STMicroelectronics: Photonics, Satellites and Silicon Carbide

From cyclical bottom to AI structural story: the European IDM repositioning around silicon photonics, LEO satellites and silicon carbide

Welcome to the 71st investment case, 11th China, 26th Electrification & Energy, 33rd AI & Technology idea on Crack the Market (and the most comprehensive STMicroelectronics investment case you will find online)! The transition to AI data centers, electrified and software defined vehicles, smart industries and low Earth orbit connectivity will require far more specialised silicon than the market appreciates, and STMicroelectronics has quietly repositioned itself from a low quality consumer analog cyclical into one of the purest ways to own three of the most powerful structural drivers in semiconductors at once: silicon photonics for AI interconnect, LEO satellite RF, and silicon carbide power. It is the most idiosyncratic name in the European semi universe and the most misunderstood.

Twice a week, I will release deep dives into stocks and sectors that fit into the 6 themes that I see winning in the coming years and decades: AI & Technology, Electrification & Energy, Reshoring & Sovereignty, Healthcare & Longevity, China & Asia, Resilience & Quality.

Take advantage of this once in a generation opportunity to build long term wealth by investing in great stocks that will deliver returns for your portfolio for years to come.

After reading this article, you will understand why STM is a genuine AI hardware proxy hidden inside a cyclical analog wrapper, what the company actually does and how it transformed itself over the past decade, why three independent structural engines are converging on top of a clean cyclical recovery in automotive and industrial, and why, even after the stock has nearly quadrupled, the EPS story is only beginning, with the real debate now about positioning and sentiment rather than whether the demand exists.

In this article I go through:

STM’s business and how it reshaped itself into one of the most attractive EU Semi name.

The three structural growth drivers and why each is independently large enough to move group revenue.

How the manufacturing reshaping program and the mix change is creating incredible operating leverage and EPS growth in the next years.

Why the AWS engagement adds a fifth pillar to the engaged customer program base, de risking the concentration concern that historically capped the multiple.

Why the biggest risk after a 270% rally is no longer fundamental but a sentiment and positioning risk, as the market has recategorised STM as an AI and photonics name, a label that cuts both ways.

.svg — Wikipédia")

STMicroelectronics Investment Case

Table of content

Why now

Three independent vectors are converging in 2026:

