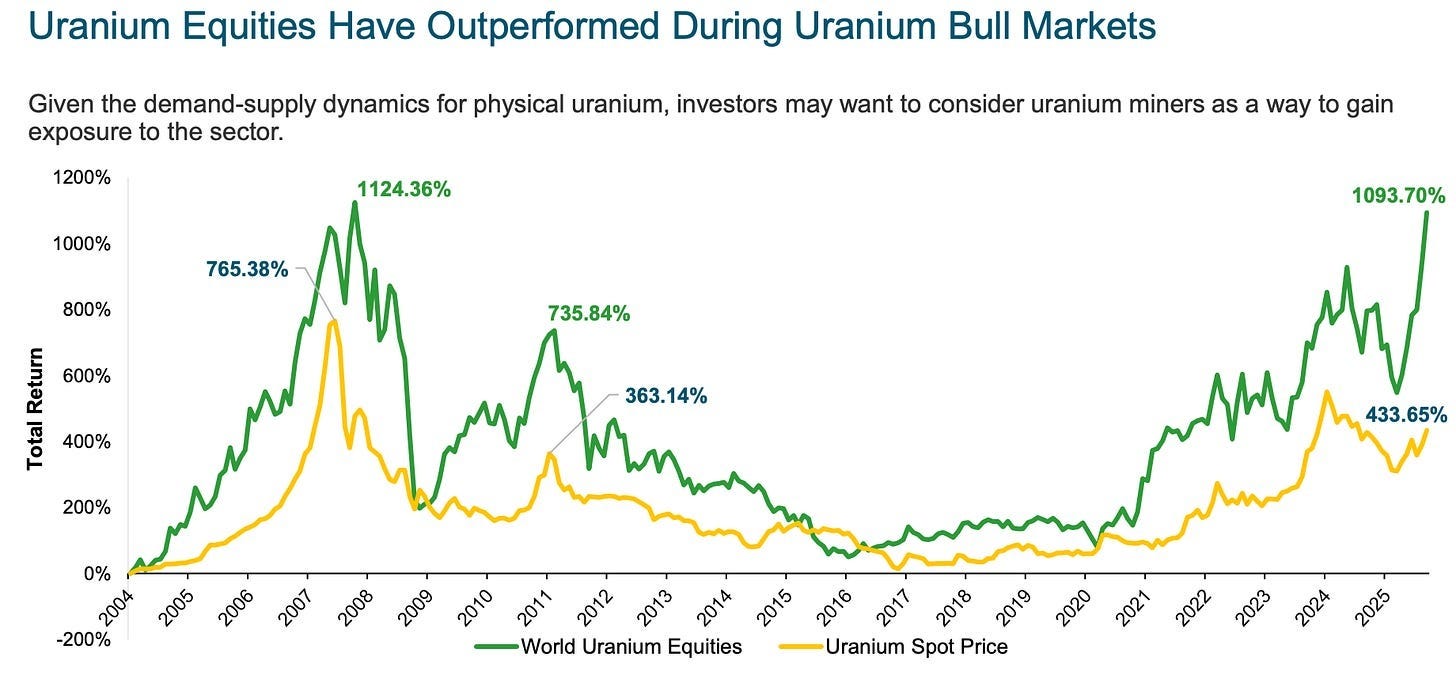

Why is this going to lead to a uranium supercycle? Demand for uranium is inelastic, uranium demand is structurally growing for the next decades, at the early stages of a nuclear renaissance, supply is struggling to keep up, geopolitical tensions are rising putting pressure on supply, financial demand is growing and the supply/demand deficit is only growing.

2025 was a big year for nuclear energy revival, especially in the US with many catalysts:

In May, executive orders were issued for the nuclear sector to have 10GW of nuclear new builds under construction by 2030 as well as orders for 5GW of upgrades to existing nuclear facilities along the same time frame.

Then in late October, the US government announced a partnership with Cameco, Westinghouse, and Brookfield to provide at least $80bn for new large scale nuclear projects in the US. The goal of the >$80bn is to jump start supply chains and help derisk the cost of the first movers, which will bear the brunt of higher sourcing and supply chain costs. This is important given how cautious utilities have been in building new nuclear reactors given the significant cost overruns (most recent project, Vogtle, ran $17bn over budget, costing a whopping $37bn). Of course, there still remains significant questions around what this investment will look like, we are likely to gain more clarity on this in 2026. How will this money be deployed? The allocation of federal dollars could take many forms ranging from upfront funding for long lead-time materials procurement to disbursements through the DOE’s Loans Program Office or other methods.

Why is nuclear power so well positioned in this day and age? Reliable, clean and energy dense baseload power

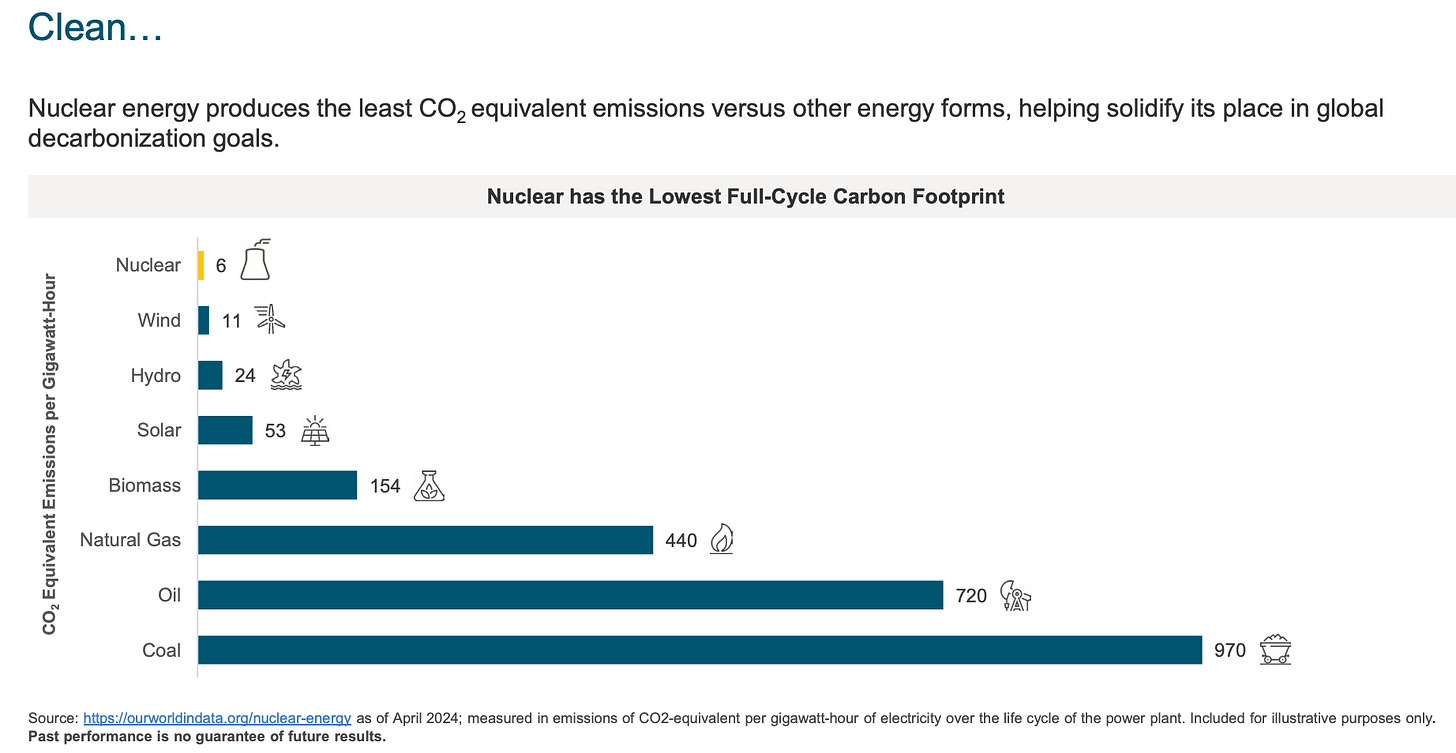

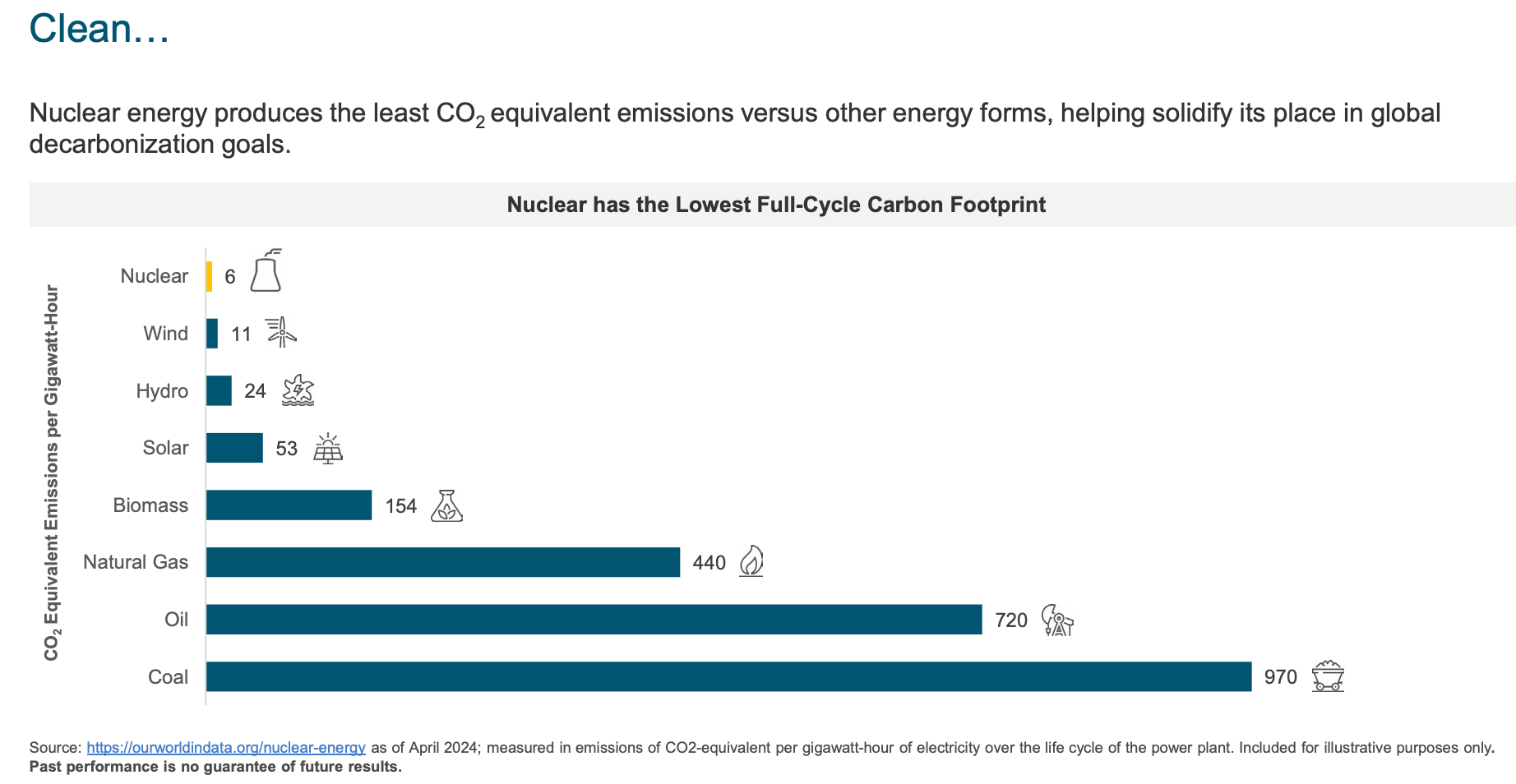

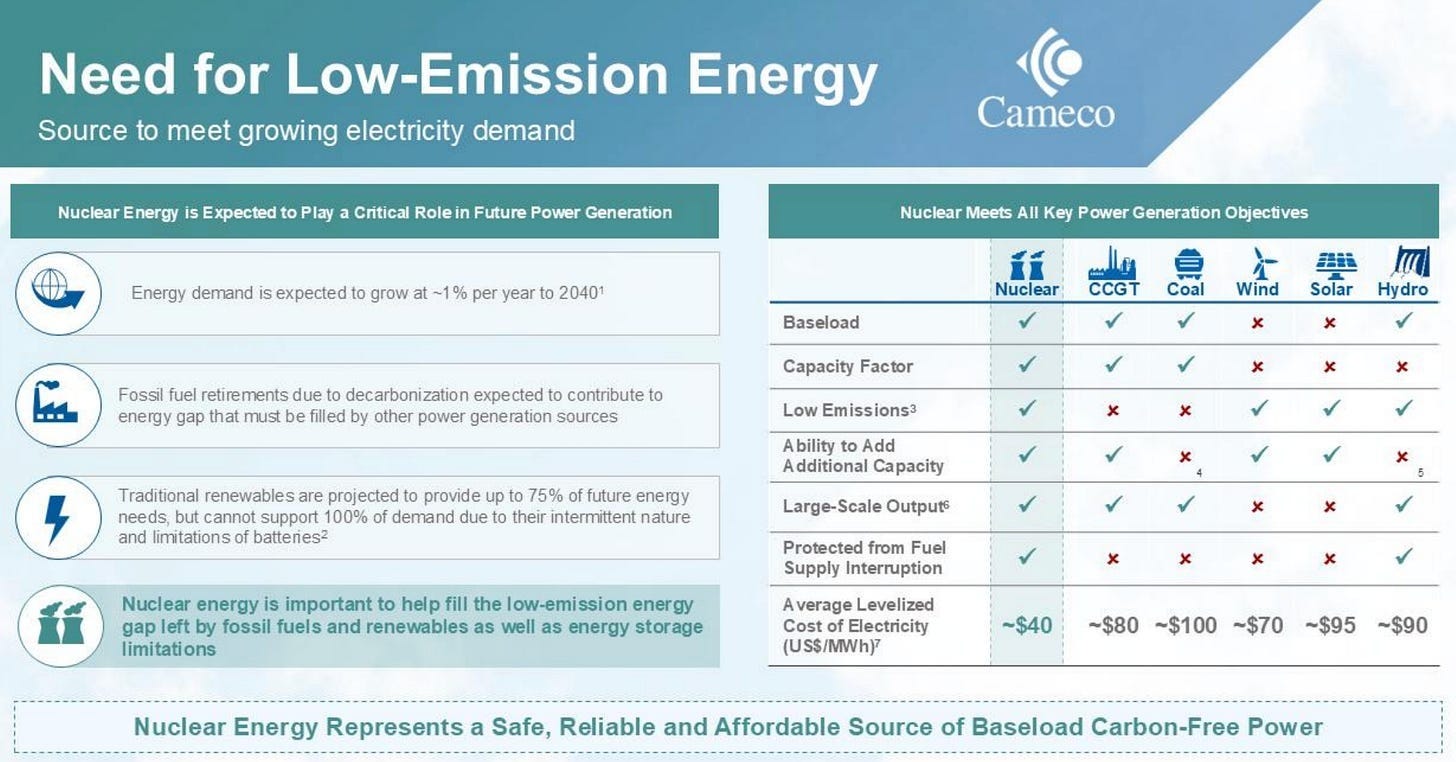

As a clean and highly reliable power source, nuclear is an essential part of a clean energy future: Increasingly, governments are recognizing nuclear as a source of clean energy that can be relied upon to operate during times when customer demand is at its peak. Nuclear fission emits no GHGs or criteria air pollutants, such as nitrogen oxides (NOX), sulfur dioxide (SO2), particulate matter (PM) or mercury. Nuclear power has one of the lowest carbon footprints of any electricity source, with the lowest lifecycle material and land use.