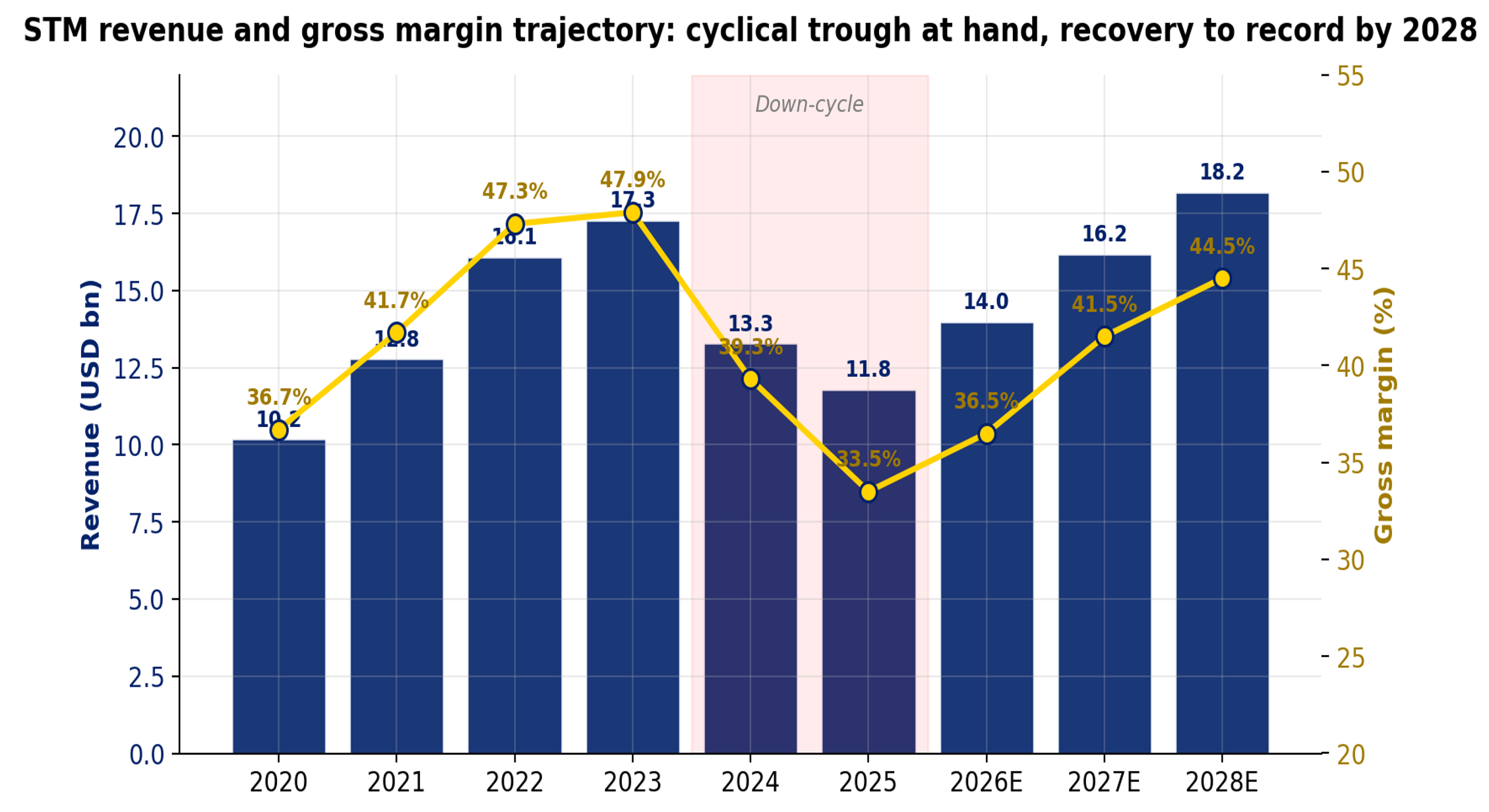

Cyclical: Q1 2026 marked the gross margin trough at 33.8% and revenue trough at $3.1bn. Industrial inventories normalised by mid 2026, automotive recovery resumed with Q1 bookings the highest since 2021, and management is guiding sequential revenue growth every quarter through year-end. Q2 mid-point guidance of $3.45bn (+11.6% sequentially) plus a Q4 2026 exit rate likely close to $4bn implies a clean inflection.

AI hardware re-rating: In February 2026 STM announced a multi-year, multi-bn$ strategic engagement with AWS covering silicon photonics PICs, BiCMOS EICs, MCUs and analog / power ICs. On June 2, 2026 the company firmed up the financial impact, raising 2026 data center revenue guidance to approximately $1bn (from “nicely above $500m”) and confirming a doubling to $2bn in 2027 (from “well above $1bn”). What was previously framed as “unconstrained demand” has now become committed guidance, the difference being confidence in the capacity ramp rather than the order book. Roughly two thirds of the revenue is optical (silicon photonics PICs, BiCMOS EICs, MCUs) at above-group gross margins (north of 40%), and one third is power and analog. Data center alone now contributes around 7% of group growth in 2027 and is set to reach 10 to 14% of group revenue by 2027 to 2028. STM remains the only large European IDM with a 300mm silicon photonics manufacturing capability at scale, a vertical integration that is structurally rare and structurally valuable.

Operational leverage: Capex peaked at 23.8% of sales in 2023 and is now in steady-state retreat toward 13 to 15%. Fab loading is improving, the manufacturing reshaping program (150mm fab closures, 300mm and 200mm SiC ramp) is executing on schedule, and management’s target operating model implies 44 to 46% gross margin and 22 to 24% operating margin on $18bn of revenue in 2027 to 2028. This is operating leverage worth more than 1,000bps of margin expansion over three years.

STM revenue and gross margin trajectory through the cycle. Source: Company reports, management guidance, Crack The Market estimates.

Business Description

STMicroelectronics is the second largest European semiconductor company by revenue (behind Infineon, which is the champion in power semis and AI power) and one of only a handful of Western integrated device manufacturers (IDMs) operating at scale.

It designs, manufactures and sells a broad portfolio of analog, mixed signal, power, microcontroller, sensor and RF chips. The company was created in 1987 from the combination of the Italian SGS Microelettronica and the non-military semiconductor business of the French Thomson group, and it remains today one of only two semiconductor businesses in the world where the French and Italian governments retain a meaningful equity stake.

STM’s place in the global semiconductor stack is best understood in context. As noted in my broader sector primer (Semiconductors: The most important sector in the world), the semi industry is split between leading-edge logic (TSMC, Samsung, Intel), memory (Samsung, SK Hynix, Micron), and a vast mature-node ecosystem of analog, power, microcontroller and sensor businesses that supply every other industry on earth. STM sits squarely in this mature node space, but with two specificities that distinguish it from the typical Texas Instruments/Analog Devices/Microchip cohort:

It is vertically integrated as an IDM: approximately 80% of its production is in-house (which explains the vast operational leverage and margin swings), with 300mm wafer fabs in Crolles (France) and Agrate (Italy), 200mm SiC vertical integration in Catania (Italy), back-end in Muar (Malaysia), Bouskoura (Morocco), Shenzhen (China) and Kirkop (Malta). This footprint is replicated by very few peers globally.

It controls the full SiC value chain end-to-end: from substrate (Norstel acquisition 2019) through epitaxy, front-end wafer fab, and module assembly. This is the broadest SiC vertical of any Western player, and the most important structural moat in the power semiconductor sub-industry over the next decade.

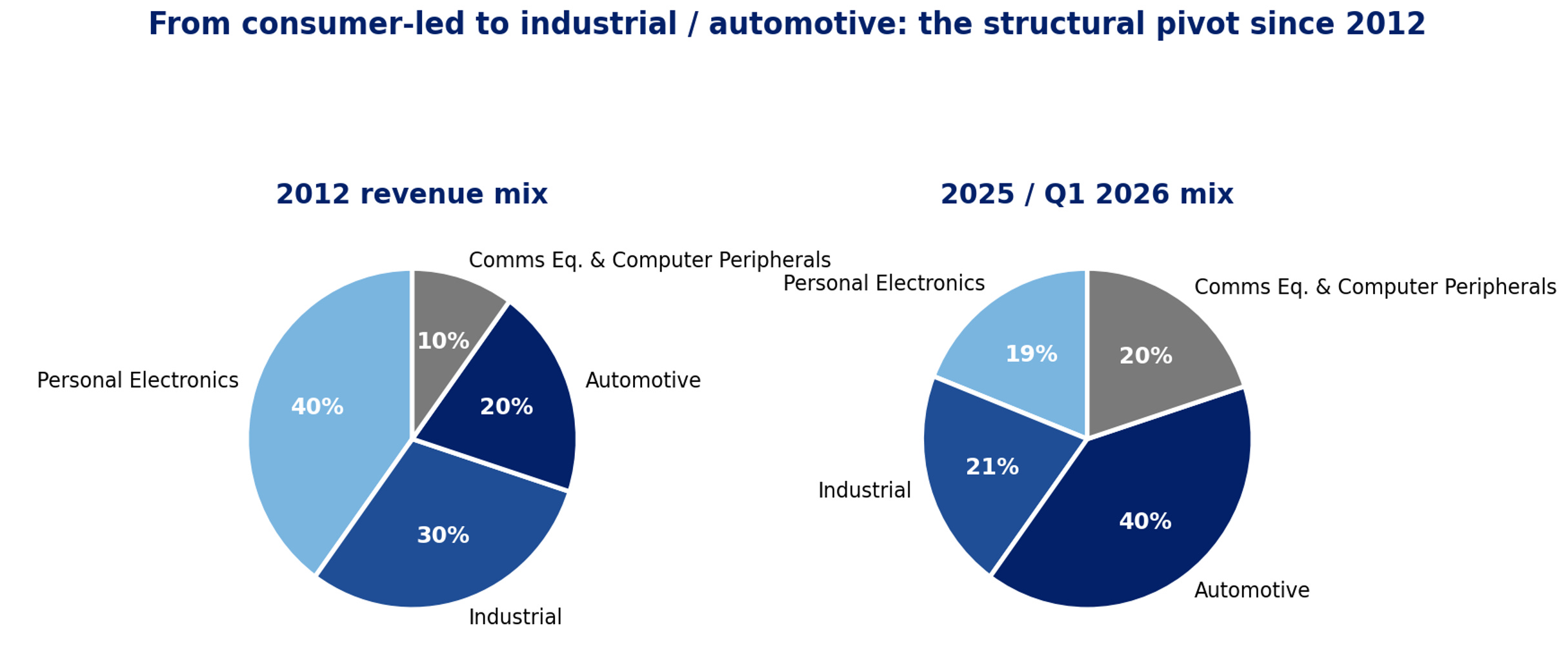

The structural pivot since 2012:

The most important fact about STM, and the one most consistently underappreciated by investors looking at the name through a US analog peer lens, is the degree of business transformation accomplished over the past 12 years.