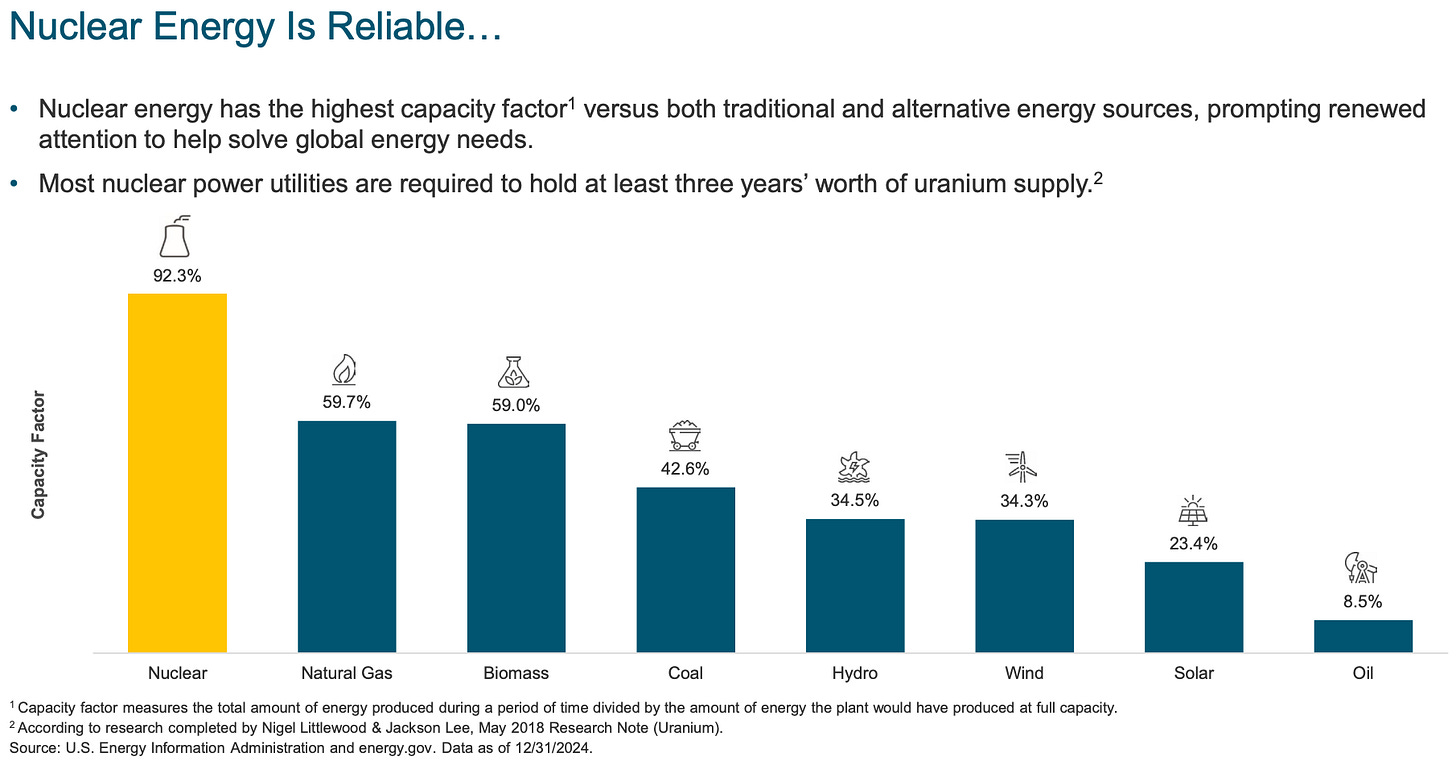

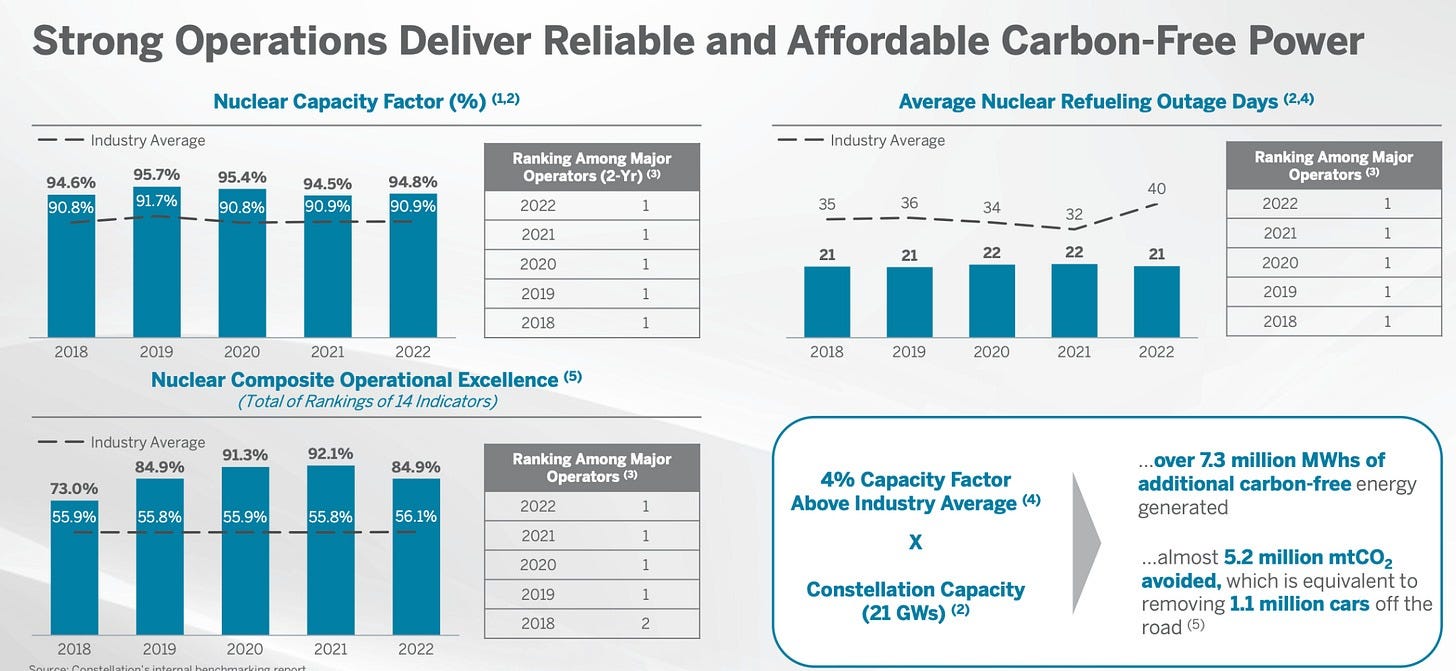

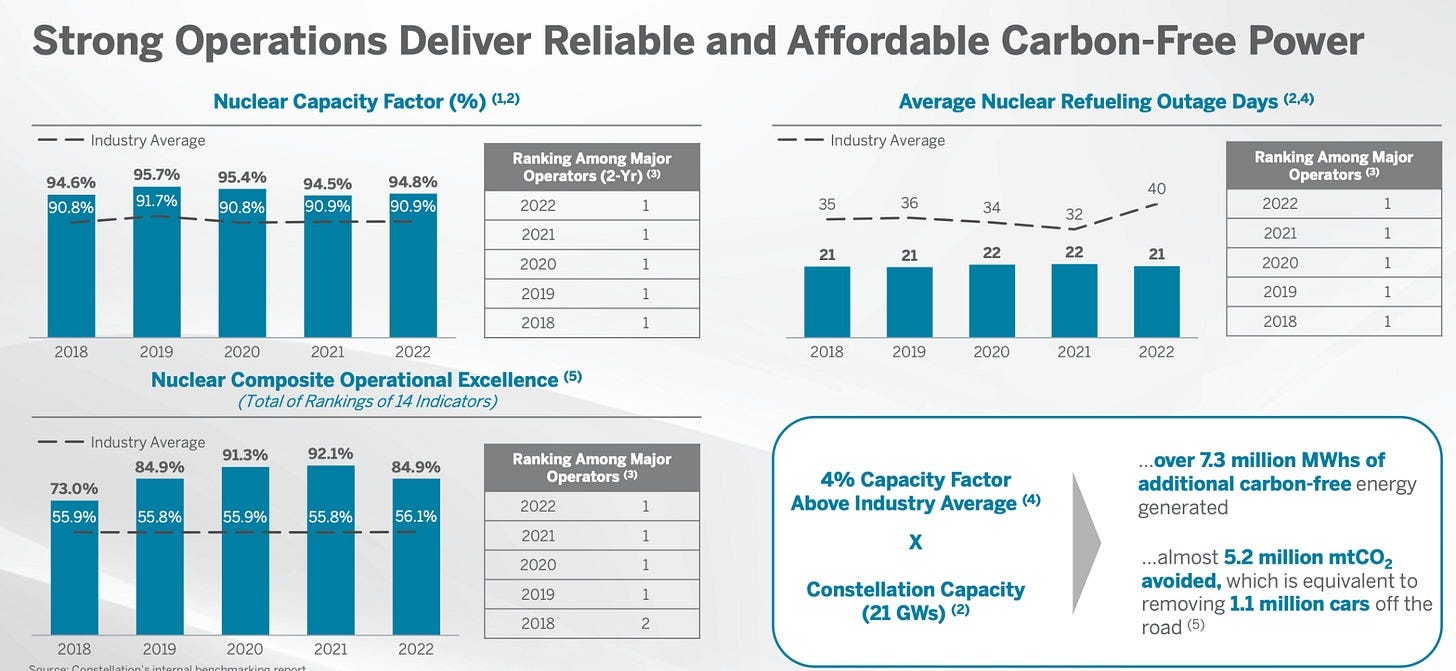

Nuclear is the most reliable energy source - providing reliable baseload power: When it comes to power generation, reliable baseload power, the minimum level of electricity that must be continuously supplied to meet demand on the grid, is essential. Nuclear power plants are highly dependable, producing power 93% of the time, on average, versus just 57% for natural gas and 40% for coal. Renewable sources like wind and solar are more variable, generating power 35% and 25% of the time, respectively. The technical term for this measure is capacity factor. It represents the ratio of actual electricity produced over a given period to the maximum potential output if the plant ran at full capacity all the time. For example, if a solar installation has a maximum capacity of 100 mega-watt hours (MWh) but only produces 25 MWh on average, its capacity factor is 25%. This difference in capacity factor explains why technologies with lower values struggle to provide steady power. Nuclear power plants deliver consistent output, while solar and wind fluctuate significantly. To compensate for these swings, renewable sources require either a backup source (such as natural gas or coal) or energy storage solutions like lithium- ion batteries. It operates 24 hours per day, 365 days per year, even in extreme cold or heat. It is the backbone of our nation’s energy grid. Through the Polar Vortex in 2014, Winter Storm Uri in 2021, Winter Storm Elliott in 2022, and numerous other once-in-a- hundred-year events that have happened in recent years, nuclear has kept the system running when other resources have not been available. During the summer of 2024, which experienced extended heatwaves and extreme weather, CEG’s nuclear fleet operated at a 98.1% capacity factor to keep the lights on and air conditioners humming 24/7 for nearly 16 million homes and businesses. Modern Gen III and VI reactors, however, can ramp up and down between 25-100% of power within minutes, this allows them to load-follow and better integrate with variable renewable energy/support grid balancing.

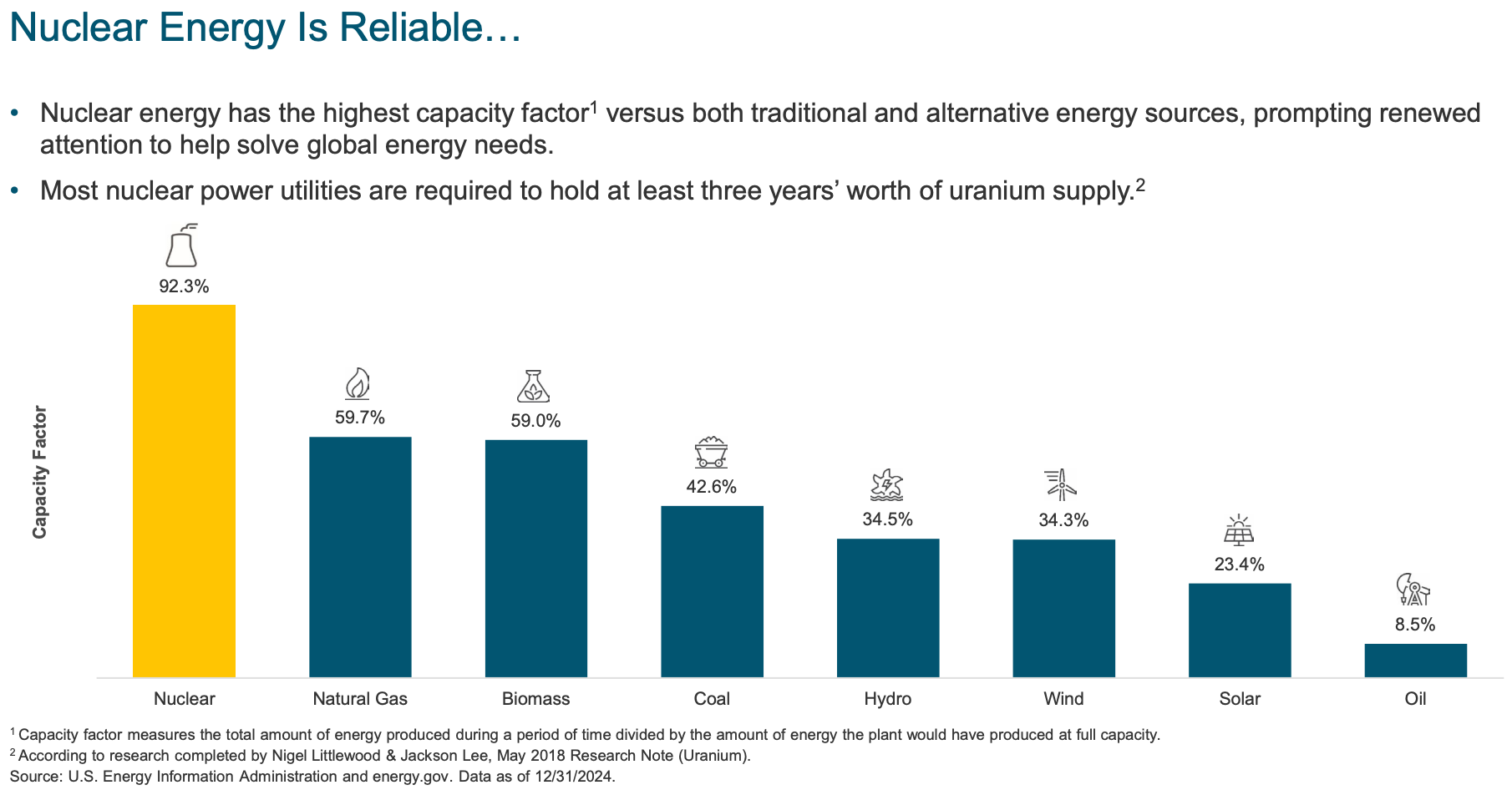

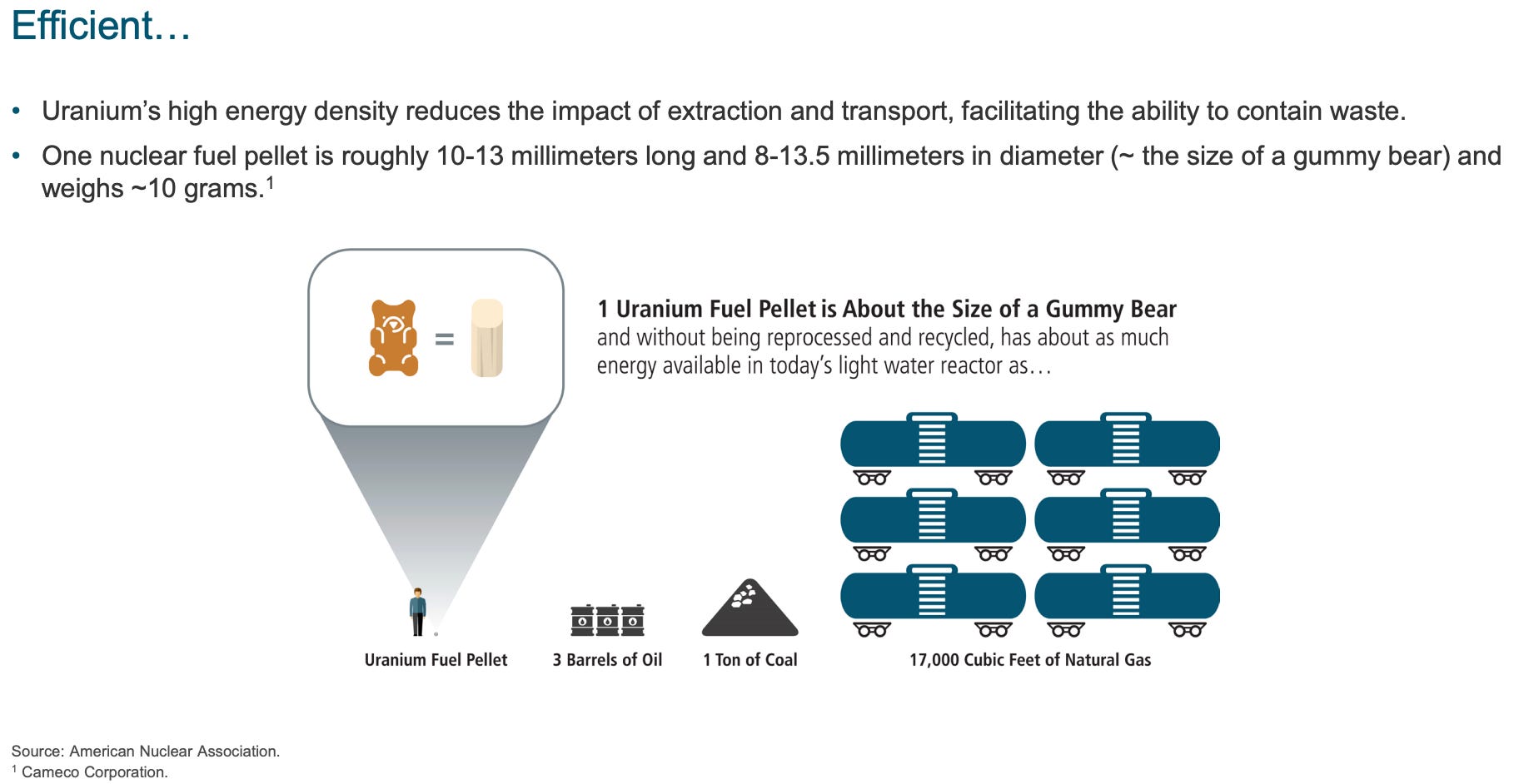

Ultra efficient power source - Nuclear produces more energy for the same amount of installed capacity than any other generation source: Plants usually need around 2 trucks of uranium a year, whereas a similar coal-fired plant would need 2000 full trains of coal a year. Uranium is incredibly energy dense. 1 tonne of natural uranium can produce 44m kWh of carbon free electricity, compared to >20,000 tonnes of thermal coal needed to produce the same electricity on top of the fact that it delivers carbon emissions. To put this into context, a single uranium fuel pellet (8-15mm in diameter and 10- 15mm in length) used in nuclear fuel can power a single light bulb for 5 years, whereas a similar amount of coal will only be able to power it for 100 seconds. Uranium’s high energy density reduces the impact of extraction and transport, facilitating the ability to contain waste. One nuclear fuel pellet is roughly 10-13 millimeters long and 8-13.5 millimeters in diameter (the size of a gummy bear) and weighs 10 grams.

One of the cheapest forms of energy though initial capital costs are very high (hence why government support is mandatory): Industry research suggests that, after accounting for efficiency, storage needs, transmission costs, and other broad system costs, nuclear power plants are one of the least expensive sources of energy. The initial capital costs for nuclear power are high, but energy payback, as measured by the energy return on investment (EROI), surpasses that of competing energy sources (like coal and natural gas).

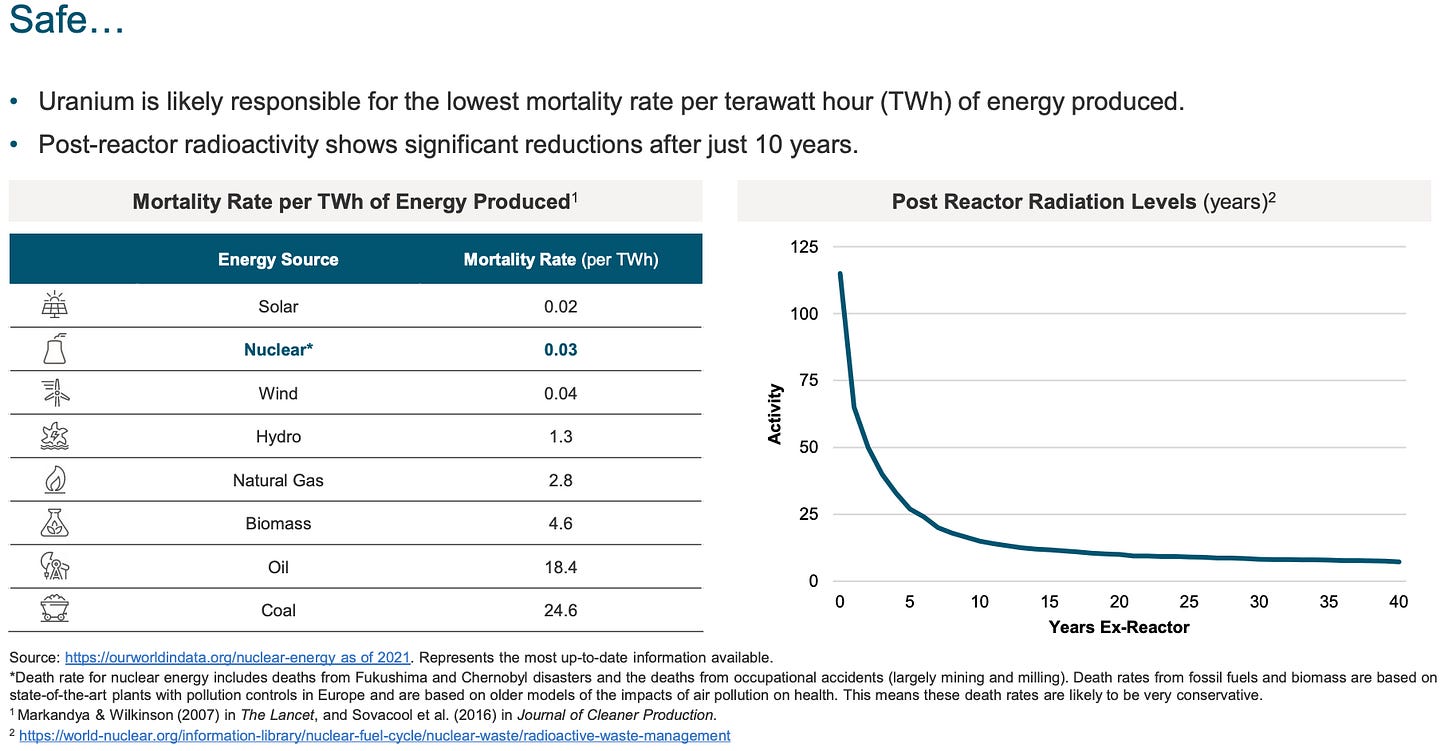

Safety (discussed in more details below): Containment and engineering methods have advanced significantly over the years, helping to reduce operational risks. A 1,000MW nuclear plant produces only three cubic meters of highly radioactive waste per year when recycling is applied. Long-term disposal remains a challenge, however, around 90% can currently be safely managed without extended storage. Looking ahead, as nuclear energy scales in the coming years, there is an opportunity to further develop and implement improved solutions for sustainable waste management.

Very long asset life with potential to extend to 60+ years: Nuclear plants can run for 60+ years, hence the commercial gains for a country in the long term are immense.

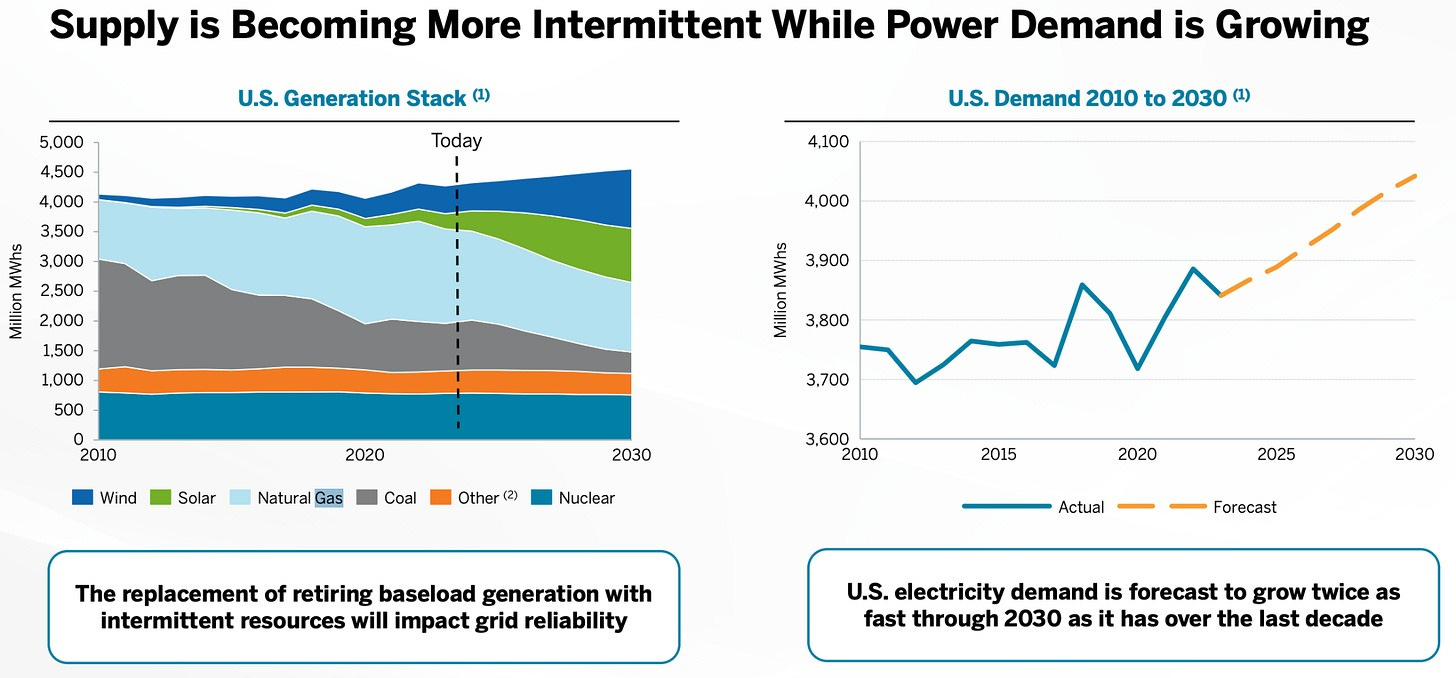

An inflection in load growth in the West after 2 decades of no electricity demand growth puts further pressure on utilities to upgrade grid infrastructure:

After two decades of stagnation, electricity demand in Western economies is finally inflecting. Since 2008, consumption has cumulatively declined by 10%. But the rapid expansion of data centers and the steady electrification of transport, industry, and heating are set to reverse that trend. Over the next decade, Europe’s power demand could rise by 40–50%.