In 2012, STM was a consumer electronics business in semiconductor clothing: 40% of revenue came from personal electronics (Nokia phones, smartphones, set-top boxes, NOR/NAND memory), 20% from automotive, 30% from industrial and 10% from communications equipment. The Nokia smartphone collapse alone wiped out approximately 25% of group revenue in the space of two years. The company’s market multiple in that period reflected its position as a low-quality, low-margin, cyclically pro-cyclical analog player.

Since then, management has executed one of the cleaner business reshapings in European semi history. Personal electronics dropped from 40% to 19% of revenue. Automotive doubled to 41%. Industrial held at 30%. The company exited NOR / NAND memory, mobile application processors, and the lowest-margin consumer sockets, and reinvested the capital into wide-bandgap power (SiC, GaN), automotive electrification, industrial MCUs (the STM32 ecosystem with 1.6m developers worldwide), MEMS sensors, and silicon photonics.

The financial result of that pivot is captured by the cycle peak in 2022 to 2023: $17.3bn of revenue, a 47.9% gross margin and a 27.5% operating margin. Those are best-in-class semi numbers for any European industrial business and a complete validation of the strategic shift.

The point of this investment case is not that STM is structurally a 47.9% gross margin business at its current scale (it is not, that print partly reflected post-Covid pricing tailwinds), but that the underlying earnings power is dramatically higher than the 2025 trough suggests, and that the demand drivers for the next leg of growth are now structural rather than cyclical.

End market mix transformation since 2012. Source: STM, Crack The Market.

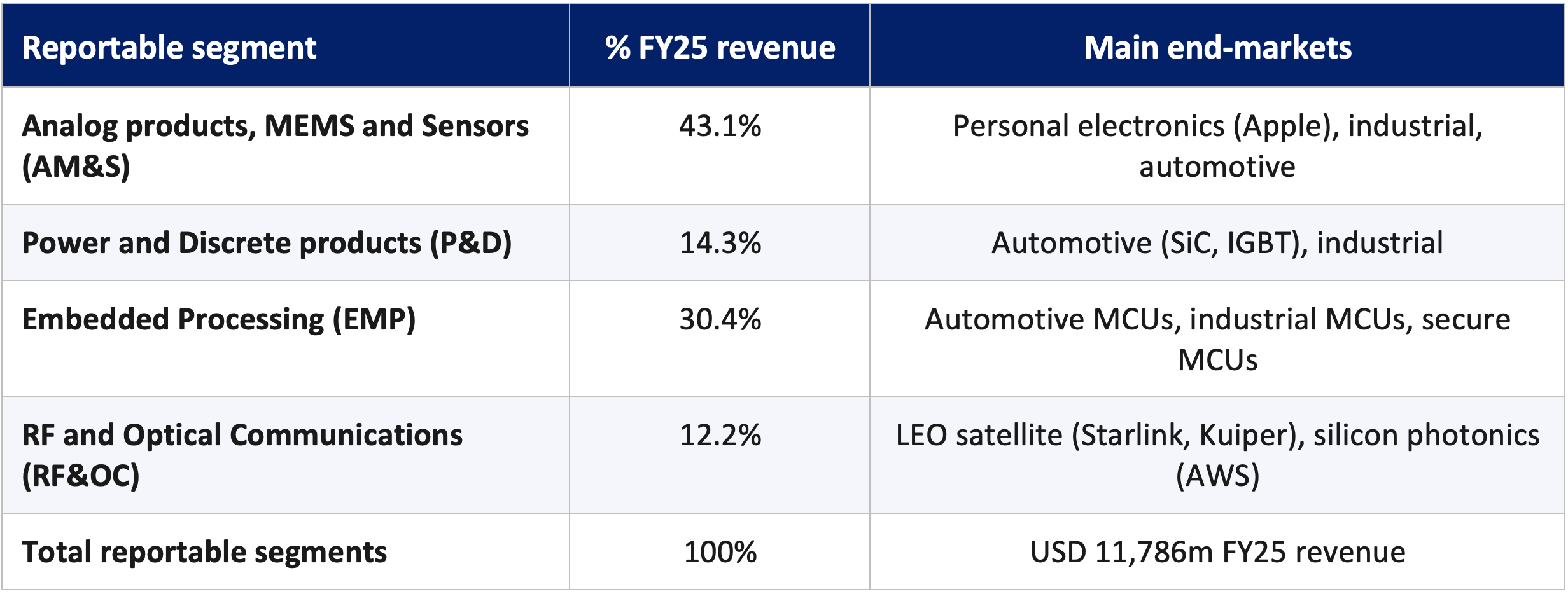

The four segments after the 2024 reorganisation:

Following the January 2024 reorganisation, STM reports two product groups and four reportable segments. The segment view captures the product / technology dimension, the end-market view (just above) captures the demand-side exposure. FY25 revenue of $11.8bn split as follows:

The two product groups are APMS (Analog, Power & Discrete, MEMS and Sensors) and MDRF (Microcontrollers, Digital ICs and RF products).