This unprecedented load growth is prompting utilities and policymakers to rethink grid planning, capacity expansion, and reliability strategies to ensure the power system can meet future needs. Indeed, in order to respond to load growth, US utilities would have to add 70-90 GW of power generation per year in coming decades, 5-7x more compared to 10-20 GW in the prior 20 years.

2. Nuclear 101: The Fuel Cycle & The Reactor

To understand the investment thesis behind the nuclear renaissance, we first need to understand the underlying physics and the complex supply chain required to make it work.

At its core, a nuclear power plant is essentially a highly sophisticated steam engine. The magic lies in the heat source: Nuclear Fission.

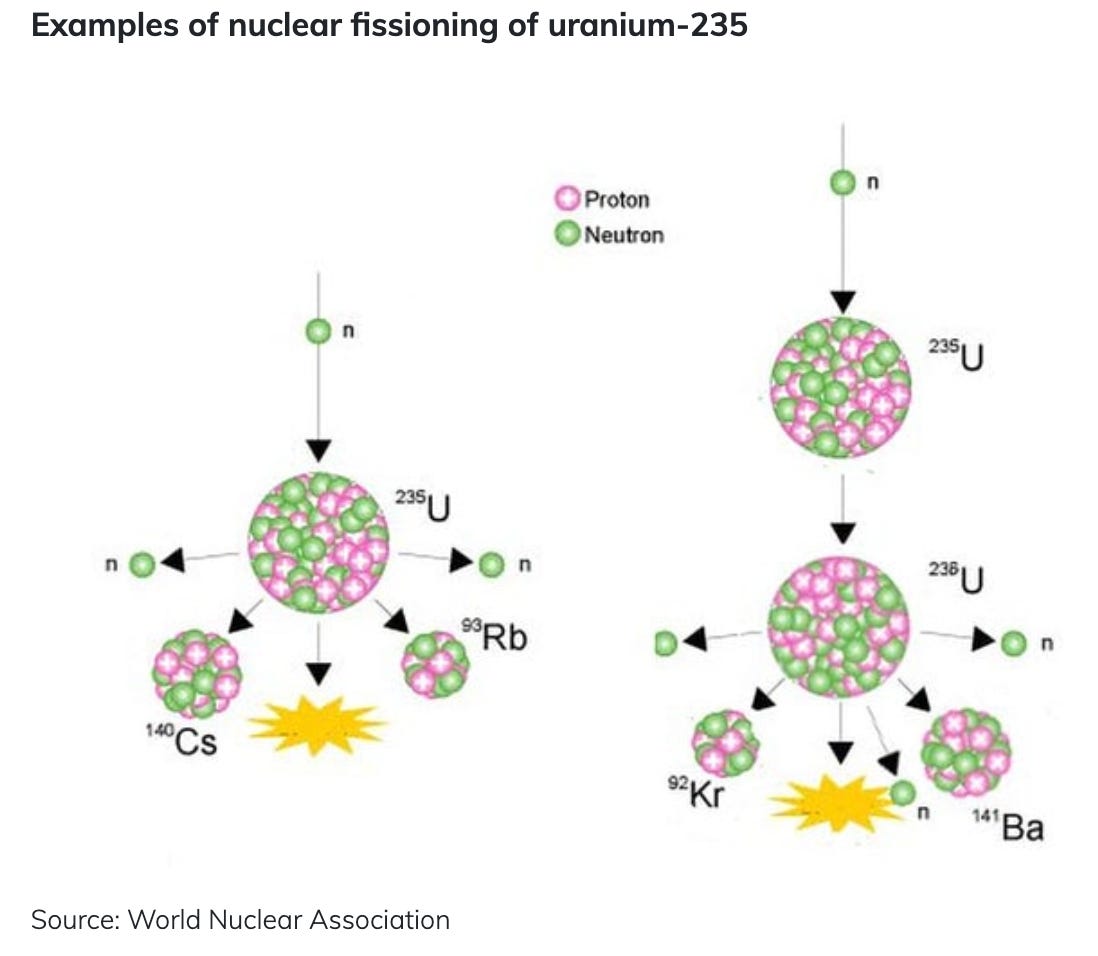

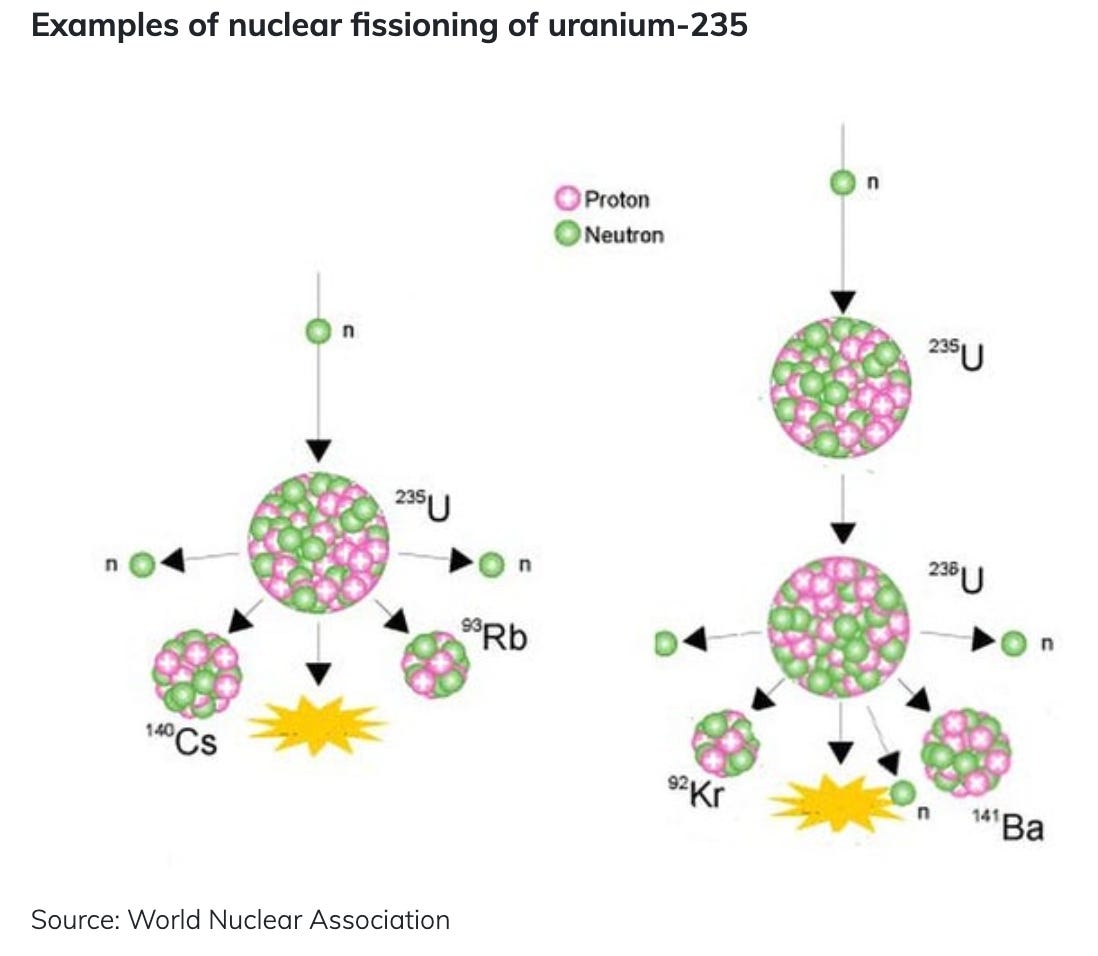

When the nucleus of a heavy atom, specifically the uranium-235 (U-235) isotope, is struck by a moving neutron, it splits in two. This splitting releases an enormous amount of heat, alongside two or three additional neutrons. Those newly freed neutrons go on to strike other U-235 atoms, causing them to split in a controlled, continuous chain reaction. The massive heat generated from this reaction is used to boil water, produce pressurized steam, and spin a turbine to generate electricity.

The energy density of this process is difficult to overstate: a single one-inch uranium fuel pellet contains the same amount of energy as one ton of coal. Just an egg-sized amount of uranium fuel can provide enough power for an average person’s entire lifetime.

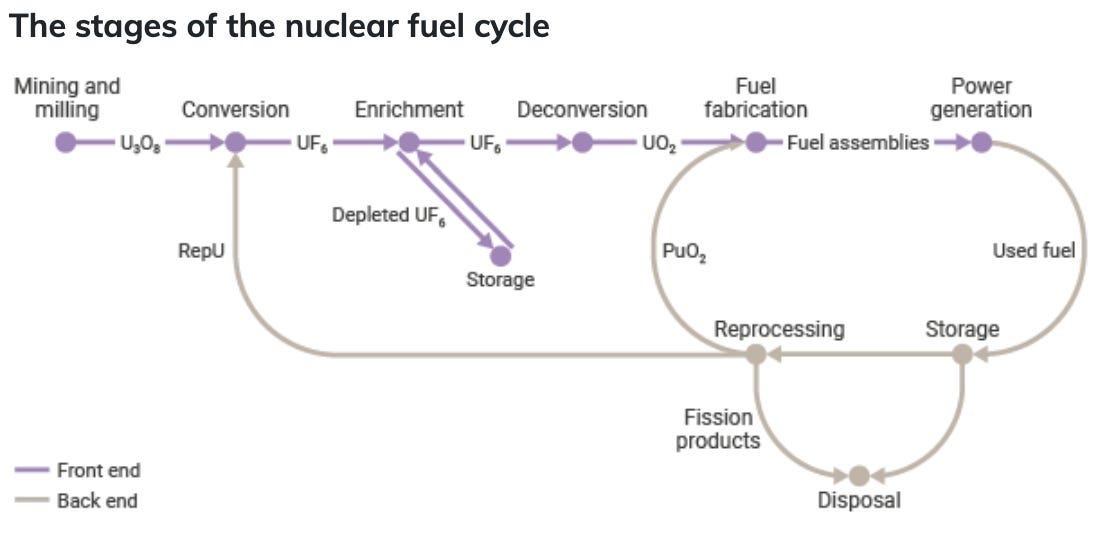

However, you cannot just dig uranium out of the ground and throw it into a reactor. It must go through the Front-End of the Nuclear Fuel Cycle, a highly specialized, multi-step industrial process that has recently become the center of a geopolitical chess match.

How nuclear power works:

Several hundred fuel assemblies make up the core of a reactor. For a reactor with an output of 1,000 MW, the core would contain about 75 tonnes of low-enriched uranium. In the reactor core the U-235 isotope fissions or splits, producing a lot of heat in a continuous process called a chain reaction. The process depends on the presence of a moderator such as water or graphite, and is fully controlled.

Some of the U-238 in the reactor core is turned into plutonium and about half of this is also fissioned, providing about one-third of the reactor’s energy output.

As in fossil-fuel burning electricity generating plants, the heat is used to produce steam to drive a turbine and an electric generator. Through this process, a 1,000 MW unit provides over 8 billion kilowatt hours (8 TWh) of electricity in one year, enough to power 600,000-900,000 homes.

To maintain efficient reactor performance, about one-third of the spent fuel is removed every year or 18 months, to be replaced with fresh fuel. The length of fuel cycle is correlated with the use of burnable absorbers in the fuel, allowing higher burn-up.

Typically, some 44m kWh of electricity is produced from one tonne of natural uranium. The production of this amount of electrical power from fossil fuels would require the burning of over 20,000 tonnes of coal or 8.5 million cubic metres of gas.

An issue in operating reactors, and hence specifying the fuel for them, is fuel burn-up. Fuel burn-up is measured in gigawatt-days (thermal) per tonne and its potential is proportional to the level of enrichment. To date a limiting factor has been the physical robustness of fuel assemblies, and hence burn-up levels have been limited to about 40 GWd/t, requiring only around 4% enrichment. With the advancement of equipment and fuel assemblies, 55 GWd/t is now possible (with 5% enrichment), and 70 GWd/t is in sight (though this would require 6% enrichment). The benefit of increased burn-up is that operation cycles can be longer, around 24 months, and the number of fuel assemblies discharged as used fuel can be reduced by one third. Associated fuel cycle cost is expected to be reduced by about 20%.

As with coal-fired power stations, about two thirds of the heat produced is released, either to a large volume of water (from the sea or large river, heating it a few degrees) or to a relatively smaller volume of water in cooling towers, using evaporative cooling (latent heat of vaporization).

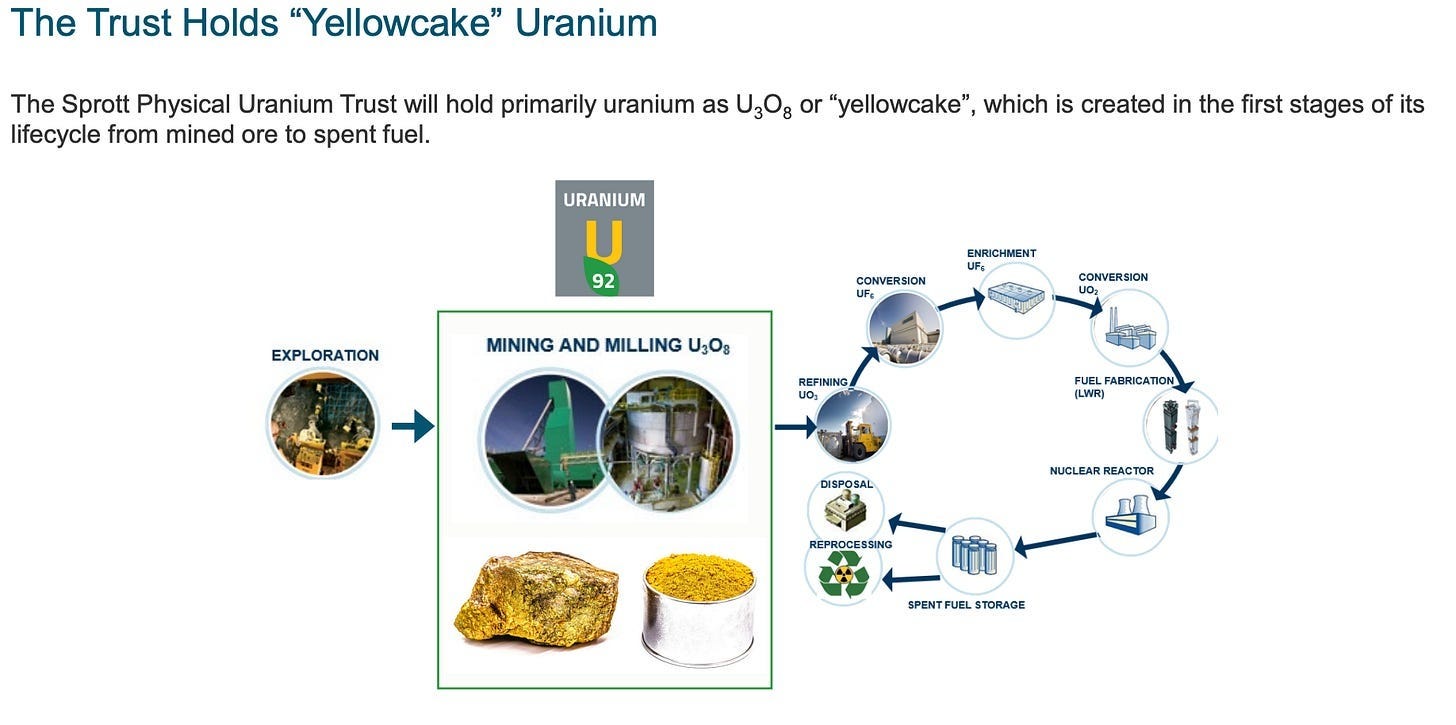

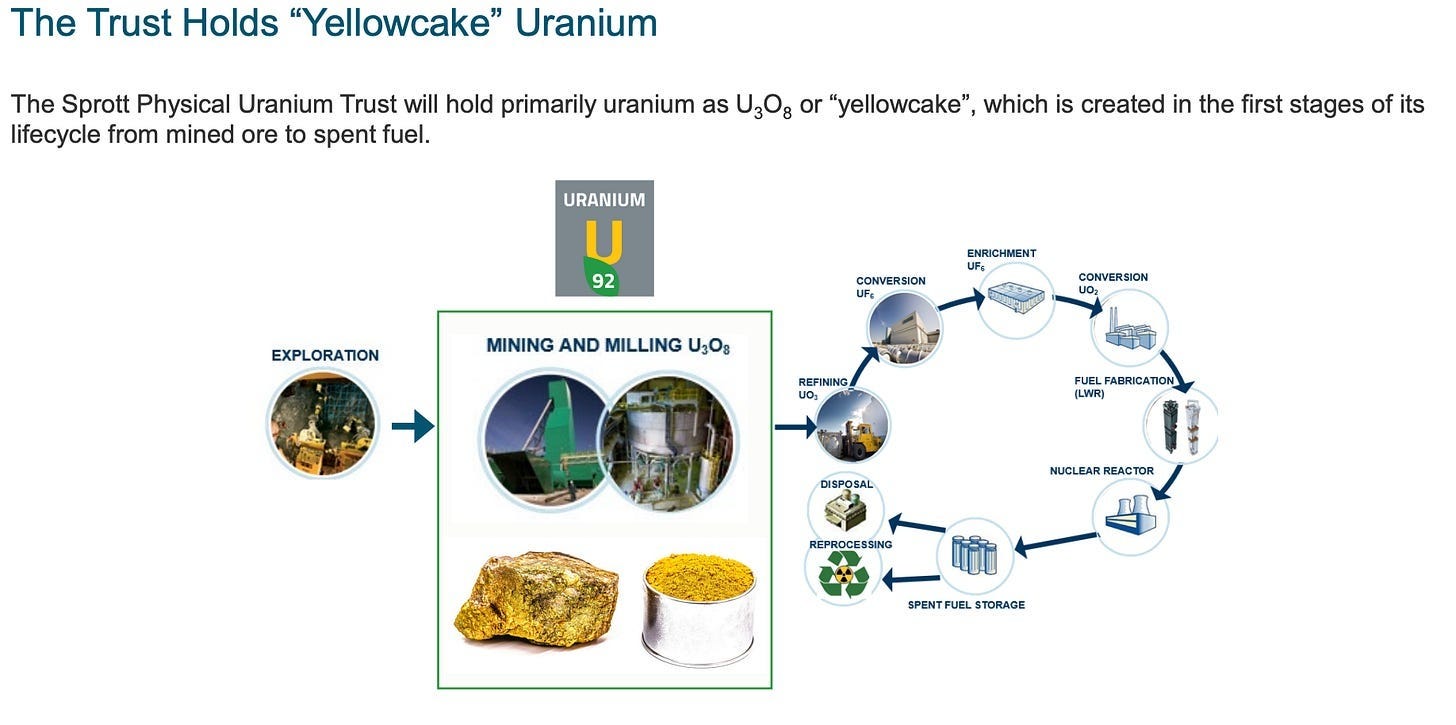

The Nuclear Fuel Cycle: From Uranium Ore to Reactor Fuel

On its path to becoming nuclear fuel, uranium goes through solid, liquid and gaseous forms. To prepare uranium for use in a nuclear reactor, it undergoes the steps of mining and milling, conversion, enrichment and fuel fabrication (front end of the nuclear fuel cycle). After uranium has spent about three years in a reactor to produce electricity, the used fuel may undergo a further series of steps including temporary storage, reprocessing, and recycling before the waste produced is disposed of (back end of the fuel cycle). Fuel removed from a reactor, after it has reached the end of its useful life, can be reprocessed so that most is recycled for new fuel.

Mining:

Uranium ore (UO2, or other mineral forms) naturally exists as the mineral uraninite which appears as a dense, silvery-grey metal typically found within most unconformity deposits (like in Canada), or as coffinite or carnotite which appear yellow or green and typically found within sandstone deposits (like in Kazakhstan). Unconformities or breccia-type hard ore deposits are mined using traditional underground or open-pit methods, whilst the sandstone deposits are extracted using in-situ recovery.

Companies involved in mining and milling:

UK: Yellow Cake

Canada: Cameco, Denison Mines, NextGen Energy

Kazakhstan: Kazatomprom

Australia: BHP, Paladin Energy, Boss Energy

China: CGN Mining

US: enCore Energy, Uranium Energy Core, Ur-Energy, Energy Fuels

France: Orano

Russia: Rosatom

Milling:

The mined uranium ore is milled and/or leach-processed into a concentrated, yellow or brown oxide powder, the famous yellowcake or U3O8, containing 80-85% of uranium (vs as little as 0.1% in the original ore). Triuranium octoxide (U3O8) is low in radioactivity and chemically stable, this is the standard tradable commodity that is quoted and sold on the markets, and transported around the world in 200L drums to be the feedstock of nuclear fuel.

Processing & conversion:

The solid yellowcake is chemically converted into uranium hexafluoride or UF6, colloquially termed the hex, through reduction and fluorination, which can exist either in stable solid form as a white crystalline for storage and transportation, or heated to vaporise into a gas form for isotope separation.

Companies involved in conversion:

France: Orano

Canada: Cameco

Enrichment:

Through a gas centrifuge which exploits the slight mass difference between the fissile U-235 isotope and the non-fissile U-238, the UF6 gas is spun and separated into two streams: one containing the level of desired U-235, and the other (the tail) with progressively depleted U-235 that is run back again through the centrifuge. Enrichment increases the content of the fissile isotope U- 235 from 0.7% in natural to 3-5%. Each tonne of enriched UF6 represents 7-8 tonnes of natural uranium feed.

Fuel fabrication & assemblies: The enriched UF6 is processed back into enriched uranium dioxide or UO2, a black powder-like substance that is sintered to make uranium fuel pellets. The fuel pellets are stacked and encapsulated in metal cladding into 3-4 metre long rods to be used as reactor fuel.

Companies involved in enrichment:

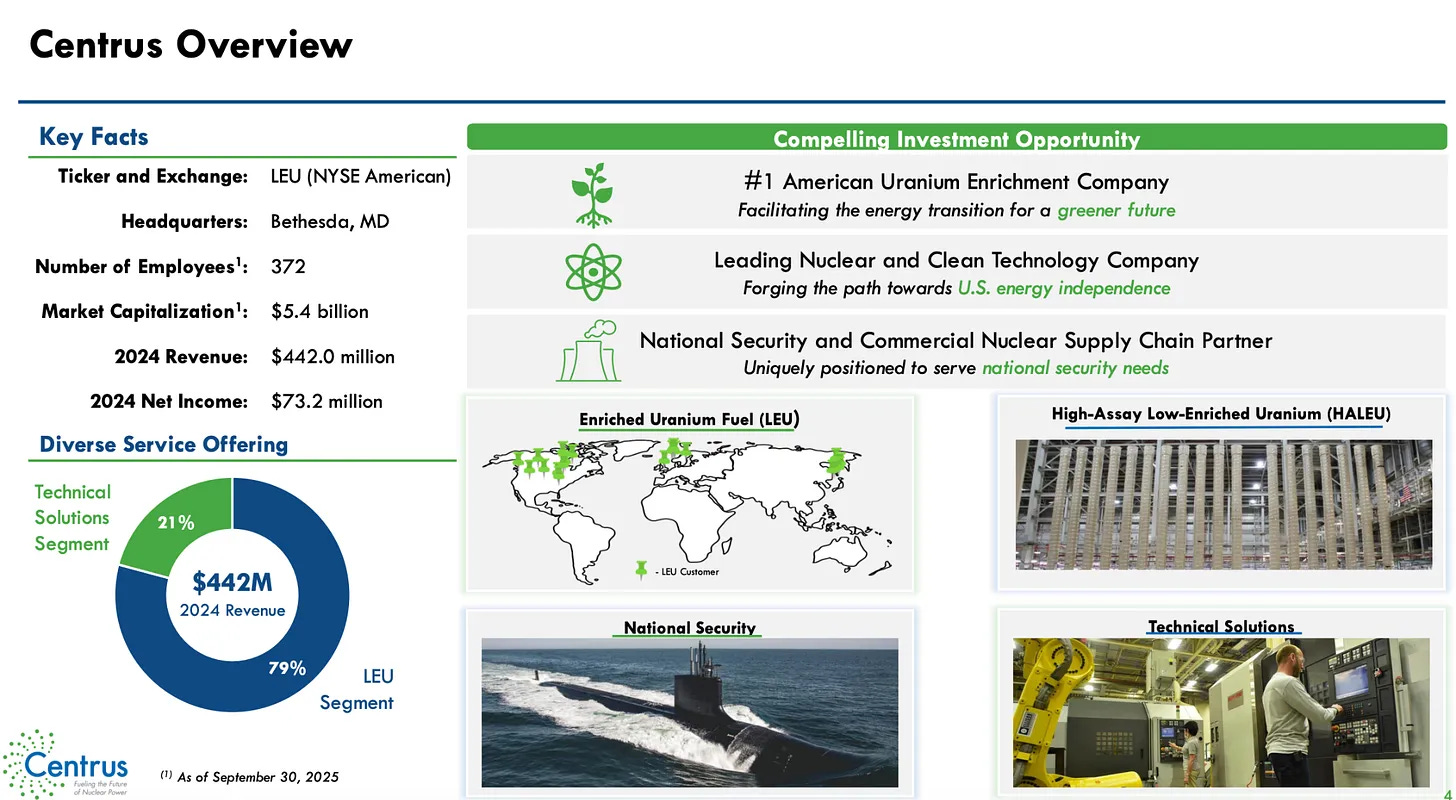

US: Centrus Energy, Lightbridge

UK: Urenco

France: Orano, Framatome

Russia: Rosatom

China: CNNC

Japan: Mitsubishi Heavy Industries

Power generation and burn-up:

Several hundred fuel assemblies make up the core of a reactor. For a reactor with an output of 1,000 MW, the core would contain about 75 tonnes of low-enriched uranium. In the reactor core the U-235 isotope fissions or splits, producing a lot of heat in a continuous process called a chain reaction. The process depends on the presence of a moderator such as water or graphite, and is fully controlled.

Some of the U-238 in the reactor core is turned into plutonium and about half of this is also fissioned, providing about one-third of the reactor’s energy output.

As in fossil-fuel burning electricity generating plants, the heat is used to produce steam to drive a turbine and an electric generator. Through this process, a 1,000 MW unit provides over 8 billion kilowatt hours (8 TWh) of electricity in one year, enough to power 600,000-900,000 homes.

To maintain efficient reactor performance, about one-third of the spent fuel is removed every year or 18 months, to be replaced with fresh fuel. The length of fuel cycle is correlated with the use of burnable absorbers in the fuel, allowing higher burn-up.

Typically, some 44m kWh of electricity is produced from one tonne of natural uranium. The production of this amount of electrical power from fossil fuels would require the burning of over 20,000 tonnes of coal or 8.5 million cubic metres of gas.

An issue in operating reactors, and hence specifying the fuel for them, is fuel burn-up. Fuel burn-up is measured in gigawatt-days (thermal) per tonne and its potential is proportional to the level of enrichment. To date a limiting factor has been the physical robustness of fuel assemblies, and hence burn-up levels have been limited to about 40 GWd/t, requiring only around 4% enrichment. With the advancement of equipment and fuel assemblies, 55 GWd/t is now possible (with 5% enrichment), and 70 GWd/t is in sight (though this would require 6% enrichment). The benefit of increased burn-up is that operation cycles can be longer, around 24 months, and the number of fuel assemblies discharged as used fuel can be reduced by one third. Associated fuel cycle cost is expected to be reduced by about 20%.

As with coal-fired power stations, about two thirds of the heat produced is released, either to a large volume of water (from the sea or large river, heating it a few degrees) or to a relatively smaller volume of water in cooling towers, using evaporative cooling (latent heat of vaporization).

Used fuel:

With time, the concentration of fission fragments and heavy elements in the fuel will increase to the point where it is no longer practical to continue using it. So after 18-36 months the used fuel is removed from the reactor. The amount of energy that is produced from a fuel assembly varies with the type of reactor and the policy of the reactor operator. Used fuel will typically have about 1.0% U-235 and 0.6% fissile plutonium (almost 1% Pu total), with around 95% U-238.f The balance, about 3%, is fission products and minor actinides.

When removed from a reactor, the fuel will be emitting both radiation, principally from the fission fragments, and heat. It is unloaded into a storage pond immediately adjacent to the reactor to allow the radiation levels to decrease. In the ponds, the water shields the radiation and absorbs the heat, which is removed by circulating the water through external heat exchangers. Used fuel is held in such pools for several months and sometimes many years. It may then be transferred to naturally-ventilated dry storage, generally on site.

Depending on the policies of particular countries, some used fuel may be transferred to central storage facilities. Whilst there is a clear incentive for interim storage, used fuel must ultimately either be reprocessed in order to recycle most of it, or prepared for permanent disposal. The longer it is stored, the easier it is to handle, due to decay of radioactivity.

There are two options for used fuel: Reprocessing to recover and recycle the usable portion of it or long-term storage and final disposal without reprocessing.

Reprocessing: Used fuel still contains about 96% of its original uranium, of which the fissionable U-235 content has been reduced to less than 1%. About 3% of the used fuel comprises waste products and the remaining 1% is plutonium (Pu) produced while the fuel was in the reactor. Reprocessing separates uranium and plutonium from waste products (and from the fuel assembly cladding) by cutting up the fuel rods and dissolving them in acid to separate the various materials. It enables recycling of the uranium and plutonium into fresh fuel, and produces a significantly reduced amount of waste (compared with treating all used fuel as waste). The remaining 3% of high-level radioactive waste (some 750 kg per year from a 1,000 MW reactor) can be stored in liquid form and subsequently solidified.

Uranium and plutonium recycling:

The uranium recovered from reprocessing, which typically contains a slightly higher concentration of U-235 than occurs in nature, can be reused as fuel after conversion and enrichment.

The plutonium can be directly made into mixed oxide (MOX) fuel, in which uranium and plutonium oxides are combined. In reactors that use MOX fuel (which power 5% of the nuclear fleet and 10% of France’s fleet), plutonium substitutes for the U-235 in normal uranium oxide fuel.

About eight fuel assemblies reprocessed can yield one MOX fuel assembly, two-thirds of an enriched uranium fuel assembly, and about three tonnes of depleted uranium (enrichment tails) plus about 150 kg of waste. It avoids the need to purchase about 12 tonnes of natural uranium from a mine.

Another way of recycling plutonium and uranium from reprocessing is Russia’s REMIX-Fuel (REgenerated MIXture of U, Pu oxides), not yet commercialized. Here a non-separated mix of both has some low-enriched uranium (17% U-235) added, to produce fuel with about 1% Pu-239 and 4% U-235.

Apart from the incidental transformation of U-238 into plutonium in a normal reactor, U-238 is not usable in today’s fuel cycle. However, in a fast neutron reactor it is fissionable, as well as (more importantly) giving rise to plutonium, and is therefore potentially valuable. Increasingly, today’s used fuel is being seen as a future resource rather than a waste.

Nuclear waste:

Waste from the nuclear fuel cycle is categorized as high-, medium- or low-level based on the amount of radiation that it emits. This waste comes from a number of sources and includes:

Low-level waste produced at all stages of the fuel cycle.

Intermediate-level waste produced during reactor operation and by reprocessing.

High-level waste, which is waste containing the highly-radioactive fission products separated in reprocessing, and in many countries, the used fuel itself. Separated high-level waste also contains long-lived transuranic elements (all radioactively unstable).

After reprocessing, the liquid high-level waste can be calcined (heated strongly) to produce a dry powder, which is incorporated into borosilicate (Pyrex) glass to immobilize it. The glass is then poured into stainless steel canisters, each holding 400 kg of glass. A year’s waste from a 1,000 MW reactor is contained in five tonnes of such glass, or about 12 canisters 1.3 metres high and 0.4 metres in diameter. These can readily be transported and stored, with appropriate shielding.

The uranium enrichment process leads to the production of much depleted uranium, in which the concentration of U-235 is significantly less than the 0.7% found in nature. Small quantities of this material, which is primarily U-238, are used in applications where its very high-density characteristics are required, including radiation shielding the production of MOX fuel. While U-238 is not fissile it is a low specific activity radioactive material and some precautions must, therefore, be taken in its storage or disposal.

Companies involved in waste disposal:

France: Veolia, Orano

US: Holtec, Cadre

South Korea: Hyundai E&C, Korea Nuclear Fuel

Russia: Rosatom

UK: Babcock

Used fuel and separated waste, final disposal:

At the present time, there are no disposal facilities (as opposed to storage facilities) in operation in which used fuel not destined for reprocessing, and the waste from reprocessing, can be placed. In either case the material is stored in a solid, stable wasteform.

There is currently no pressing need to establish such facilities, as the total volume of such waste is relatively small. Further, the longer it is stored the easier it is to handle, due to the progressive decrease of radioactivity.

There is also a reluctance to dispose of used fuel because it represents a significant energy resource which could be reprocessed at a later date to allow recycling of the uranium and plutonium.

A number of countries are carrying out studies to determine the optimum approach to the disposal of used fuel and waste from reprocessing. The general consensus favours its placement into deep geological repositories, about 500 metres down, initially recoverable before being permanently sealed.

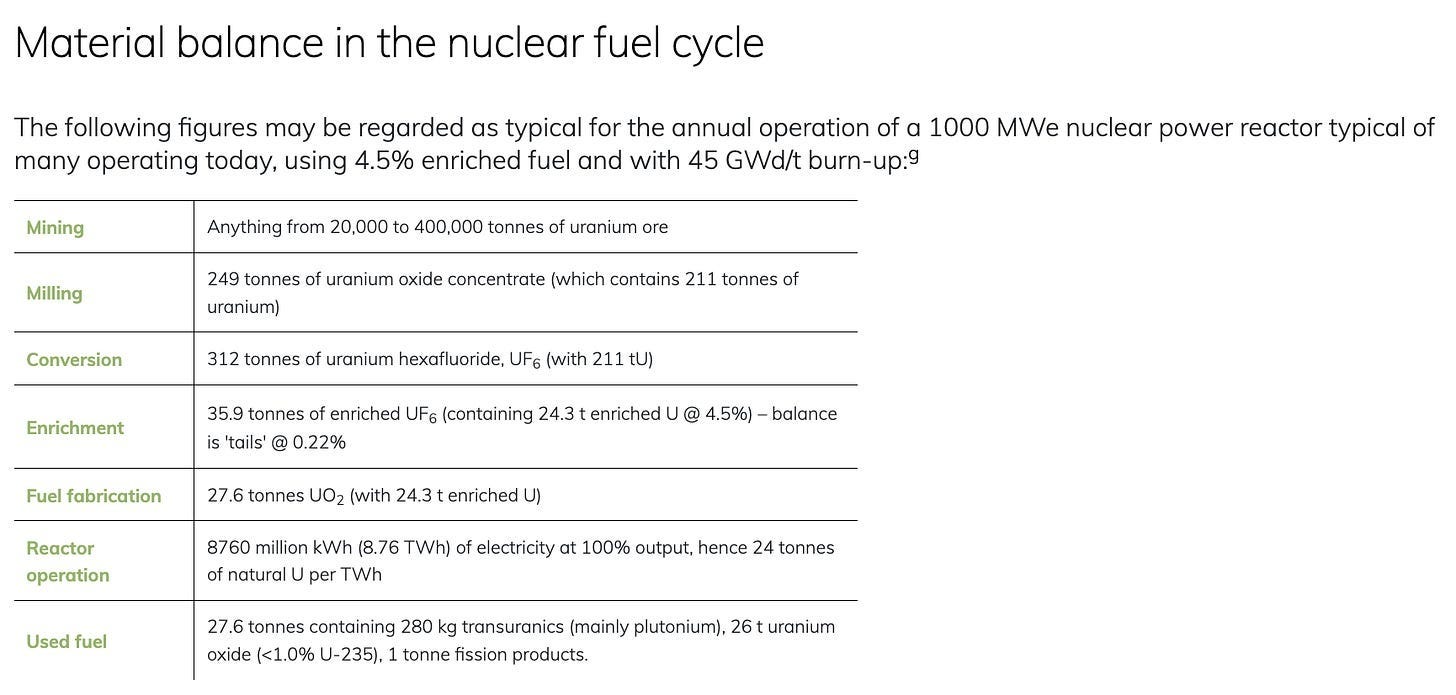

To give a sense of the lifecycle of uranium with real numbers, for a 1,000 MW nuclear power reactor (typical of the reactors operating today, for context France has 63,000 MW of installed nuclear power capacity), you need to extract 20,000-40,000 tonnes of uranium ore to make 27.6 tonnes of enriched fuel (UO2), with ⅓ needing to be replaced every year.

The Geopolitics of Fuel: A Race for Sovereignty

While uranium resources themselves are relatively abundant, the capability to process them is not. The West allowed its nuclear fuel supply chain to atrophy over the last few decades, creating a glaring national security vulnerability.

Nowhere is this more obvious than in enrichment. The enrichment process is highly complex, capital-intensive, and proliferation-sensitive. Today, Russia controls roughly 46% of global enrichment capacity. For context, in 1985, the United States was the world’s dominant enricher with >65% of global capacity, today, it has zero domestically owned enrichment capacity. Prior to recent geopolitical events, Russia supplied roughly 24% of the US and 31% of the EU’s enriched uranium demand.

Following the war in Ukraine, Western nations realized the danger of relying on strategic adversaries for baseload power. This sparked a furious race for energy sovereignty. In May 2024, the US signed the Prohibiting Russian Uranium Imports Act into law, officially banning the import of enriched uranium from Russia (with temporary waivers allowed through 2027).

This bifurcation of the market is structurally altering uranium demand. When enrichment capacity tightens due to sanctions, Western enrichers are forced to overfeed their centrifuges, meaning they must run significantly more raw natural uranium through the system to extract the required amount of U-235. This dynamic artificially amplifies the demand for raw uranium, which, combined with the West’s urgent push to reshore billions of dollars into domestic conversion and enrichment facilities, has set the stage for a massive uranium and nuclear supply chain upcycle.

The Nuclear Hardware: From Water-Cooled Giants to Fast Reactors

While the nuclear fuel cycle dictates how we get the energy out of the ground, the reactor technology determines how we harness it. Over the last 70 years, reactor hardware has evolved through distinct generations, prioritizing efficiency, passive safety, and waste reduction.

The Baseline: Water-Cooled Reactors (WCRs) Today, the global commercial nuclear industry is almost entirely standardized around a single core concept: the Water-Cooled Reactor (WCR). WCRs account for over 95% of all operational nuclear power plants worldwide. Among these, the Pressurized Water Reactor (PWR) is the undisputed king, making up roughly 74% of the global fleet and generating 78% of the world’s nuclear electricity.

In a traditional WCR, uranium-235 fuel pellets are used to start a controlled chain fission reaction. The heat from this reaction boils water into pressurized steam, which spins a massive turbine to generate electricity. These are the “Generation II” workhorses that were built predominantly in the 1970s and 1980s.

The Evolution: Passive Safety and Advanced Fuels (Gen III+)

The reactors currently being built today, such as the Westinghouse AP1000 in the US, the EPR in France, the APR1400 in South Korea/UAE, and the HPR1000 in China, represent “Generation III+” technology.

The defining evolutionary leap for these advanced WCRs is the integration of passive safety systems. Unlike older reactors that required active, electrically powered pumps and human intervention to cool the core during an emergency, Gen III+ passive systems rely on natural physical forces like gravity, natural circulation, and compressed gas to safely shut down the reactor without needing any external power.

Furthermore, the industry is transitioning to Advanced Technology Fuels (ATFs) and pushing for higher fuel burn-up rates. By enriching fuel slightly higher, modern reactors can extend their operating cycles (meaning they need to be refueled less often) and squeeze significantly more energy out of the same amount of uranium.

The Frontier: Fast Neutron Reactors (FNRs)

While WCRs use water to moderate (or slow down) neutrons, the absolute frontier of nuclear engineering, Generation IV technology, relies on Fast Neutron Reactors (FNRs).

FNRs operate without a moderator, utilizing high-energy, fast-moving neutrons to split atoms. Instead of water, they use advanced coolants like liquid sodium or liquid lead. This is a massive technological leap for two reasons:

Fuel Efficiency: FNRs can extract over 60 times more energy from uranium than normal reactors. They can even be configured as breeder reactors to produce more fissile material than they consume.

Waste Reduction: Because of the fast neutron spectrum, these reactors can significantly reduce the volume and radiotoxicity of high-level nuclear waste, effectively burning the long-lived actinides that currently require thousands of years of geological storage.

Currently, the East is dominating this frontier. Russia operates three sodium-cooled fast reactors (including the 880 MW BN-800) and is building a 300 MW demonstration lead-cooled fast reactor. China is commissioning its own 600 MW fast reactors (CFR-600), and India is commissioning a 500 MW Prototype Fast Breeder Reactor (PFBR).

The Demographic Cliff: The Aging Fleet vs. Life Extensions

The reality of the current nuclear renaissance is that it relies heavily on an aging foundation. Following decades of underinvestment and stagnation, the global nuclear fleet has a median age of roughly 32 years. Today, 66% of operational reactors have been running for over 30 years, and 34% have been operating for over 40 years.

To meet the COP28 pledge of tripling nuclear capacity by 2050, the industry cannot just build new plants, it must execute a massive wave of Long-Term Operations (LTO). Reactors that were originally licensed to operate for 40 years are undergoing massive modernization programs. Regulators are now approving life extensions pushing operational lifespans out to 60 and 80 years, with current policy frameworks even preparing for the possibility of reactors operating for up to 100 years.

The End of the Cycle: Decommissioning and Remediation

Eventually, all reactors reach the end of their useful lives. As of late 2024, 211 power reactors across 21 countries were shut down and undergoing decommissioning, while 23 power units had been fully decommissioned.

Historically, operators would place shut-down reactors into long-term safe enclosure to let radiation levels drop over decades. Today, the trend has shifted aggressively toward early dismantling. To avoid the rising costs of facility maintenance and prolonged surveillance, specialized, multi-company consortia are stepping in to take over and execute complete decommissioning projects at fixed budgets. This phase of the lifecycle is becoming highly advanced, with heavy reliance on digital twins, remote sensing, and robotics (like Boston Dynamics dogs) to handle materials, segment facility components, and safely access high-dose areas.

3. The Current State of Nuclear Energy

Nuclear Power Generation

Who uses nuclear power? About 9% of the world’s electricity is generated from uranium in nuclear reactors. This amounts to over 2500 TWh each year, as much as from all sources of electricity worldwide in 1960.