The reorganisation matters because it surfaces RF and Optical Communications as a distinct segment, which is where the AWS silicon photonics revenue, the BiCMOS satellite revenue, and the AI data center optical revenue all sit.

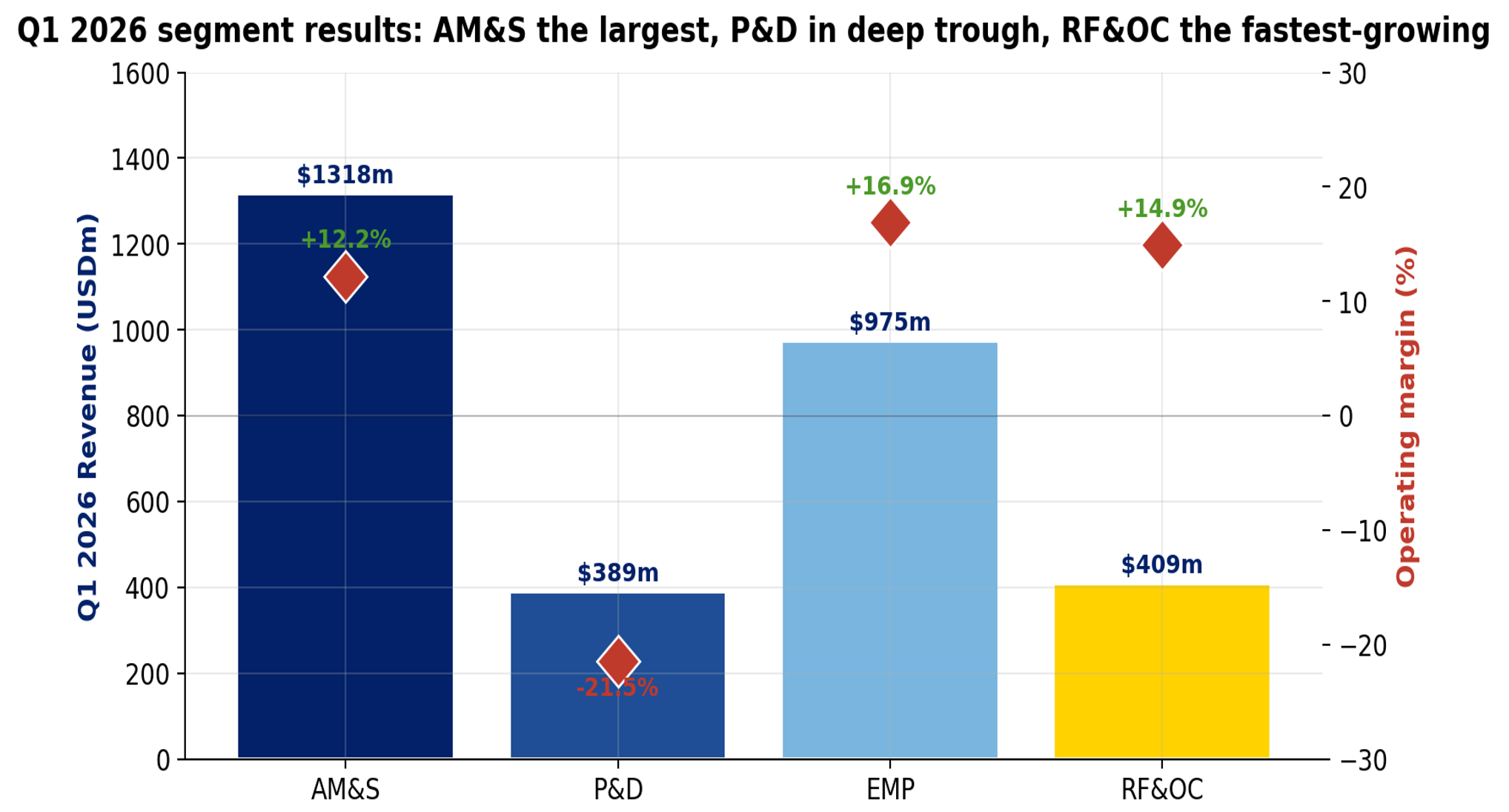

RF&OC grew 41% year on year in Q1 2026 and is the fastest-growing segment in the group. Expect this segment to roughly triple in revenue between 2025 and 2028.

Business segments breakdown:

Analog products, MEMS and Sensors (AM&S) division ($5.1bn sales, 43% of FY25 revenue):

AM&S is STM’s largest reportable segment and arguably the most strategically diverse. It pulls together three structurally different businesses under one P&L: general-purpose and application-specific analog ICs, MEMS motion and pressure sensors, and the imaging franchise (notably the Time-of-Flight and near-infrared CMOS image sensors that anchor the Apple Face ID program).

The division addresses both consumer (Apple is the anchor customer here) and industrial/automotive analog applications, which is why it is the most cyclically diverse of the four segments.

Breakdown by product family (approximate split based on company commentary and channel checks):

Imaging and 3D sensing (approximately 30% of division revenue): anchored by the Apple Face ID near-infrared CMOS image sensor and Time-of-Flight proximity detector, manufactured at Crolles on STM’s proprietary 140nm SOI process. From the iPhone 17 (Sep 2025), STM has also gained the meta-optics socket on the emitting side of the TrueDepth module, worth approximately $3 of incremental content per device. The under-display Face ID transition (likely from the iPhone 18 in 2026) is the next content step-up.

MEMS (approximately 35% of division revenue): inertial measurement units, accelerometers, gyroscopes, pressure sensors, microphones. Used across consumer (Apple AirPods, MacBook, iPad), automotive (airbag, ABS, electronic stability), and industrial (predictive maintenance, robotics). The Q1 2026 acquisition of NXP’s MEMS sensor business adds approximately $300m of annualised revenue and rebalances the MEMS mix from 41% personal electronics down to 30%, and from 24% automotive up to 37%, a clear positive on quality of earnings.

General-purpose and application-specific analog (approximately 35% of division revenue): op amps, voltage references, regulators, LDOs, eFuses, PMICs, real-time clocks, gate drivers. Sold across industrial (factory automation, energy infrastructure, medical) and personal electronics (display PMICs, wireless charging ICs).

Key customers: Apple (largest), the broader industrial distribution channel (Avnet, Arrow), Bosch and other Tier 1 automotive suppliers, Schneider Electric, ABB, and a long tail of consumer and industrial OEMs.

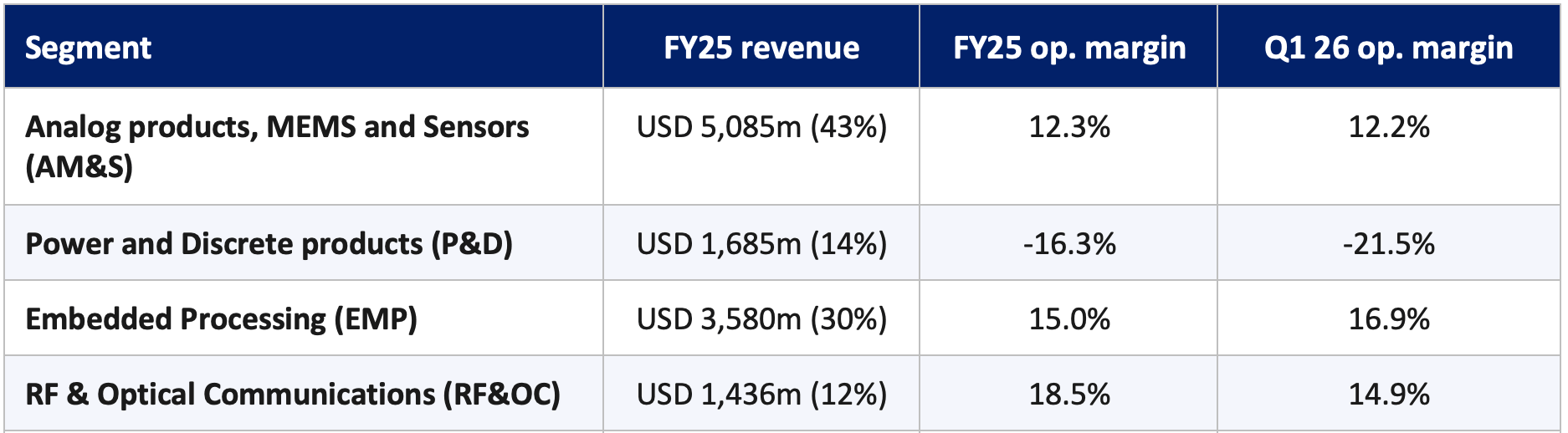

Cyclical position: AM&S is at the trough of its margin cycle (12.3% in FY25 versus 21.7% in 2023). The recovery in MEMS (industrial restock plus NXP acquisition mix shift), the Apple meta-optics content step-up, and the imaging mix improvement all point to a margin recovery toward 18-20% by 2027. The segment is structurally a mid-to-high teens operating margin business at cycle mid-point.

Power and Discrete products (P&D) division ($1.7bn sales, 14% of FY25 revenue):

P&D is the smallest segment by revenue but the most strategically important for the long-term thesis: it houses STM’s silicon carbide franchise, the #1 SiC business globally with 33% market share, alongside the legacy silicon power discrete portfolio (MOSFETs, IGBTs, GaN FETs, diodes, thyristors). The segment is in the deepest cyclical trough of the four, with FY25 operating margin at -16.3% and Q1 2026 at -21.5%, reflecting the combination of fab under-loading, Tesla SiC volume reset, and aggressive Chinese price pressure in silicon power.

Breakdown by product family:

Silicon carbide MOSFETs and modules (approximately 55% of division revenue): the franchise product. FY25 SiC revenue approximately $0.9bn, with Tesla still the largest customer but with rapid diversification to Chinese OEMs (BYD, Geely, Great Wall, Li Auto, XPeng). Gen 3 in production, Gen 4 ramping, Gen 5 in R&D. Target $5bn revenue and 30%+ market share by end of decade.

Silicon power MOSFETs and IGBTs (approximately 25% of division revenue): legacy silicon power portfolio. #2 in high-voltage silicon MOSFETs globally and #3 in discrete IGBTs. Faces structural Chinese competition (Nexperia / Wingtech, Silan, StarPower, CR Micro), which has weighed on pricing in 2024-2025.

GaN FETs, discretes, diodes, protection devices (approximately 20% of division revenue): the broader power discrete portfolio used across automotive 48V systems, industrial AC-DC, consumer fast charging, and increasingly AI data center 800V DC power conversion (the NVIDIA partnership announced in November 2025 covers 12V and 6V architectures for gigawatt-scale compute).

Key customers: Tesla (incumbent for SiC since 2017 Model 3 launch), Chinese auto OEMs via Sanan JV (production starting H2 2026), industrial distribution, NVIDIA (for AI data center power), and a broad base of automotive Tier 1 suppliers.

Cyclical position: this is where the largest absolute margin upside sits. Even a return to a 15% operating margin (the pre-Covid normalised level) on $2bn+ of FY27 revenue would add approximately $350-400m of operating profit versus the FY25 print of minus $275m. The Sanan JV ramp, the Catania mega-fab transition to 200mm, and the AI data center power ramp are the three vectors that re-rate P&D from the worst-margin segment to one of the better ones over 2026-2028.

Embedded Processing (EMP) division ($3.6bn sales, 30% of FY25 revenue):

EMP is the second-largest segment and the segment with arguably the strongest competitive moat: it houses the STM32 microcontroller ecosystem, which has been the global #1 in general-purpose MCUs since 2021 and which is supported by a developer community of 1.6m users worldwide. STM32 lifetime shipments have crossed 13bn units. The segment also includes the automotive MCU franchise (Stellar), the secure MCU business (used in eSIMs and banking), and the custom processing business (which is where the AWS engagement and other hyperscaler custom ASIC programs are reported).

Breakdown by product family:

General-purpose MCUs (STM32 family) (approximately 55% of division revenue): the flagship product. Used across industrial (factory automation, motor control, energy infrastructure), consumer (white goods, IoT devices), and increasingly edge AI (the STM32N6, launched in 2024, became the fastest STM product ever to reach $100m of revenue in 2025). Customer survey data shows 78% of customers maintained or grew their STM32 share in 2025, and 72% prefer to reuse the platform across product generations.