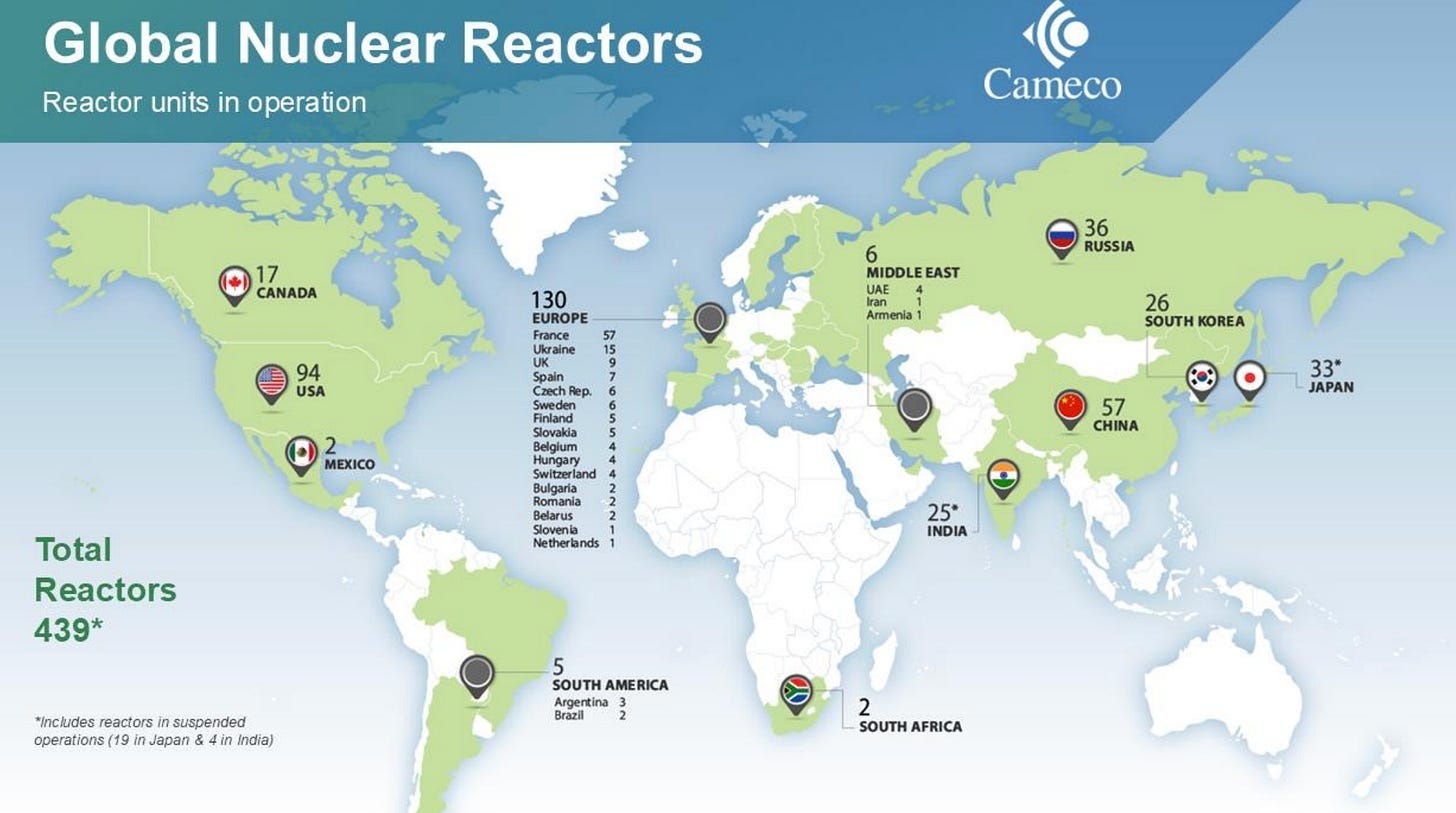

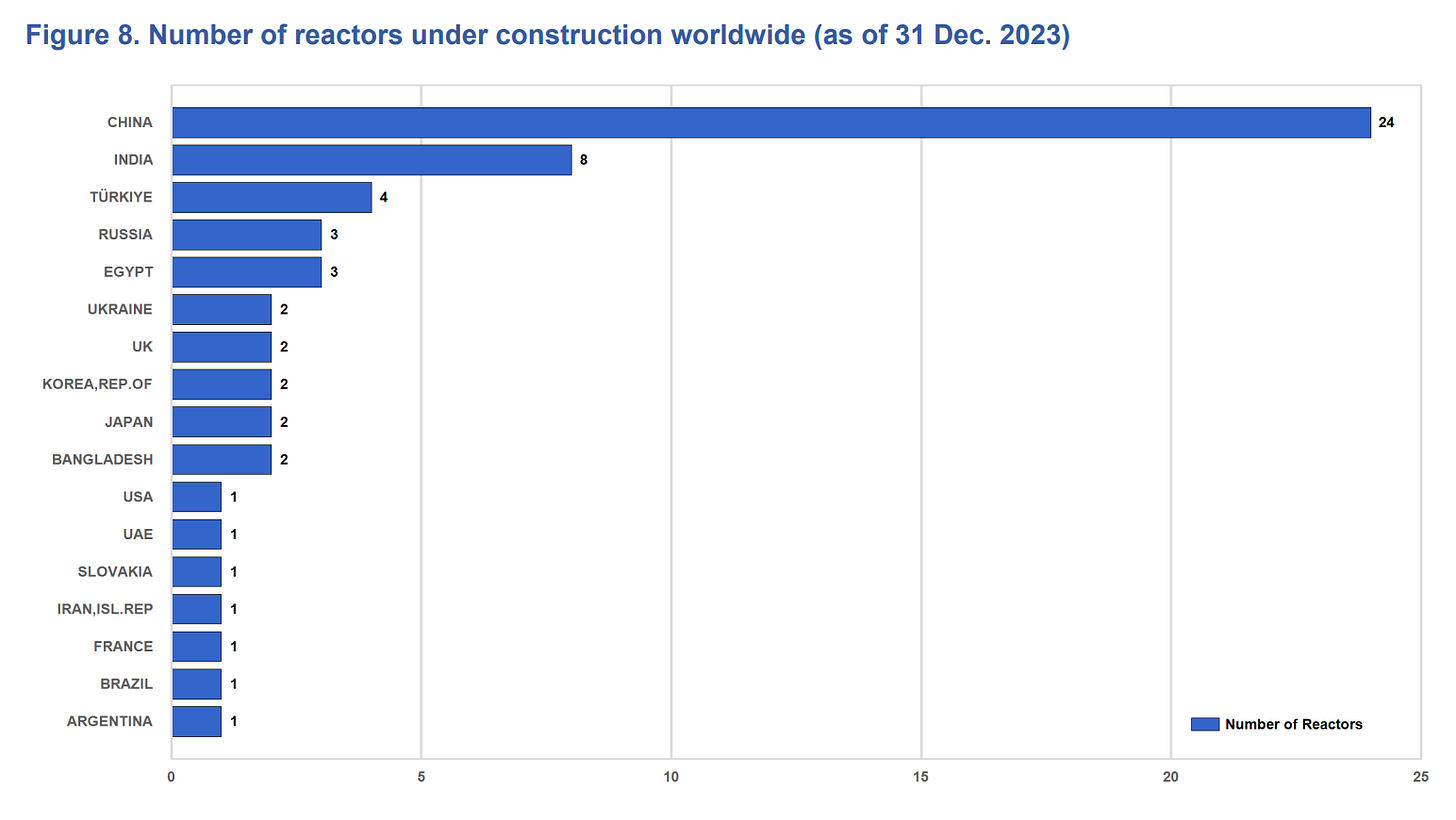

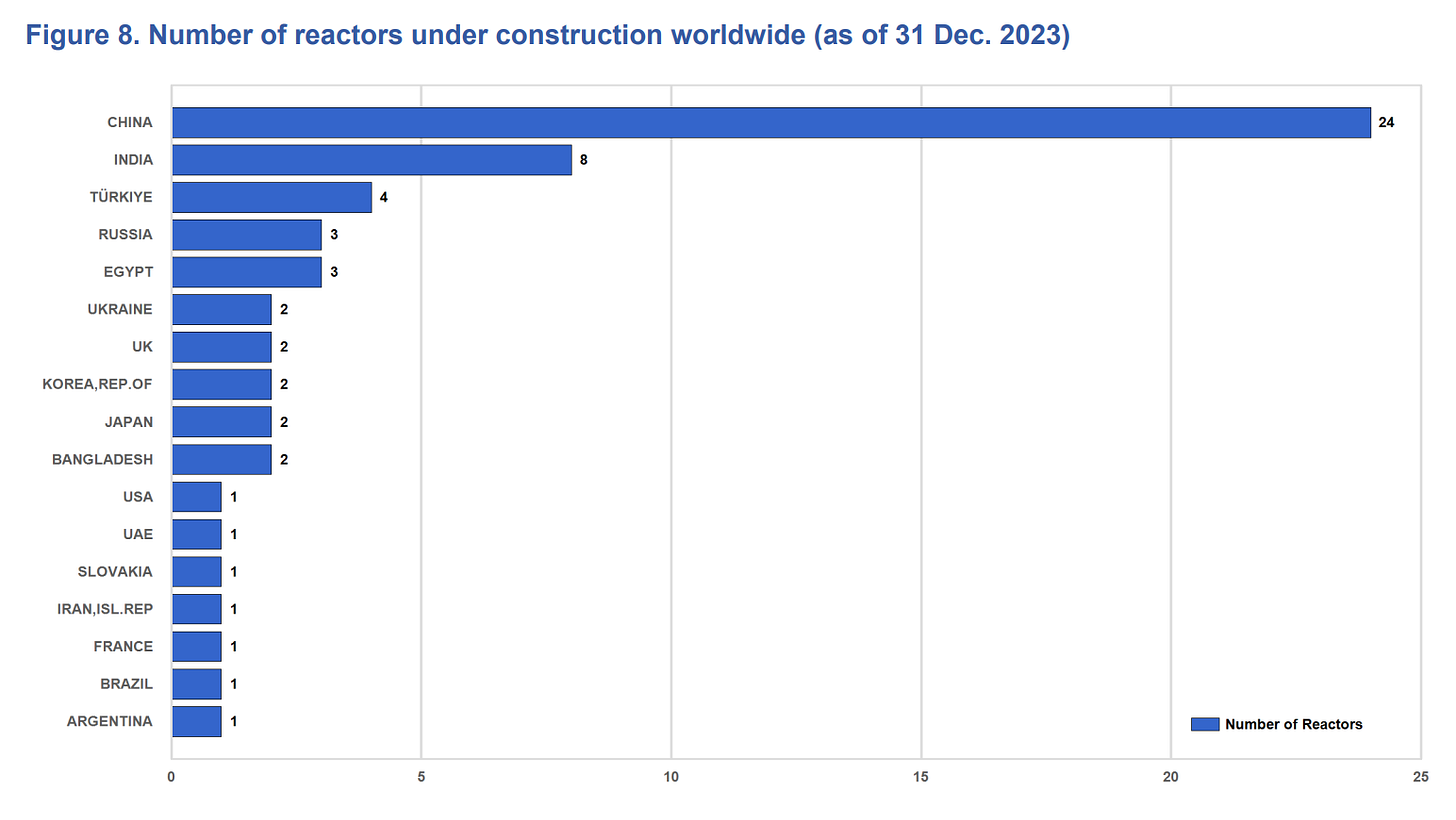

It comes from about 440 nuclear reactors with a total output capacity of about 400,000MW operating in 31 countries. About 70 more reactors are under construction and about 110 are planned.

Armenia, Belarus, Belgium, Bulgaria, Czech Republic, Finland, France, Hungary, Slovakia, Slovenia, South Korea and Ukraine all get 30% or more of their electricity from nuclear reactors. The USA has over 90 operable reactors, supplying 20% of its electricity. France gets about 70% of its electricity from uranium.

Over the 60 years that the world has enjoyed the benefits of cleanly-generated electricity from nuclear power, there have been about 18,500 reactor-years of operational experience.

The uranium used in this case is called Low Enriched Uranium, which contains a U-235 concentration between 0.711 percent and 20 percent. Most commercial reactor fuel uses low enriched uranium (LEU) enriched to between 3 percent and 5 percent U-235, sometimes referred to as reactor-grade uranium.

The West dominates nuclear energy & uranium consumption but China will be the biggest growth driver going forward

Whilst the West currently dominates nuclear energy & uranium consumption, China is expected to be the biggest growth driver in the next decade. Uranium demand is geographically diverse, though over half of the world’s nuclear power generation currently comes from the US (29%), France (13%), and China (16%).

But the rest of the world is looking to catch up, with divergent nuclear policies, regulatory frameworks, and growth strategies between nations, demand is increasingly shifting to China and India who are more aggressively expanding their nuclear fleet in the short-/medium-term. India + China’s share of global nuclear generation will double from 18% to 35% by 2035, driving 3/4 of demand growth in the next decade. The prospects globally of nuclear energy are bright with big investment pushes everywhere and decades of negative nuclear policies being reversed in many geographies.

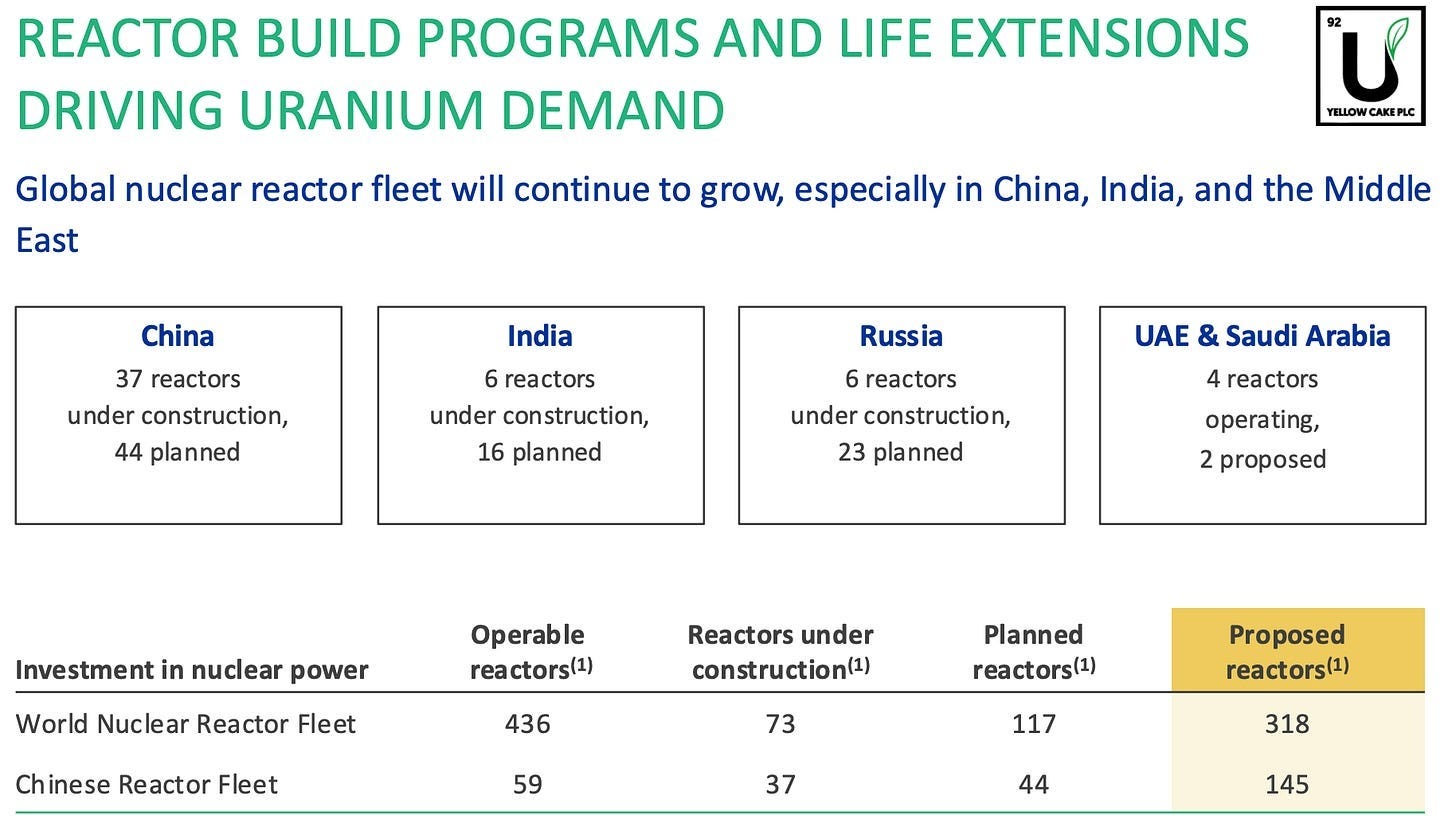

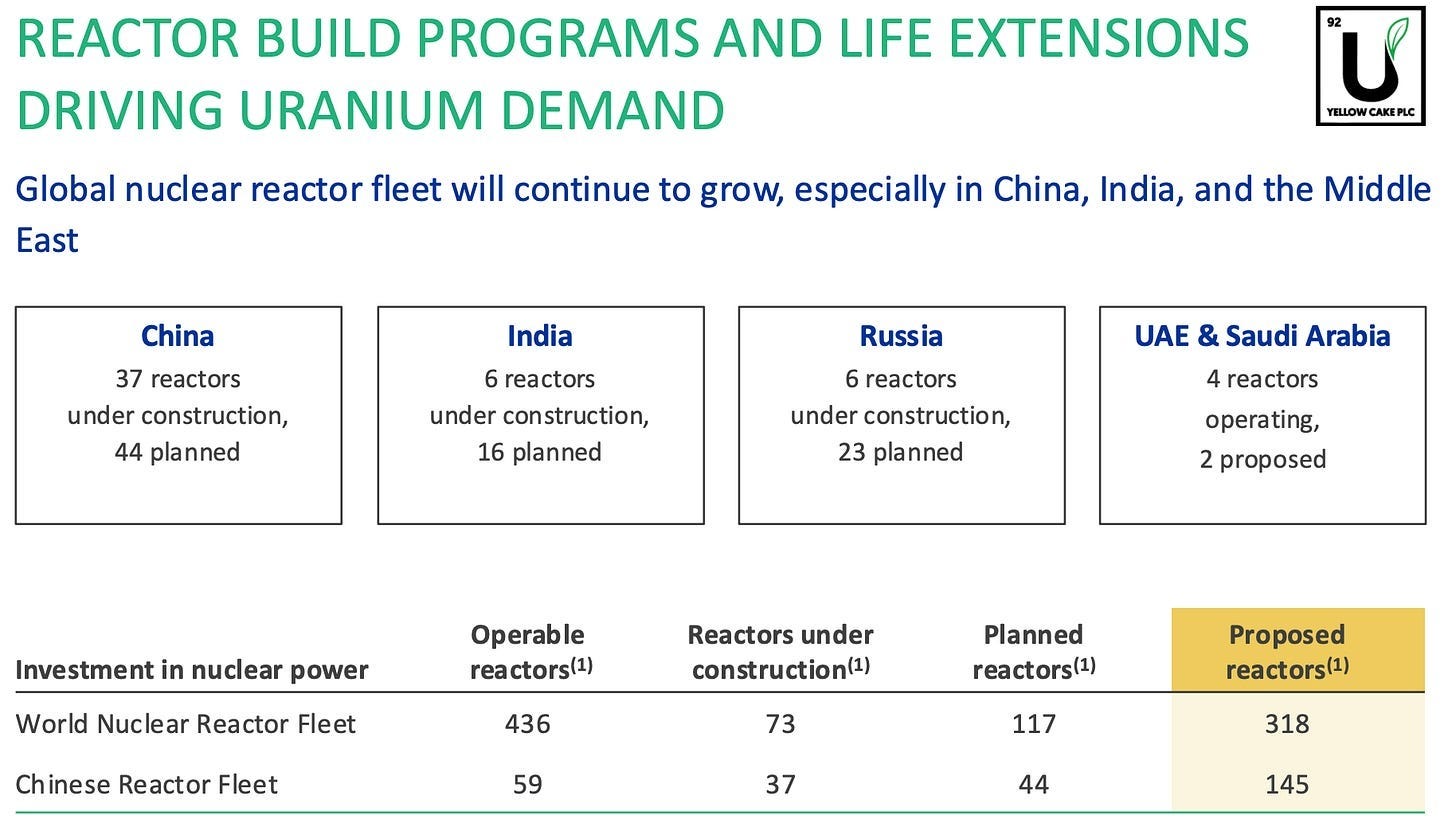

China - The rising nuclear powerhouse: China is expected to be the biggest demand growth driver in the next decade, with an ambition to grow nuclear capacity to 110-120 GW by 2030 (vs 60 GW currently). This translates into 12% CAGR to 2030, and 8% CAGR beyond as the new reactors consume more uranium in its initial cycle. Currently operating a nuclear fleet of 58 reactors, China has 33 reactors under construction and has been consistently adding 2-3 reactors per year. China should account for 1/3 of global nuclear capacity by the next decade.

India - Huge growth: India is expecting to grow nuclear capacity to 22.5 GW by early 2030s (vs 5GW currently). This translates into >5% CAGR to 2030, and 18% CAGR beyond in uranium demand.

North America - The start of a nuclear renaissance: The US currently has the world’s largest reactor fleet accounting for 29% of global nuclear capacity & Canada 3%. There are however no major capacity additions planned or new reactors in construction, and we can expect more aged plants being extended. Expect demand to be flat over the next decade, only accelerating in late 2030s/2040s from license extension and refurbishment as the current fleet ages. There is an increasing focus for US utilities to secure local/ allied uranium supply.

Europe - Finally a pro-nuclear inflection?: The state of nuclear power is divergent in Europe, with France accounting for 13% of global nuclear generation vs Germany having decommissioned its fleet. Europe is still a big nuclear continent with around 100 GW of nuclear capacity. Short term, there is some incremental demand from newbuilds in the UK (Hinkley Point C) and Eastern Europe, but this will not be a meaningful demand driver. Europe, like the US, is starting to pivot to more pro-nuclear policies with France again taking the lead on reversing the decline of its nuclear industry, but of course this will be very slow. France is planning a large nuclear revival built around six new EPR2 reactors by the late 2030s, with options that could take total new capacity to roughly 25 GW by 2050 and keep nuclear above 50% of its power mix.

Japan & South Korea - A return of nuclear?: Japan and South Korea have seen a policy & sentiment reversal in nuclear energy, with incremental demand from both restarts (in Japan following shutdowns after the Fukushima accident in 2011, including most recently the approval of TEPCO’s plant in early 2026) and newbuilds.

Middle East - Broadening adoption of nuclear: Across the Middle East, UAE’s four-unit plant is fully operational with plants being built in Turkey, Saudi Arabia, and Egypt amongst others with the technical support from other more technologically advanced countries.

The Nuclear Renaissance will happen in 3 phases:

Short-term renaissance: current reactors, the monopoly of time, immense beneficiaries from the rise of AI and surge in baseload power demand

Medium-term renaissance: expansion of reactor fleet, a second historical nuclear buildout & the rise of SMRs

Long-term renaissance: nuclear fusion, the ultimate form of energy

4. Phase I of the Renaissance: The AI Catalyst & The Monopoly of Time

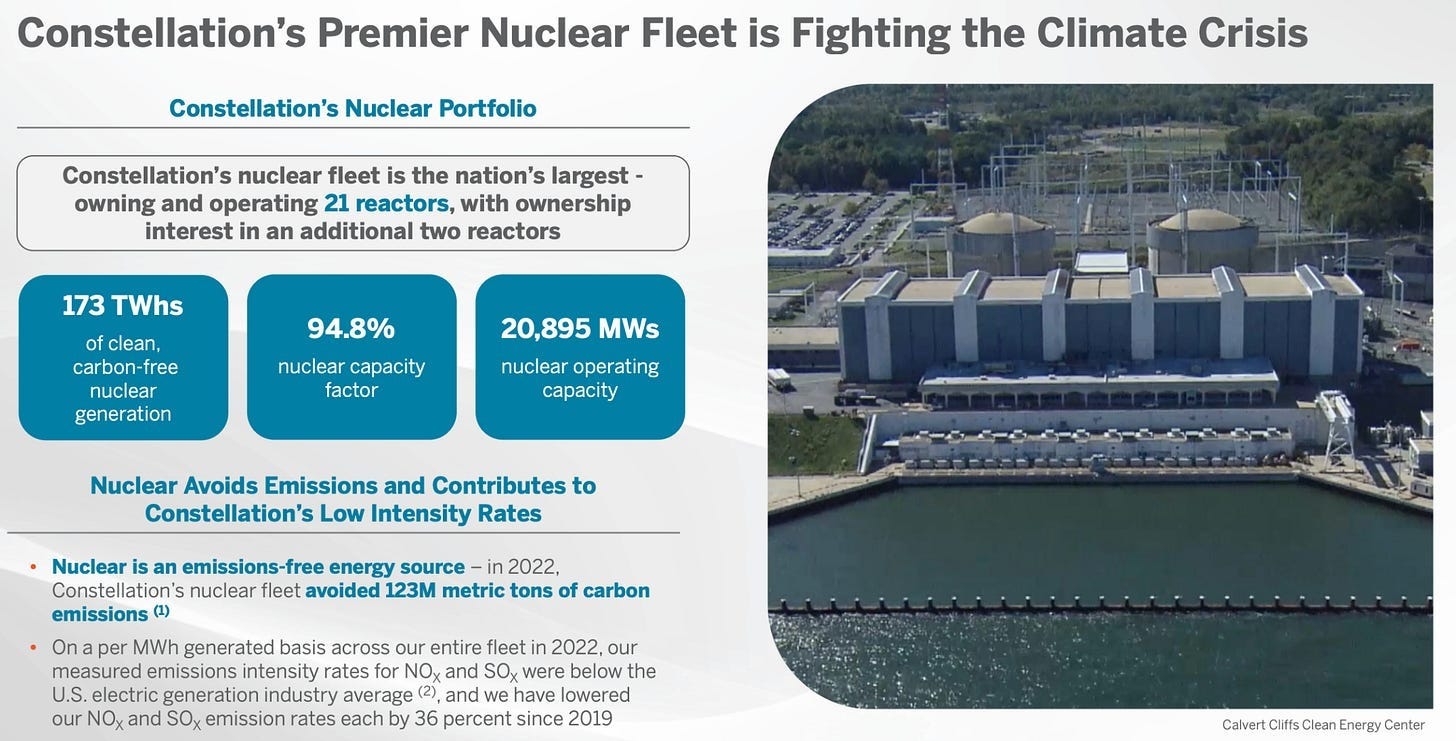

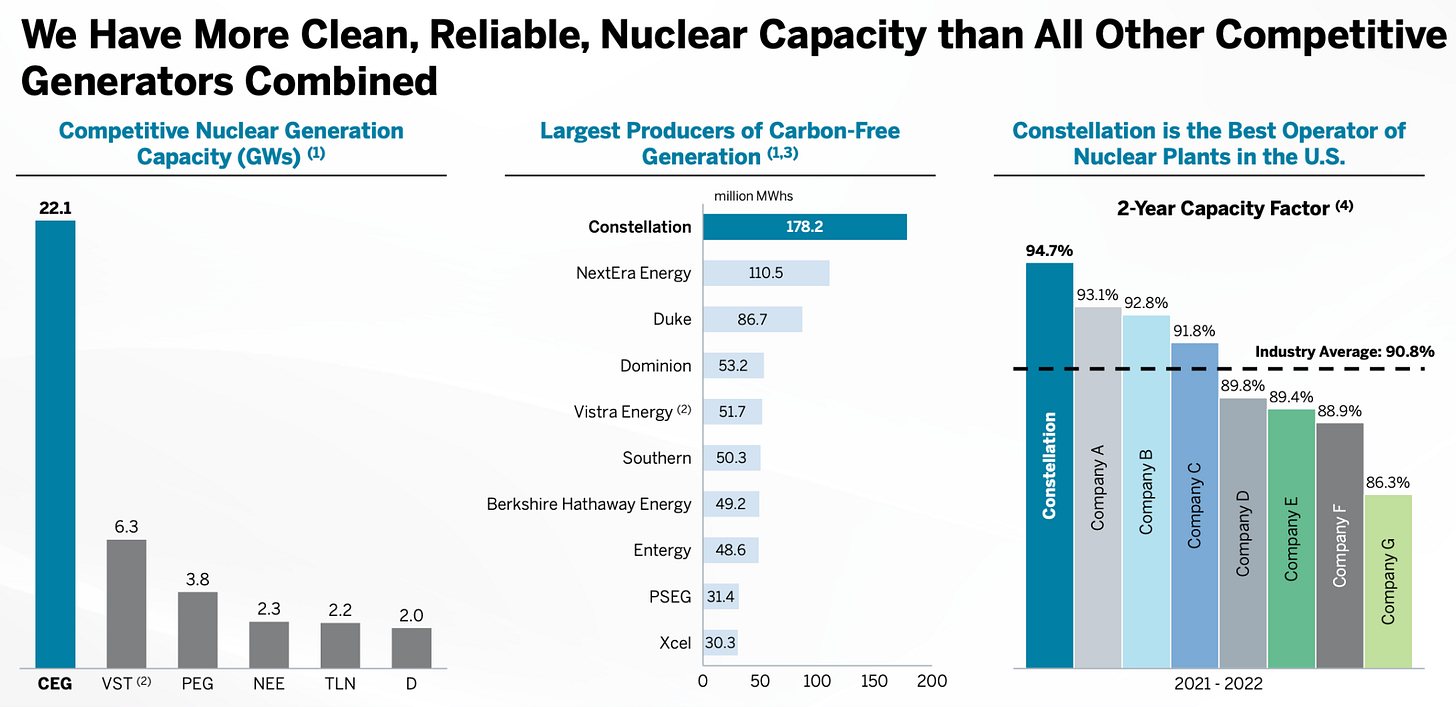

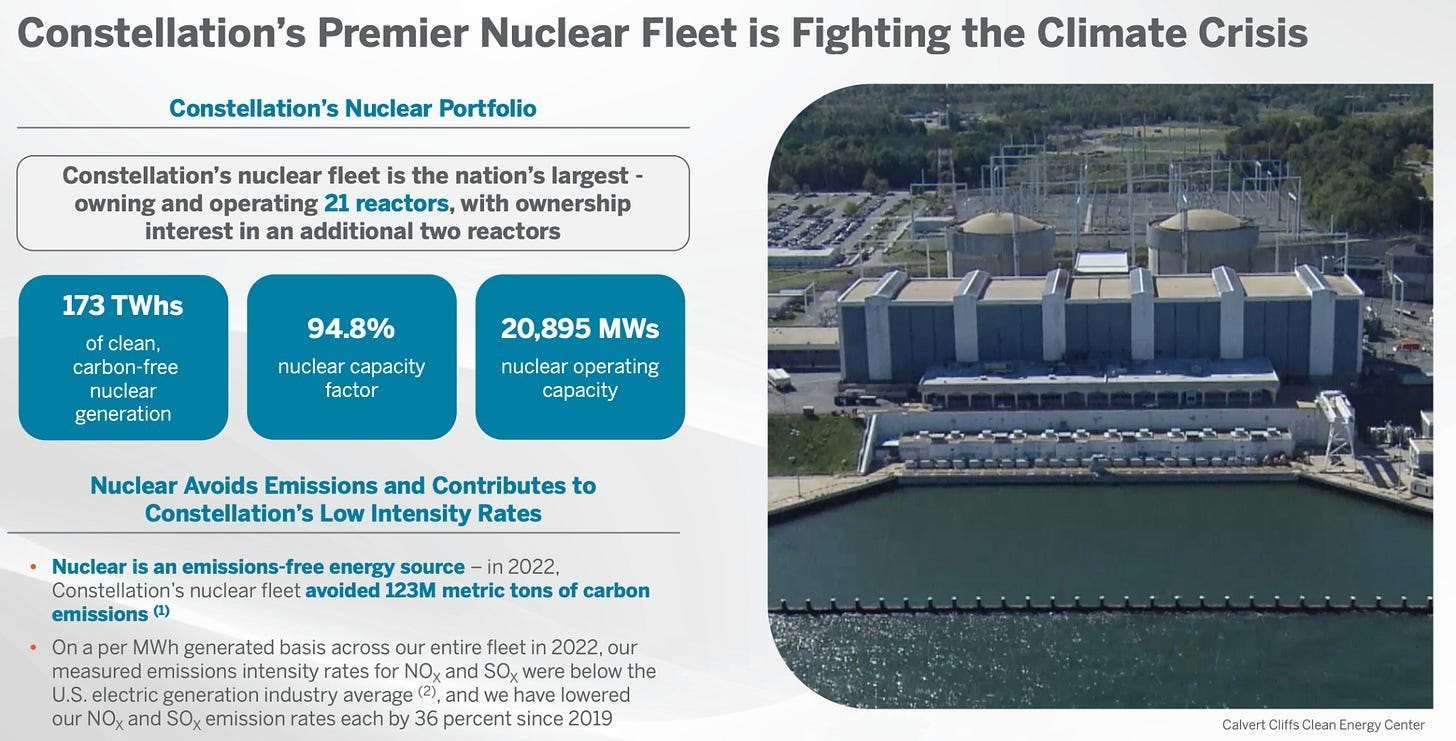

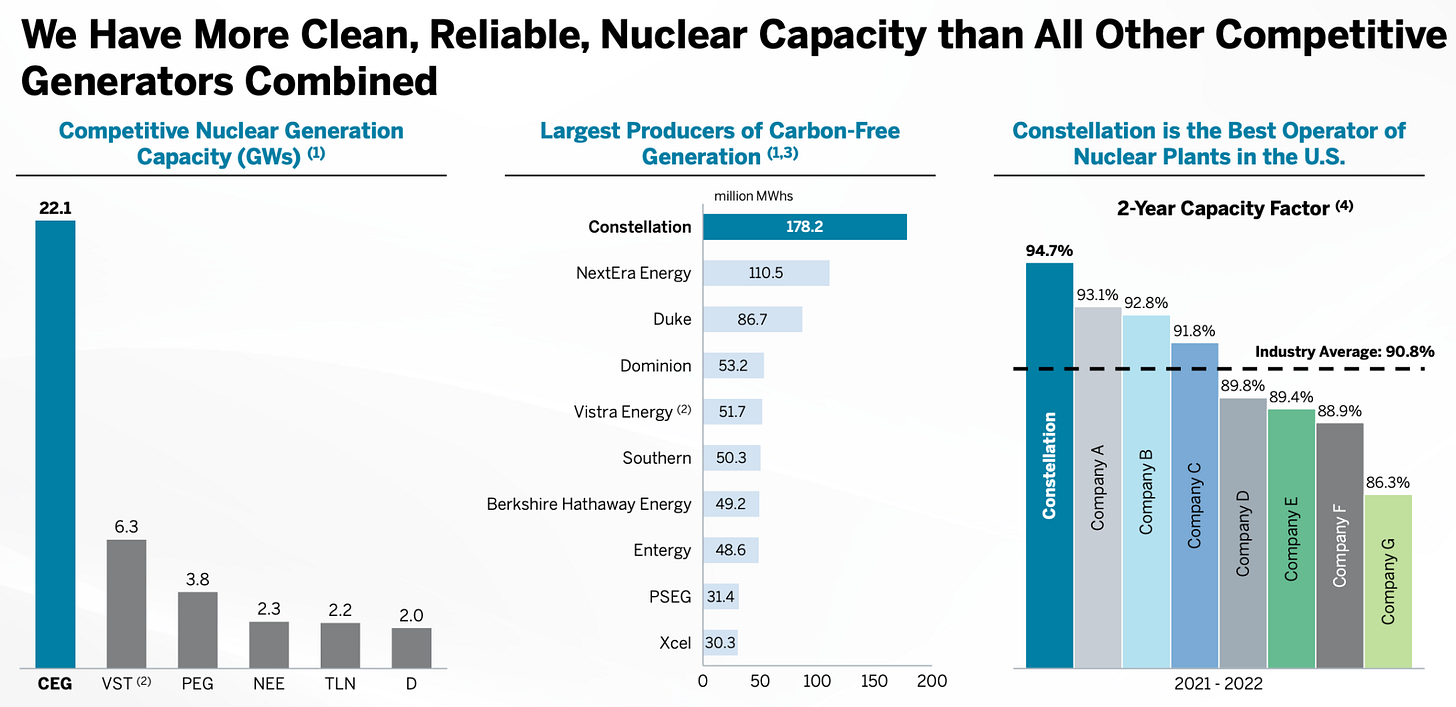

The first winners of this nuclear renaissance and scramble to secure baseload power generation are the incumbent nuclear operators, chief amongst them Constellation Energy.

Historical load growth inflection and acceleration linked to the Age of Electrification and AI data center boom:

Surging power demand growth tailwinds accelerate: During the early 2000s, US power demand stagnated as higher energy efficiency offset load growth from population and economic growth. However, trends across manufacturing onshoring, transportation/heating electrification, and data center growth, coupled with easier energy efficiency measures completed, have propelled accelerating growth in power demand. Utility large-load pipelines continued to increase over the year, and there are tightening reserve margins in PJM and ERCOT as read-throughs to significant generation build-out needs, as well as contracting opportunities for both nuclear and natural gas.

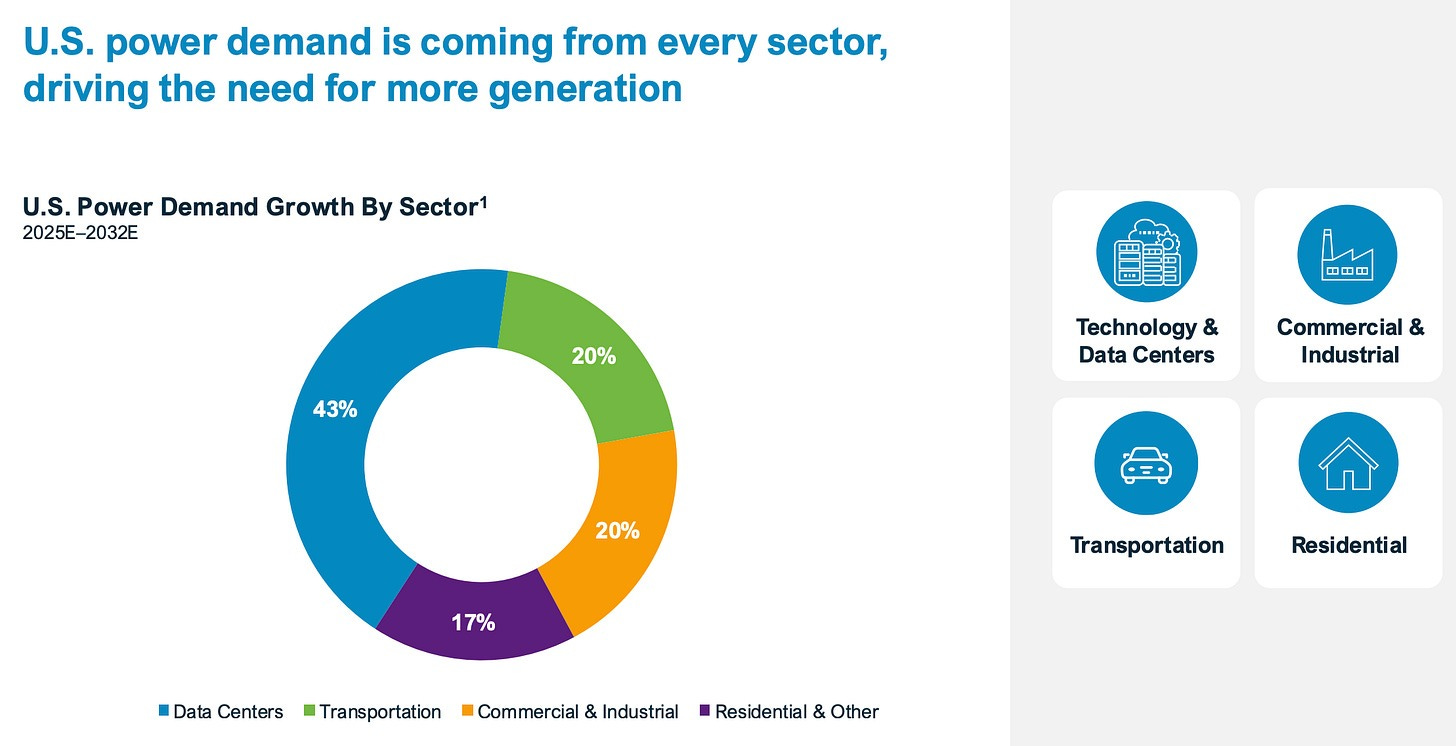

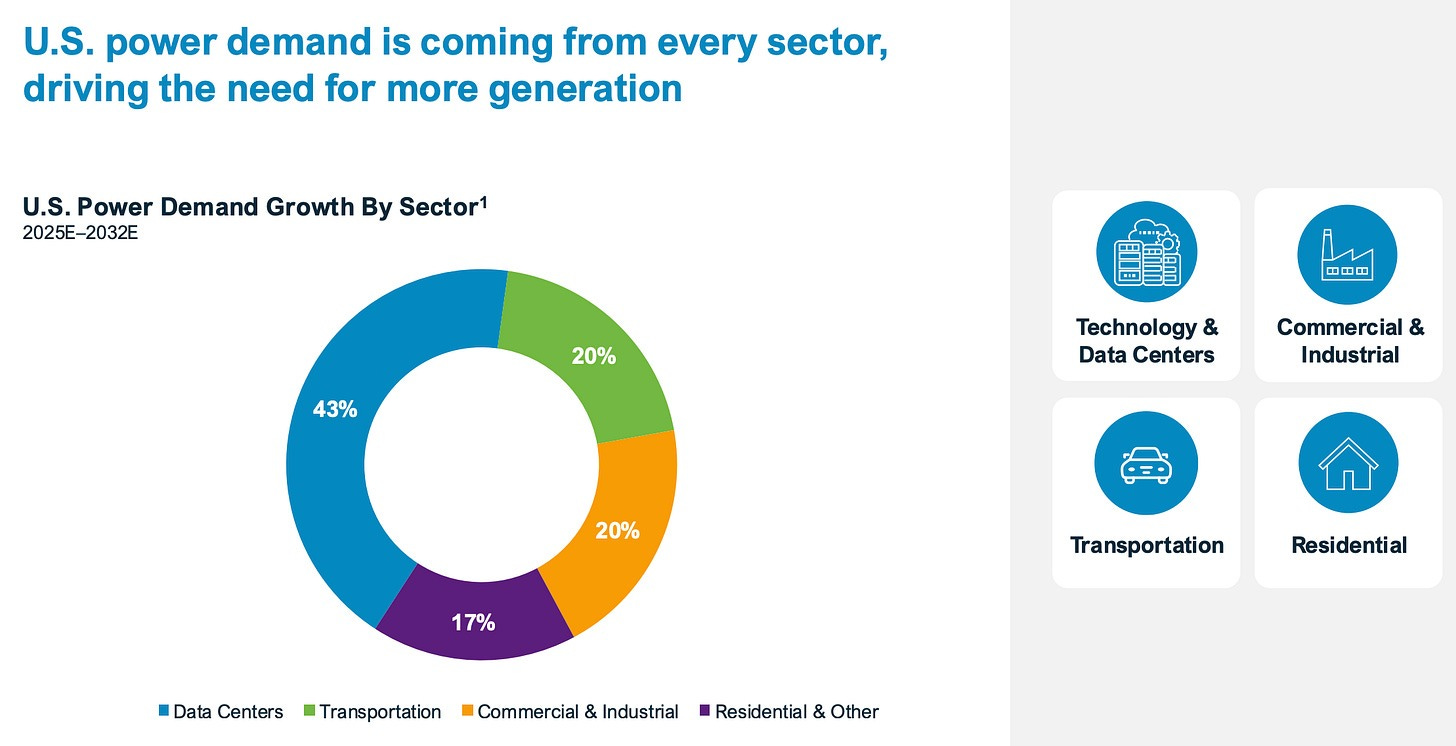

What’s driving the growth? Primarily, heating and industry electrification because they account for roughly 25% of new demand. Secondly, electric vehicles and data centers contribute another 20% each and finally green hydrogen which adds a final 20%, but this growth driver remains the most uncertain driver out of all of them.