Automotive MCUs (Stellar) (approximately 25% of division revenue): launched in 2019, addresses the high-end automotive MCU market (domain controllers, ADAS, body control). STM has nearly doubled its automotive MCU market share from approximately 6% in 2019 to approximately 11% in 2023, now ranked #4 behind Infineon (29%), Renesas (23%), and NXP (22%). The market share gain trajectory is one of the cleaner secular tailwinds in the segment.

Secure MCUs and custom processing (approximately 20% of division revenue): eSIM, banking secure elements, the Mobileye foundry relationship (STM manufactures the EyeQ ADAS chips for Mobileye on a foundry basis), and the new AWS custom processing engagement. The latter is part of why this segment has structurally improving margins from 2026 onward.

Key customers: industrial distribution (the long tail of STM32 customers), automotive Tier 1 and OEMs (Stellar), Mobileye (foundry), AWS (custom processing), and the broader IoT and edge AI ecosystem.

Cyclical position: EMP delivered 15.0% operating margin in FY25 and 16.9% in Q1 2026, already running well above the AM&S and P&D levels. The path to 25%+ operating margin by 2027 depends on the industrial MCU recovery, continued automotive MCU share gains, and the AWS custom processing ramp. This is the highest-quality earnings segment in the group.

RF and Optical Communications (RF&OC) division ($1.4bn sales, 12% of FY25 revenue):

RF&OC is the smallest segment but the fastest growing and the most strategically transformative. It houses two of STM’s three structural growth engines: silicon photonics for AI data centers (anchored by the AWS partnership) and BiCMOS RF for LEO satellite (anchored by Starlink). The segment grew 33.9% year on year in Q1 2026 and is expected to roughly triple in revenue between 2025 and 2028, going from $1.4bn to $4bn+.

Breakdown by product family:

LEO satellite RF front-end modules (approximately 50% of division revenue): FY25 LEO revenue approximately $600m, going to approximately $1bn in FY26 (+50-60% yoy). Built on STM’s proprietary BiCMOS technology with K-band to V-band capability, packaged at Muar, Malaysia using panel-level packaging at up to 9m units per day. Starlink is the cornerstone customer with approximately 90% market share, Amazon Kuiper is the second customer ramping in 2026, with two more in the funnel. STM has shipped more than 5bn ICs to Starlink to date.

Silicon photonics and optical interconnect (approximately 25% of division revenue and rising fast): PIC100 platform entered high-volume production in Q1 2026, used by hyperscalers for 800Gbps and 1.6Tbps optical interconnect. AWS is the cornerstone hyperscaler partner (multi-year, multi-bn USD engagement announced February 2026). STM also supplies optical components for Chinese AI data centers via pluggable transceiver makers. >30% market share in EICs (electronic ICs on BiCMOS), targeting similar in PICs.

Other RF and custom ASICs (approximately 25% of division revenue): legacy RF business including ADAS-related custom ASICs (the company has been gradually disengaging from lower-margin networking ASICs), satellite ground gateway products, and other specialty RF.

Key customers: SpaceX (Starlink), Amazon (Kuiper and AWS), Innolight and other Chinese pluggable transceiver vendors, plus an emerging hyperscaler funnel.

Cyclical position: RF&OC delivered 18.5% operating margin in FY25 and is expected to expand toward 25%+ by 2028 as the silicon photonics mix increases (management has confirmed silicon photonics margins are above group average) and as the LEO franchise scales. This segment, more than any other, is the reason the stock has nearly quadrupled from the 2025 trough.

Q1 2026 segment results. AM&S the largest, P&D in deep margin trough, RF&OC the fastest-growing. Source: STM, Crack The Market.

How to think about segment evolution 2025 to 2028:

The four-segment structure provides a useful lens on where the operational leverage comes from over the next three years.

AM&S delivers stable mid-teens margins with modest revenue growth.

P&D is the deepest recovery story, from a negative margin in 2025 to potentially 15-20% by 2027-2028 as SiC volume normalises and fab loading recovers.

EMP is the highest-quality compounder, with the STM32 ecosystem providing the moat and the AWS custom processing the optionality.

RF&OC is the structural growth engine, tripling in revenue and contributing the bulk of the incremental margin expansion at the group level.

Importantly, the company manages on a consolidated basis but discloses segment-level operating margins, which means the cyclical trough versus structural growth dynamics are visible quarter-by-quarter.

The trajectory toward the management 2027 to 2028 financial model ($18bn revenue, 44-46% gross margin, 22-24% operating margin) implies an average segment margin of approximately 20%, which is roughly the segment-weighted average of EMP and RF&OC running at 25%+ and AM&S and P&D running at 15-18%.