According to the IEA and ICIS, data centers alone could add:

0.4–0.6% to Europe’s annual demand growth

1.0% in the US

Data centers have historically only modestly grown as a share of global electricity consumption rising only from 1% in 2005 to 1.5% in 2024, despite explosive growth in digital activity and internet usage, largely due to advances in energy efficiency. However, with most gains from consolidating enterprise data centers already realized, AI servers already highly optimized, and physical limits to further chip miniaturization approaching, future efficiency improvements are becoming more challenging.

As AI adoption accelerates, energy use by data centers is now set to surge: In 2024, data centers consumed about 415 TWh, or 1.5% of global electricity, but this is projected to more than double to roughly 945 TWh by 2030, driven mainly by generative AI, which will account for 41% of total data center demand by then, up from 16% today. While this will mean data centers make up about 3% of global power use by 2030, their contribution to total electricity demand growth will remain under 10%, less than sectors like industrial motors, air conditioning, or electric vehicles.

The impact will be uneven: in advanced economies, data centers are expected to drive over 20% of electricity demand growth to 2030, and in the US, their share of national electricity use could climb from 4% today to as much as 9% within a decade. In Ireland, data centers already account for 21% of electricity consumption. This concentration will put significant pressure on local grids, with the risk that up to 20% of planned data center projects could be delayed due to grid connection bottlenecks and infrastructure constraints.

So, while data centers’ global energy footprint will remain a relatively modest slice of total demand, the rapid expansion of AI is making their growth a key driver of electricity demand in many regions, raising new challenges for grid management, energy infrastructure, and generation and therefore opportunities for many companies providing solutions to those sectors.

The biggest constraint in the AI infrastructure race is not capital or silicon, it is time.

You cannot simply code or print a nuclear power plant into existence. In the Western world, building a new large-scale reactor is a bureaucratic and engineering ordeal that routinely takes 10 to 15 years from planning to commercial operation. The most recent US nuclear project, Vogtle Units 3 and 4, took roughly 15 years and ran $17 billion over budget, bringing the total cost to an astonishing $37 billion.

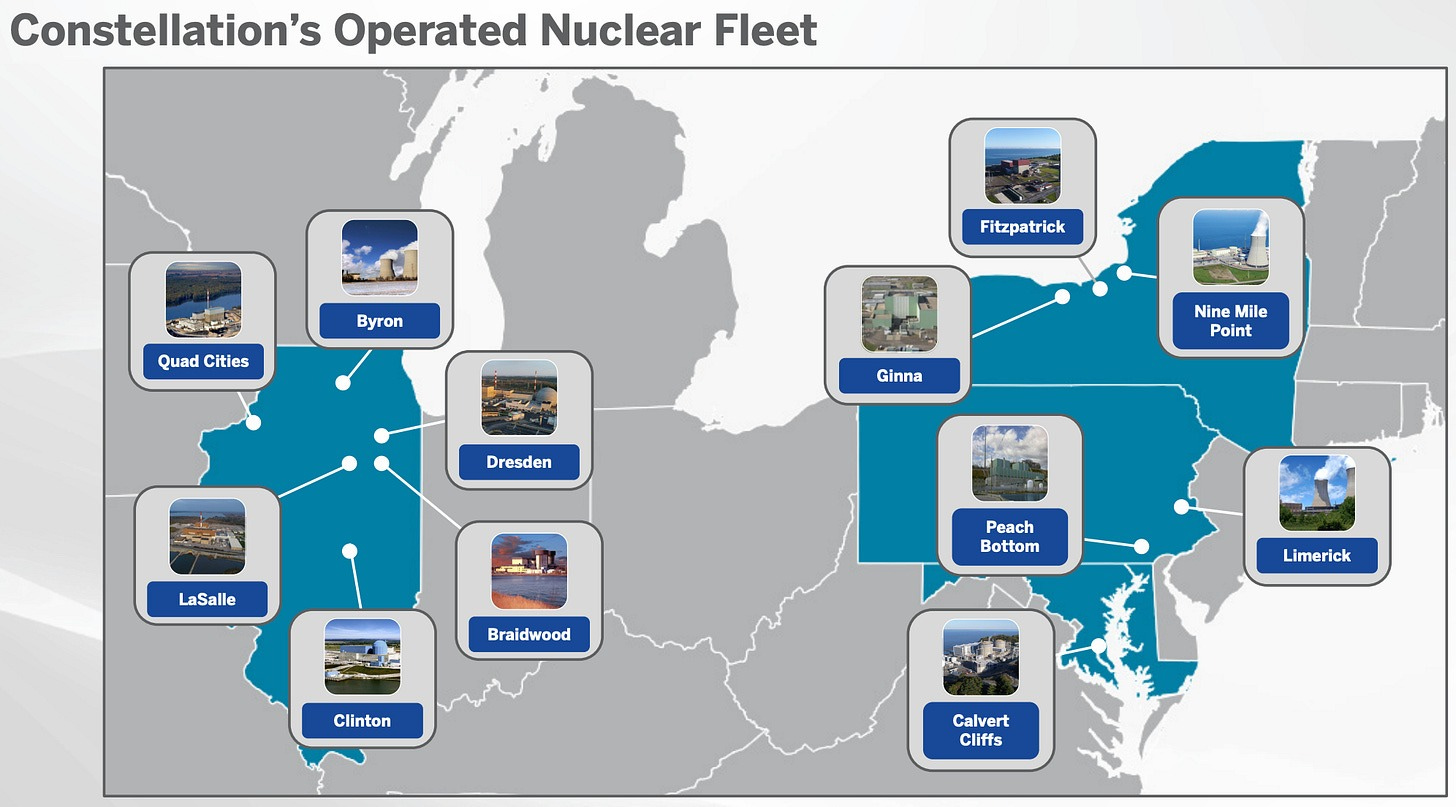

Because of this severe supply inelasticity, we are not going to build our way out of the immediate AI power deficit with new reactors. Therefore, Phase I of the nuclear renaissance relies entirely on maximizing the existing fleet.

This dynamic confers a Monopoly of Time to existing, established operators. Companies like Constellation Energy, which controls the largest unregulated nuclear fleet in the US with over 21 gigawatts of capacity, are the immediate winners. When a tech giant signs a Power Purchase Agreement (PPA) with an existing nuclear plant, they are not just buying commodities, they are effectively purchasing the 15 years of time that their competitors would need to replicate those assets.

To meet the surging demand before new reactor technologies commercialize in the 2030s, the nuclear industry is aggressively pulling three levers to squeeze every possible electron out of the current grid:

Plant Restarts: The most dramatic signal of the nuclear revival is the resurrection of decommissioned plants. Restarting a dormant plant is a complex engineering challenge, but it is vastly faster and cheaper than greenfield construction.

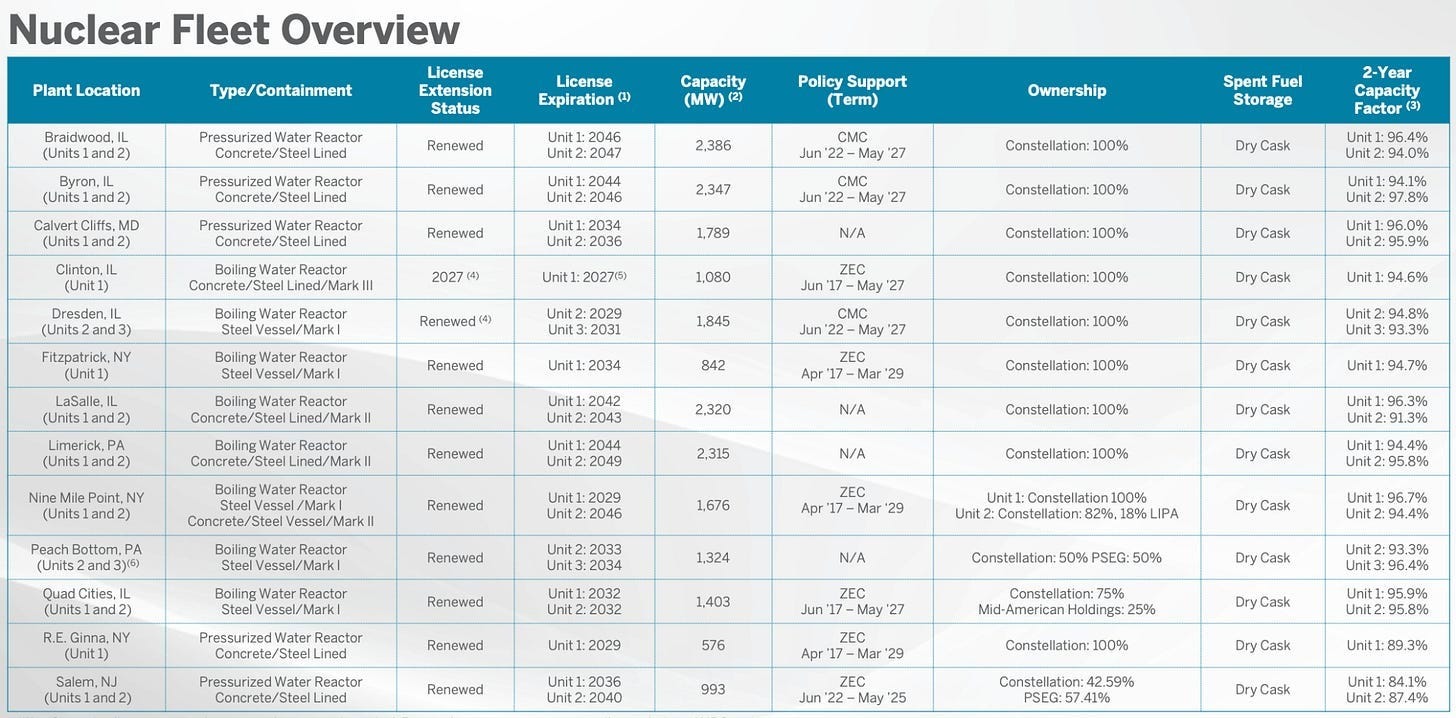

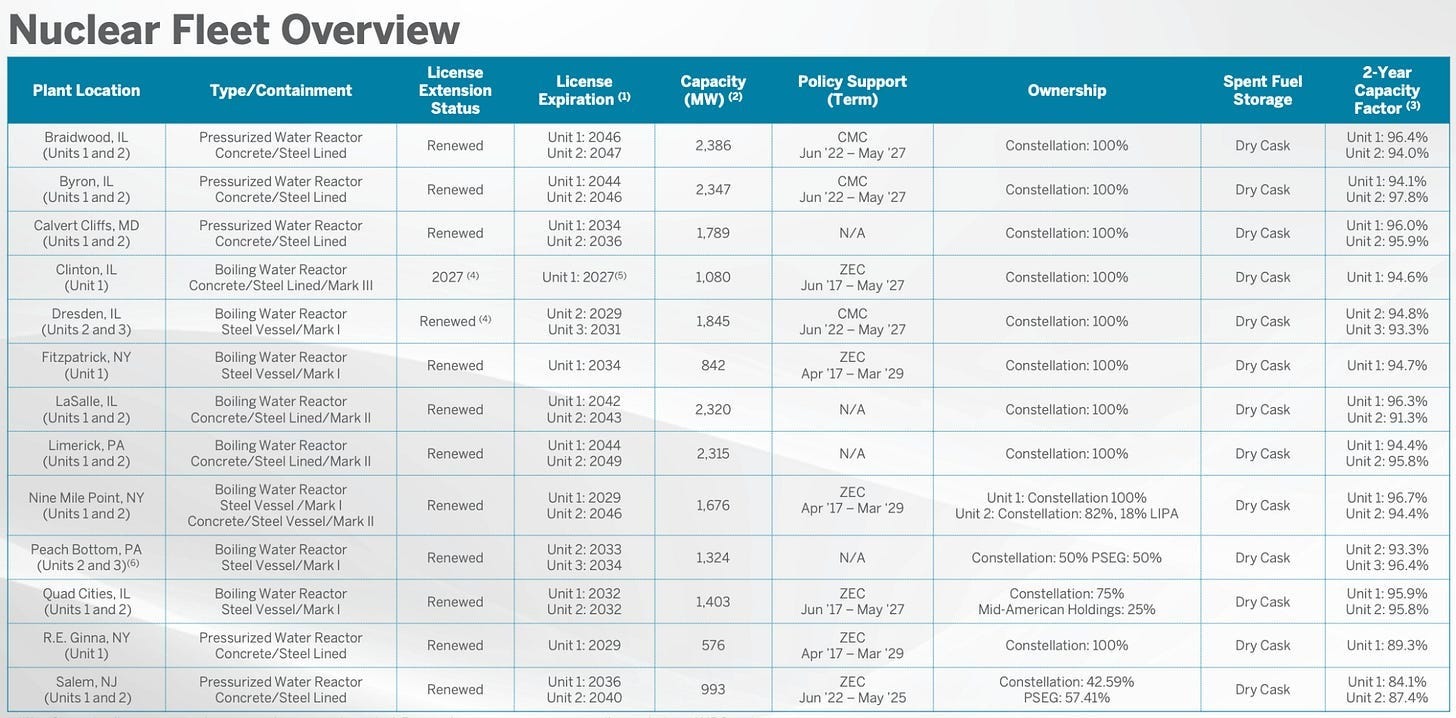

Three Mile Island: In September 2024, Microsoft signed a 20-year PPA to purchase 100% of the output from the retired Unit 1 reactor at Three Mile Island (now renamed the Crane Clean Energy Center). Constellation Energy is investing roughly $1.6 billion to bring the 835 MW plant back online by 2028, supported by a $1 billion loan guarantee from the US Department of Energy.

Palisades: Similarly, the US DOE finalized a $1.5 billion loan guarantee to restart the Palisades nuclear plant in Michigan, which had been shut down in 2022.

Capacity Uprates: An uprate is a highly cost-effective way to generate new power by upgrading the equipment inside an existing, operating reactor (such as replacing turbines or feedwater measurement tools). Constellation Energy is currently pursuing a 1 GW pipeline of uprates across its fleet. For example, the company is moving forward with $800 million in upgrades at its Braidwood and Byron stations in Illinois to squeeze out an additional 135 MW of capacity, enough to power 100,000 homes around the clock.

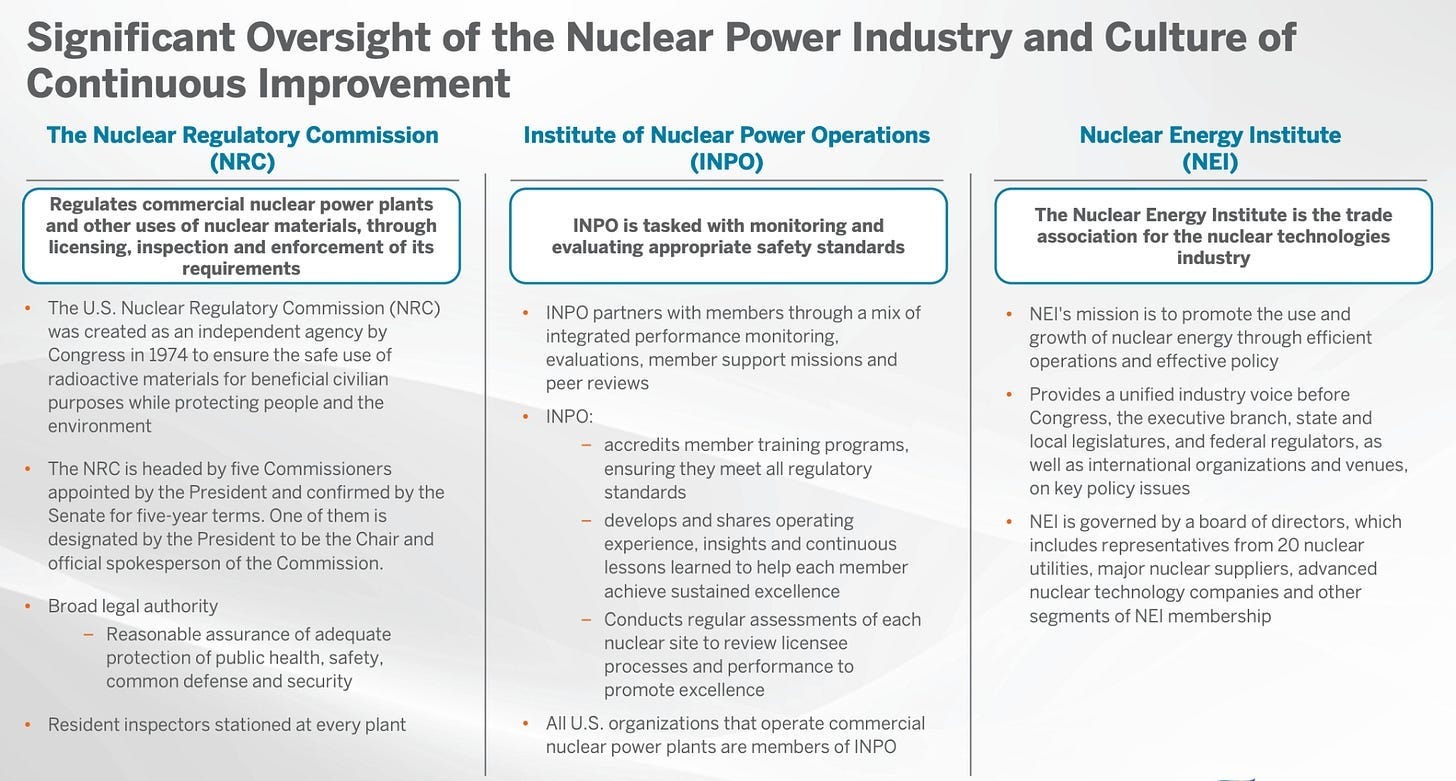

Subsequent License Renewals (Life Extensions) Nuclear plants were originally licensed to operate for 40 years, but the NRC allows for 20-year extensions. Today, the industry is aggressively pushing for subsequent license renewals (SLRs) to extend reactor lifespans from 60 to 80 years, effectively ensuring that the current baseload fleet remains a steady foundation for the grid through the mid-century. Recently, the NRC granted 20-year extensions for Constellation’s Clinton and Dresden units, supported by over $370 million in upgrades.

In this first phase of the renaissance, existing nuclear infrastructure has been structurally re-rated. These assets were once viewed as rusting, toxic liabilities of the industrial age today, they have been revealed as the scarcest, most critical infrastructure assets on the planet.

Historically, the utility sector was a sleepy, regulated cage. Power providers operated with capped profit margins, modeling predictable, low-single-digit load growth based on housing starts and modest industrial expansion. Today, that model has been blown apart by the arrival of a new, voracious buyer: the trillion-dollar technology hyperscaler.

We are witnessing an unprecedented surge in power demand driven by the electrification of the broader economy and the explosive growth of artificial intelligence. To put the sheer scale of this into perspective: data centers alone could consume more energy than the entire nation of Japan by 2026, and more than India by 2030. The computational intensity of AI means that a single ChatGPT query requires significantly more power than a traditional Google search, creating a demand shock that the legacy grid is simply not equipped to handle.

For companies like Amazon, Microsoft, and Meta, the calculus is simple. When you are building billion-dollar GPU clusters, the cost of electricity is a rounding error compared to the cost of the compute itself. However, the availability of uninterrupted, 24/7 power is the single biggest bottleneck to AI supremacy. If the power cuts out, the cloud shuts down.

This has completely inverted the pricing power dynamics of the energy market. Tech giants are effectively price-insensitive when it comes to securing clean, reliable baseload power. They have transformed electricity from a standard operating expense (opex) into a strategic, balance-sheet asset (capex). We have officially entered a Seller’s Market for electrons, and nuclear power, as the only zero-carbon, baseload energy source capable of 93%+ capacity factors, is the ultimate prize.

The Acquisition of Sovereignty

Three Mile Island in Pennsylvania stood for nearly half a century as the ultimate symbol of nuclear fear in the United States. When Unit 2 suffered a partial meltdown in 1979, it did not just destroy a reactor or bankrupt a company. It effectively froze the Western atomic industry for a generation. Capital fled the sector, engineers moved to software, and the public solidified a psychological barrier against the atom.

In September 2024, that narrative reversed polarity with a force that the global market is still struggling to price. Microsoft did not just sign a 20-year contract with Constellation Energy to restart Unit 1, now renamed the Crane Clean Energy Center. They executed an acquisition of physical sovereignty. The deal involves purchasing 100% of the 835 megawatts of output to power Artificial Intelligence data centers exclusively.

This transaction shatters the traditional utility model that has governed the sector for a century. Microsoft is not buying electricity as a commodity to light up offices or charge laptops. It is buying the mathematical certainty of continuity. It bought the guarantee that its processors will run 24 hours a day, 7 days a week, regardless of weather conditions, gas pipeline constraints, or global fossil fuel volatility.

When the news broke, Constellation shares soared and decoupled violently from the traditional utility sector (XLU). This was the precise signal Capital needed to reallocate. The market realized that a nuclear reactor in the 2020s is no longer a toxic liability or a legacy asset to be decommissioned. It is the scarcest infrastructure asset on the planet.

By securing the electrons directly at the source, Microsoft signaled that in the AI era, computing power is downstream of electrical power. Sovereignty is no longer about code or algorithms. It is about the physics that allows the code to run.

Without the base layer of energy, the application layer of intelligence cannot exist.

The Monopoly of Time

The mechanism driving this Nuclear Renaissance is a violent collision between Moore’s Law and the Laws of Thermodynamics. We are witnessing a mismatch of operational speeds that no policy can fix in the short term. Generative artificial intelligence demands an energy density that the current renewable-heavy electrical grid cannot provide. A single ChatGPT query consumes ten times more energy than a Google search. As models scale from training to inference, the demand for gigawatts of constant power, known as baseload, becomes exponential.

The chip density is increasing faster than the grid’s ability to dissipate heat and supply watts. Renewable sources like solar and wind are intermittent by nature. They produce energy only when the sun shines or the wind blows. For a 100 billion dollar data center cluster, intermittency is an unacceptable operational risk. You cannot train a frontier model if your power source fluctuates with cloud cover.

Batteries are not yet a viable solution for gigawatt-scale storage over long durations, the physics of energy density in lithium-ion simply cannot compete with uranium. The only energy source capable of delivering massive, carbon-free, climate-independent baseload is nuclear fission.

Here lies the moat for existing nuclear assets. Constellation Energy controls the largest nuclear fleet in the United States with 21 gigawatts of capacity. In the Western world, building a new nuclear plant is a bureaucratic ordeal that takes ten to fifteen years due to regulatory asphyxiation and supply chain atrophy. This creates an absolute supply inelasticity. You cannot code more nuclear plants into existence. You cannot print them.

Owning licensed, operational, and connected reactors today confers a monopoly on time. Constellation does not just sell commodities. It sells the fifteen years of time that its competitors would need to replicate its assets. In a race for AI supremacy, time is the only asset you cannot buy on the margin.

The Seller’s Market

The immediate financial impact appears in the inversion of pricing power. For decades, utilities were sleepy, regulated businesses. The government defined how much the company could charge households and capped profit margins to ensure social stability. It was a sector for widows and orphans, offering low risk and low returns, acting more like a bond than a stock. Constellation’s business model has successfully migrated from this regulated cage to the corporate free market.

In this new model, Constellation signs direct Power Purchase Agreements (PPAs) with Big Tech firms, known as Hyperscalers. The buyer profile has shifted from the ratepayer to the trillion-dollar capex spender. Companies like Microsoft, Amazon, and Google hold massive cash reserves and gross margins above 60%.

For them, the price of electricity is relevant but secondary. The cost of energy represents a minor fraction of the total operating cost of an Nvidia H100 GPU cluster. The hardware is so expensive that leaving it idle due to power shortages is financial suicide. The opportunity cost of not running the model dwarfs the premium paid for the electron.

However, the lack of energy costs the business its existence. If a Hyperscaler cannot secure power, they cannot deploy chips. If they cannot deploy chips, they lose the AI race to their competitors. This creates the ultimate Seller’s Market. Constellation can charge a significant premium over the wholesale price of electricity because it offers two attributes that exist nowhere else: immediate physical scale and a zero-carbon certificate.

The nuclear electron has undergone a structural re-rating. It is now priced as a high tech input rather than a domestic service. The dynamic is no longer utility cost plus, it is value based pricing for survival.

Structural Signals

The signals of this shift are not speculative. They are verifiable, redundant, and appear on multiple fronts simultaneously. The checklist of evidence confirms the movement is underway and gaining momentum:

The Price Signal: Constellation (CEG) shares gained over 100% in 12 months. It widely outperformed the traditional utilities index (XLU) and tracked the aggressive pace of the Nasdaq. The market is treating it as a growth stock, signaling that investors see it as a technology derivative rather than a utility. The correlation has shifted from interest rates to AI CAPEX.

The Corporate Signal: Amazon purchased a data center campus from Talen Energy located directly at the Susquehanna nuclear plant for 650 million dollars. They bought it primarily for the interconnection rights and validated the co-location thesis as a standard industry practice. This proved that the premium is real and that Big Tech is willing to pay for physical proximity.

The Regulatory Signal: The US Department of Energy finalized a 1.5 billion dollar loan guarantee to restart the Palisades nuclear plant in Michigan. This confirms that state support has shifted from tolerating nuclear to actively financing the recovery of the existing fleet. The government is now a stakeholder in the restart, reducing political risk.

The Political Signal: Support for nuclear energy has become the only bipartisan issue in the US Congress. This is evidenced by the overwhelming passage of the ADVANCE Act to accelerate the licensing of new reactors. Democrats want decarbonization. Republicans want energy dominance. Nuclear delivers both, creating a rare political safe harbor.

The Physical Signal: Winter and summer peak demand on the PJM grid hit historical records. This forced the operator to drastically increase capacity payments. This direct cash injection benefits reliable nuclear generators while penalizing intermittent sources that fail during extreme weather. The grid is paying a premium for reliability.

Energy as a Balance Sheet Asset

The structural implication of this movement is the merger between the Energy and Computing sectors. Historically, these were separate industries with little overlap. Energy was merely a passive operating cost on a tech company’s P&L. Now, power generation capacity is becoming a strategic balance sheet asset. It is moving from opex to capex.

We are moving toward a world where Tech companies will acquire equity stakes in power generators or directly finance the construction of Small Modular Reactors (SMRs) to secure their future. This is a trend already signaled by Google and Oracle. They are realizing that without owning the generation, they do not own their destiny. The cloud is not free floating, it must be tethered to a power plant. If you do not own the electron, you rent your survival from someone who does.

For Constellation, this means predictable, inflation-indexed cash flows for decades. These flows are backed by the strongest counterparties on earth. The company positions itself as the “Federal Reserve of the Electron”. It issues the base currency of clean, firm power that underpins the entire digital economy. This alters competition between nations.

Countries with robust, deregulated nuclear fleets will hold a competitive advantage in attracting data centers and developing sovereign AI models. Those without stable electrons will lose digital sovereignty. The electron is the new reserve currency of the digital age, and Constellation controls the printing press.

The Return of Heavy Industry

In the long term, Constellation Energy represents the first phase of a new era of heavy industrialization in the United States. The digital world has discovered it possesses a hungry physical body. For two decades, electricity demand in the US stagnated due to efficiency gains. That era is over. We have returned to rapid, hard growth driven by chips, factories, and electrification.

The answer to this demand will not come solely from solar panels or batteries. It will come from robust thermal infrastructure. Constellation acts as the necessary bridge between the fossil fuel present and a fusion or SMR future that is still decades away from commercial scale. Over the next twenty years, the existing nuclear fleet will be extended to operate for up to 80 years.

These assets were once viewed as rusting dinosaurs of the industrial age. They have been revealed as the energy cathedrals of the 21st century. They are the only machines capable of allowing the synthetic mind to exist. We are seeing a return to the physical.

The code is important, but the generator is essential. The valuation of the digital world is being re-anchored to the physical constraints of the real world. Constellation’s value lies in a simple, brutal physical truth: without the atom, the cloud shuts down.

The Corporate Land Grab

This realization has triggered a frantic corporate land grab, with Big Tech bypassing traditional utility procurement models to sign massive, long-term Power Purchase Agreements (PPAs) directly with nuclear operators.

The corporate signals are undeniable:

The return of Three Mile Island, Unit 1 and the start of the AI/nuclear power bonanza:

Nuclear is finally back: In late September 2024, CEG announced that it will restart Unit 1 at the Three Mile Island (TMI) nuclear facility, providing the resulting output over the grid to a Microsoft data center under a 20-year power purchase agreement (PPA). Three Mile Island (renamed the Crane Clean Energy Center) is a two-unit facility: Unit 1 was shut down in 2019 for economic reasons, while Unit 2 was shut down in 1979 following an accident and is currently being decommissioned by its owner, Energy Solutions. This restart will cost approximately $1.6bn (including fuel), with the plant scheduled to re-enter service in end 2027/2028.

To restart Unit 1 CEG will require Nuclear Regulatory Commission (NRC) approval following a safety and environmental review, as well as permits from state and local agencies. As a separate process before the NRC, Constellation will pursue a license extension that will allow the plant to run through at least 2054.

How much is Microsoft paying? A lot: While CEG did not disclose the financial details of the supply contract, it did highlight that the company’s base earnings growth will increase from 10% to 13% over the 2024-2030 period, that the project exceeds its double-digit return threshold, and that it qualifies for the 45Y new nuclear tax credit. This likely means that Microsoft is paying $110/MWh.

Amazon’s Behind the Meter Move: Amazon validated the “co-location” thesis by purchasing a data center campus directly from Talen Energy at the Susquehanna nuclear plant for $650 million. By building right at the source of the generation, Amazon secured physical proximity and critical interconnection rights.

Meta also going nuclear: June 2025 - 20 years with Meta: CEG announced a twenty-year virtual power PPA with Meta for the output of its single unit reactor 1,121MW Clinton starting in June 2027. The timing aligns with the end of Illinois ratepayer subsidies zero emission credits (ZECs). The PPA covers a small incremental 30MW uprate. Meta will not be building a data center on-site. Pricing was not disclosed, but CEG guided to $80-88/MWh for a front-of-the-meter transaction with Q1 25 earnings.

In early 2026, Meta doubled down, announcing deals with advanced nuclear developer Oklo and existing operator Vistra to support up to 6.6 GW of new and existing nuclear generation for its data centers by 2035.

The message is clear: the tech industry has realized that the code is important, but the generator is essential. The valuation of the digital world is being re-anchored to the physical constraints of the real world.

5. Phase II of the Renaissance: Building the Future & The Rise of SMRs

Nuclear energy currently accounts for 9-10% of global electricity generation thanks to 440 operating nuclear reactors globally producing >2,500 TWh of electricity per year. There are a further 70 reactors in construction, as well as further incremental support from restarts and life extensions.

While Phase I of the nuclear renaissance is all about maximizing the existing fleet to meet immediate AI and electrification demand, Phase II requires putting shovels in the ground. To truly expand the grid for the decades ahead, the industry is pursuing two parallel tracks: building next-generation gigawatt-scale megaprojects and commercializing Small Modular Reactors (SMRs).

Massive push for nuclear worldwide

In the last few months, driven by AI data center needs for clean dispatchable power, the world has seen a slew of announcements for nuclear power in the US and many other countries across the world. IEA estimates for installed nuclear long term have increased by 40% in the last 5 years. The US alone is now targeting 400GW of nuclear power by 2050, India 100 GW by 2047 (for reference, the total global installed base of nuclear power at present is 420 GW).

Large-Scale Reactors and the AP1000 Standard

For large-scale baseload generation, the industry is coalescing around a standard design: the Westinghouse AP1000. It has emerged as the go-to US reactor design. The AP1000 boasts a highly compact footprint, requiring just over 3,000 square meters, compared to legacy designs that require over 10,000 square meters, and requires fewer components, which reduces maintenance and increases operational performance.

However, the economics of large conventional nuclear plants rely heavily on economies of scale, and these megaprojects have historically been plagued by massive financial risks. The most recent US AP1000 project, Vogtle Units 3 and 4, took roughly 15 years to complete and cost a staggering $37 billion. Europe’s Hinkley Point C has similarly seen costs and timelines balloon.

To overcome this First-of-a-Kind premium and de-risk construction, governments are stepping in aggressively. Recent US executive orders have explicitly targeted the reinvigoration of the nuclear industrial base, setting a goal to have 10 new large reactors under construction by 2030. Furthermore, countries like Poland and Bulgaria have officially selected the AP1000 for their upcoming nuclear expansions. For equipment suppliers and engineering firms, these large reactors represent an incredible moat: once a plant is built, it provides 60 to 80 years of locked-in, recurring revenue for specialized parts and maintenance.

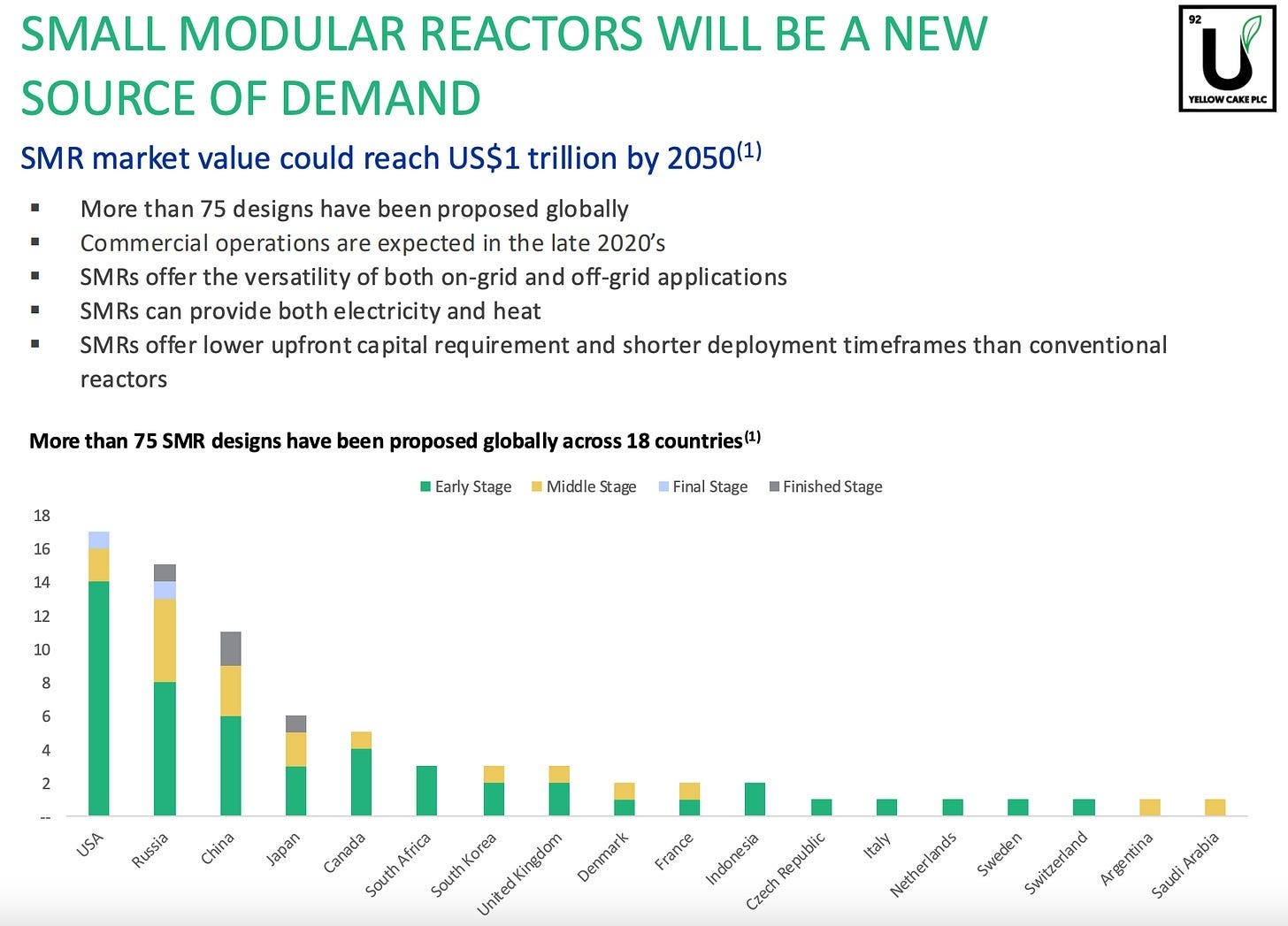

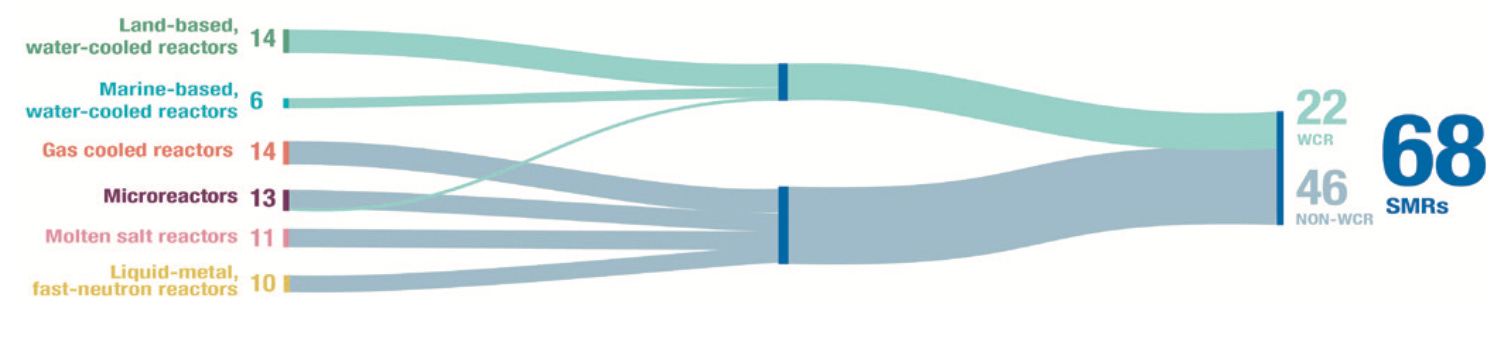

The rise of SMRs

Small modular reactors (SMRs) are re-inventing nuclear power.

SMRs are defined as reactors with a capacity of 300 MW or less. If large reactors rely on economies of scale, Small Modular Reactors aim to revolutionize the industry through economies of multiples.

They are made from individual pieces called modules, which can be mass-produced, transported separately, and assembled into a fully functioning, miniature power station. Theoretically, they are cheaper, faster, and simpler to build than traditional megaprojects (3 years construction time estimated vs 9 years as discussed above for traditional nuclear power plants), and can be built commercially on site within AI data centers and industrial parks.

SMR technology is now at an inflection point after years of stagnation, pushed by the historical load growth seen in the US in the context of the AI infrastructure supercycle, electrification and reshoring. SMRs are clearly moving from concept (more than 75 designs have been proposed) to execution (with commercial operations starting in the late 2020s).

To give a sense of the current hopes, some analysts estimate that the SMR market could reach $1tn by 2050. But the sector is seeing a real momentum. The Department of Energy has put real money behind the sector, with $900m in federal cost-sharing to support first SMR deployments, including projects with TVA and Holtec and strong backing for designs like GE Hitachi’s BWRX-300. At the policy level, streamlined licensing efforts at the NRC and bipartisan support in Congress are helping many projects see the light of day. Commercially, momentum is accelerating as utilities, states, and hyperscale power buyers look to SMRs to meet rising electricity demand, evidenced by TVA’s multi-GW SMR ambitions and growing interest from Big Tech in nuclear offtake (Constellation/Microsoft, Amazon, Google, & Meta to name a few high-profile examples).

It is important to remember that SMRs are still only getting off the ground, with deployment likely in the 2030s. Whilst there are >80 commercial designs across the world, only two are in operation today. By the 2030s, SMRs could:

Add incremental demand beyond the current nuclear fleet, though likely only <10% of total demand.

Provide customer diversification and fragmentation beyond the utilities.

Create greater enrichment demand and tighten fuel cycle capacity, as some advanced designs make use of high-assay low-enriched uranium (HALEU) that would require higher SWU per unit of uranium (meaning more effort required to separate uranium isotopes).

What are the catalysts for the SMR space?

There is likely to be an acceleration of catalysts across the SMR landscape in 2026. Investors will of course remain focused on the race to commercialize the technology. It is worth monitoring the progress of the DOE’s reactor pilot programs which include 10 companies which were selected for expedited reactor development. This program targets at least 3 SMR projects achieving criticality by July 4th 2026. Progress on SMR fuel supply chains will likely be a catalyst in 2026 as the scarcity of the HALEU supply chain has spurred investor doubt on the commerciality of some new designs. The EU Commission’s Industrial Alliance expects to publish its Strategic Action Plan in the first half of 2026, with the goal of outlining licensing standards, supply chain frameworks, additional R&D clarity and potential funding to accelerate Europe’s SMR strategy. Progress for specific company design licenses should be a key catalyst heading into 2026.

The US Department of Energy and private capital are pouring billions into this space to move these designs from First-of-a-Kind (FOAK) to Nth-of-a-Kind (NOAK) economics. While there are over 80 commercial SMR designs in development globally, a few major Western players are leading the pack:

NuScale Power (VOYGR): The first and only SMR design to receive official approval from the US Nuclear Regulatory Commission (NRC).

GE Vernova Hitachi (BWRX-300): A boiling water reactor design slated for deployment in Canada, Poland, and the UK by the late 2020s.

TerraPower (Natrium): Backed by Bill Gates and the US DOE, this sodium-cooled fast reactor recently submitted its construction permit application for a site in Wyoming.

X-energy (Xe-100): A high-temperature gas-cooled reactor that recently secured a massive $500m equity investment from Amazon to deploy up to 5 GW of capacity.

In 2020, the US DoE launched the Advanced Reactor Demonstration Program (ADRP) and selected two companies, Terra Power and X- Energy under the program to receive funding support by the DoE:

TerraPower:

Recently passed the final safety evaluation done by NRC. While the construction permit has not been received yet, NRC mentioned that they did not find any safety issues that could prevent them from issuing the construction permit soon. NRC completed the evaluation a month ahead of the 18-month. period deadline. Terra Power has already started the non-nuclear construction at their project site in Wyoming since June 2024. The next step for Terra Power, once they receive the final construction permit, is to apply for an operational permit. The company plans its first nuclear-related concrete pour by 2027, load fuel by 2030, and enter commercial operation by 2031 as per a recent press article.

Meta has signed an agreement with Terra Power which appears to be more of a funding agreement for the development of the reactors (2 units) with the right to procure energy (rather than a traditional power off-take agreement). It remains unclear as to who (Meta or Terra Power) would take on the risk of the cost and time overruns or how binding this agreement is.

X-energy: