Cameco: The Western Nuclear Champion

The only Western company that captures economic rent at every stage of the nuclear fuel cycle, at the inflection of a multi-decade contracting supercycle

Welcome to the 67th investment case, 55th Resilience & Quality, 42nd Reshoring & Sovereignty, 23rd Electrification & Energy idea on Crack the Market (and the most comprehensive Cameco investment case you will find online)! Join me as I dissect the only Western company that owns the entire nuclear fuel cycle, a Tier-1 uranium producer whose contract book is being repriced from $66 toward $115+/lb, and whose 49% stake in Westinghouse has just been chosen by the US government as the strategic vehicle for an $80bn AP1000 build-out with a credible path to a $30bn IPO before January 2029.

Before reading this deep dive

This piece compresses the uranium and nuclear sector primer because Crack The Market subscribers have already received four substantial pieces on the topic. Read or re-read these first, they are the macro substrate of the Cameco thesis.

Uranium: Entering a Nuclear Powered Supercycle (Jan 2026): the full uranium primer. Value chain, fuel cycle mechanics, contracting structure, supply concentration, and the structural deficit math (20m lb today widening to >120m lb by 2040).

The Nuclear Renaissance (Mar 2026): why AI, electrification and geopolitics are forcing a global return to nuclear, the COP28 tripling pledge endorsed by 38 countries, and the demand-side inflection.

The Worst Energy Crisis In History (Mar 2026): the Middle East shock, the Actuarial Blockade, and why energy infrastructure is now the primary military target. This is the macro accelerant under nuclear new build.

The Crisis That Will Rewire the Energy System (Apr 2026): why Europe and Asia will suffer most, and what the new energy system looks like once sovereignty replaces market economics as the organising principle.

Why Nuclear Power Is No Longer Optional (Apr 2026): the synthesis: nuclear shifts from a climate-driven choice to a national security imperative.

Twice a week, I release deep dives into stocks and sectors that fit into the 6 themes that I see winning in the coming years and decades: AI & Technology, Electrification & Energy, Reshoring & Sovereignty, Healthcare & Longevity, China & Asia, Resilience & Quality.

Take advantage of this once in a generation opportunity to build long term wealth by investing in great stocks that will deliver returns for your portfolio for years to come.

After reading this article, you will understand why Cameco is the cleanest Western expression of the Nuclear Renaissance, why the long-term price indicator at $91.50/lb is structurally undercounting where the contracting market actually clears today, why the Westinghouse stake is one of the most underappreciated free options in the global energy complex, and why an integrated mining-conversion-enrichment-OEM platform anchored in the most stable jurisdictions on Earth deserves to be valued on its 2028-2030 earnings power rather than its 2026 optical multiple.

In this article I go through:

Cameco’s business and how it dominates the Western nuclear fuel cycle across mining, conversion, enrichment optionality and reactor services.

Why the uranium contracting cycle is structurally early, not late, and how the shift from base-escalated to market-related contracts re-rates Cameco’s realised price through the decade.

How the Westinghouse stake transforms Cameco from a high-quality uranium producer into a fully integrated Western nuclear champion, and why the $80bn DOC framework is a step-function value creator.

How the sovereignty premium for Western pounds is widening as Russian enrichment, Russian transit and Russian-influenced supply are progressively excluded from the Western fuel cycle.

Why the stock compounds in every plausible scenario because the contracted Tier-1 production base generates cash no matter where spot trades in any given quarter.

Cameco Investment Case

Table of content

Business Description

Cameco is the cleanest, deepest and most strategically positioned Western exposure to the Nuclear Renaissance:

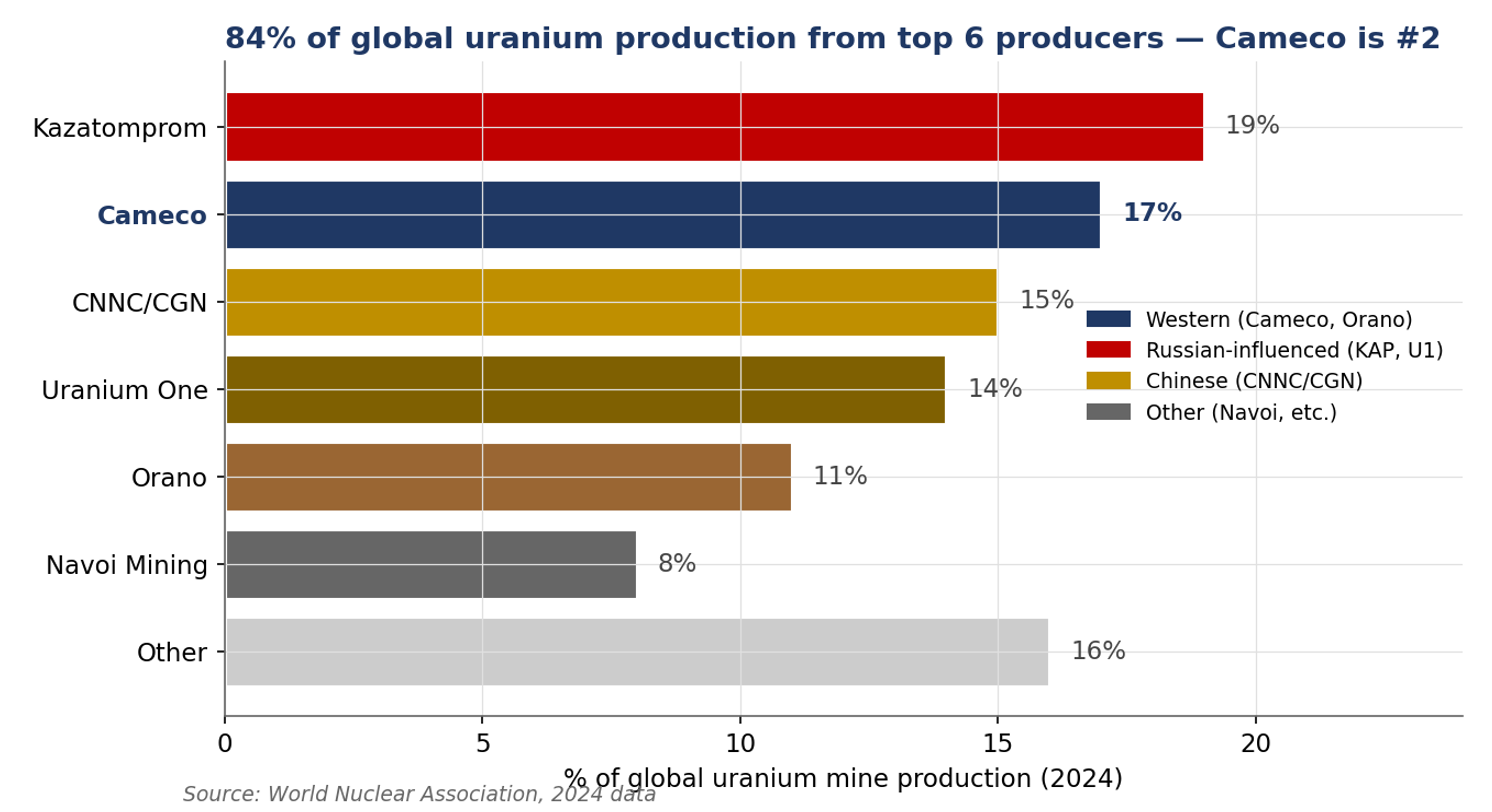

Cameco is the world’s second largest uranium producer (17% of global mine supply). It is a tier-one producer based in Saskatchewan (Canada).

The world’s largest commercial conversion footprint at Port Hope.

The 49% stake in Westinghouse Electric Company, the OEM of the AP1000 reactor at the heart of the global new build pipeline

The 49% partner in Global Laser Enrichment, the only non-centrifuge enrichment technology in late-stage development.

No other Western company offers integrated exposure across all four layers of the front end of the nuclear fuel cycle and the OEM reactor services layer.

Almost every megatrend that I cover on Crack The Market covers converges on this single equity:

AI infrastructure needs baseload power that wind and solar cannot deliver.

Reshoring needs sovereign energy supply chains that exclude Russian and Russian-influenced capacity.

Resilience and quality investors need cash-flowing Tier-1 assets in stable jurisdictions, not pre-revenue developers.

China’s structural absorption of marginal global uranium supply creates a Western contracting squeeze.

The Worst Energy Crisis In History has accelerated the transition from cost optimisation to security maximisation in energy procurement.

Cameco sits at the intersection of all of it, and unlike many “thematic” names, it generates real, contracted, near-term cash flow at the same time.

Segments and the integrated nuclear fuel platform - Cameco reports three segments: Uranium, Fuel Services, and Westinghouse (equity-accounted):

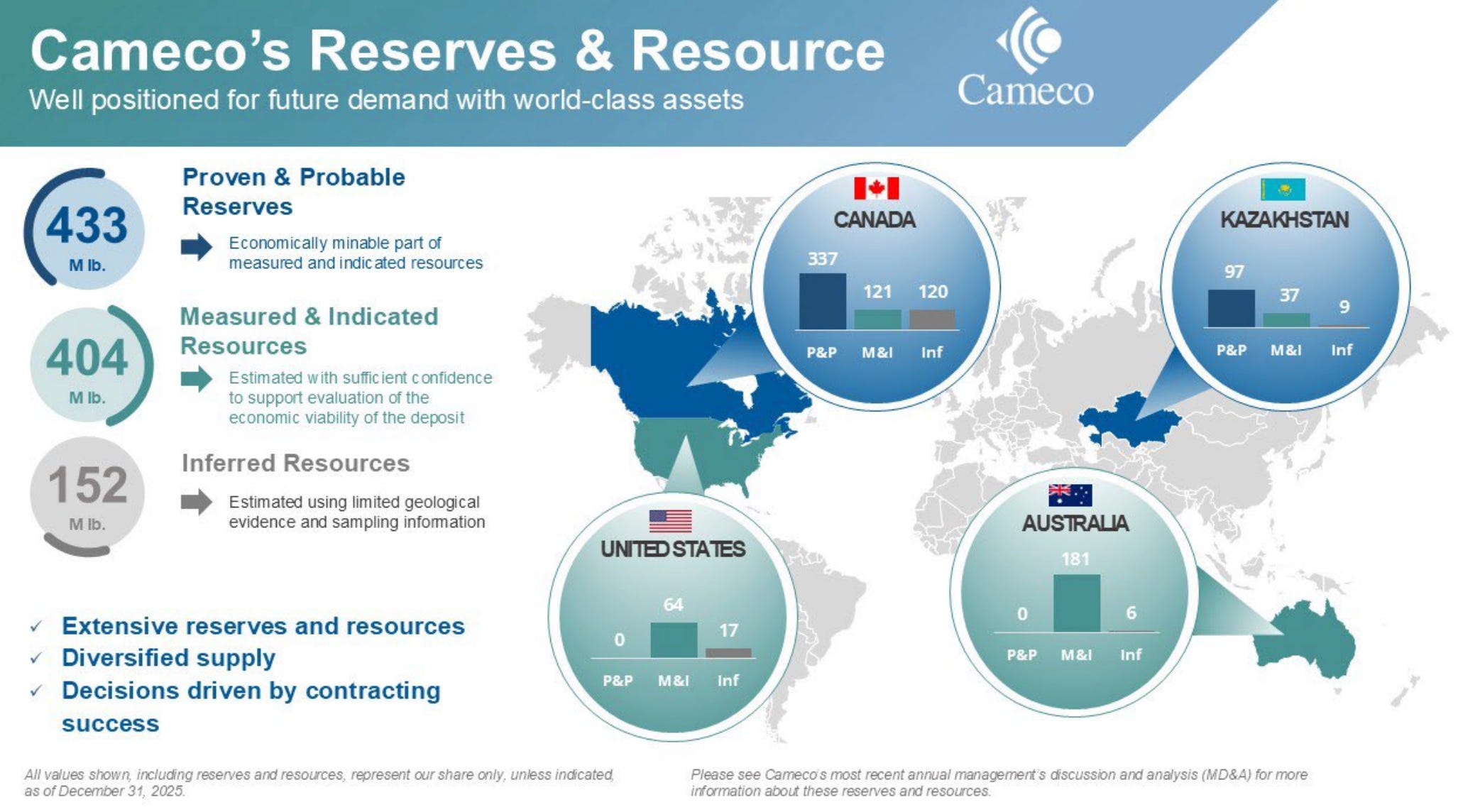

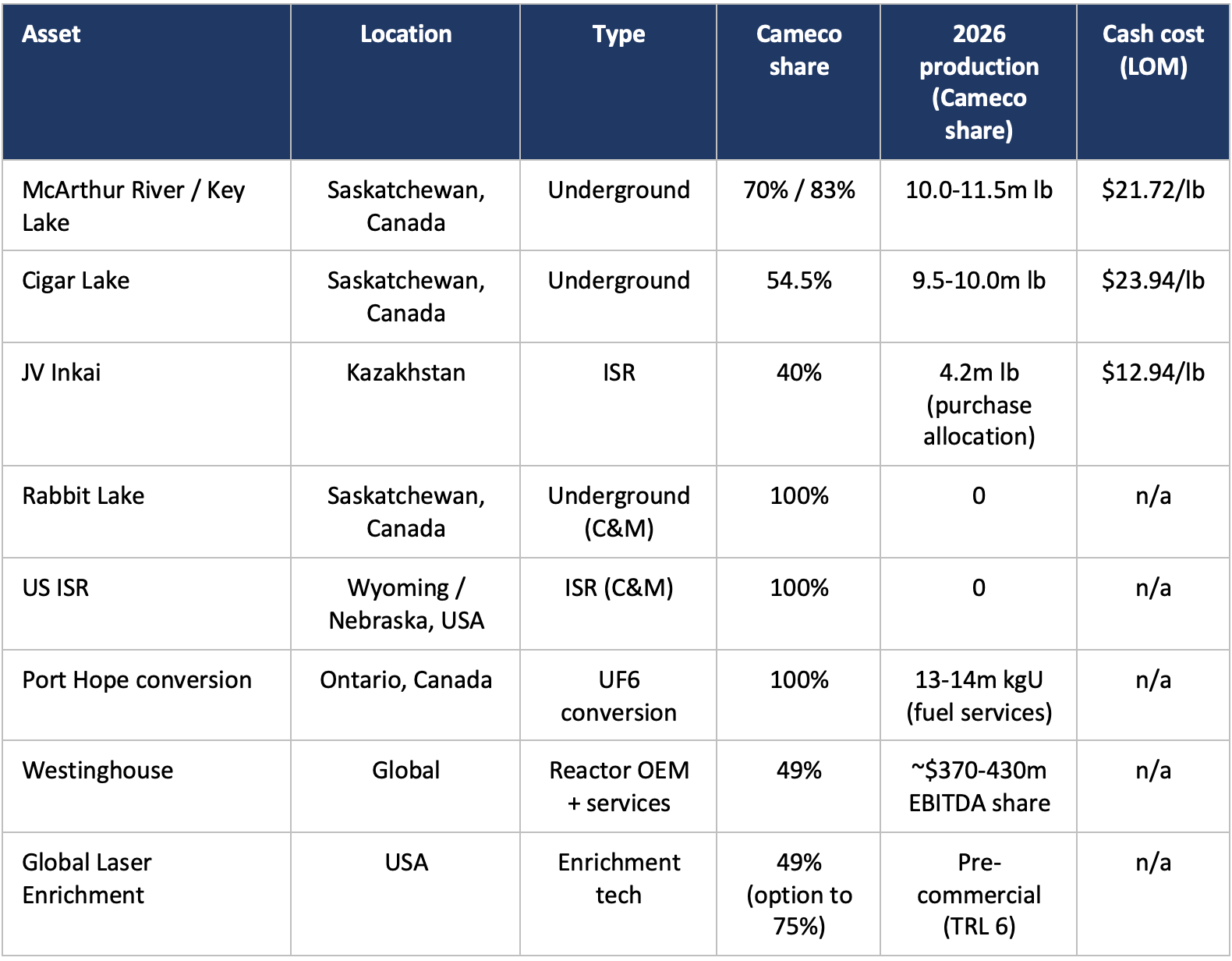

The uranium business is the core: it includes the Tier-1 McArthur River/Key Lake mill complex and Cigar Lake mine in the Athabasca Basin of northern Saskatchewan, plus the 40% interest in JV Inkai in Kazakhstan, which is operated by joint venture partner Kazatomprom. Tier-2 assets (Rabbit Lake in Saskatchewan, US ISR operations in Wyoming and Nebraska) remain in care and maintenance, with care and maintenance costs of $62-67m planned for 2026. In 2026, Cameco expects to produce 19.5-21.5m lb U3O8 (its share) from owned and operated properties, take delivery of 4.2m lb from its share of JV Inkai production, and sell 29-32m lb at an average realised price of $85-89/lb. Uranium revenue is guided to $2,540-2,730m.

The Fuel Services segment captures conversion of U3O8 to UF6 and UO2 at the Port Hope facility in Ontario plus heavy-water reactor fuel bundle fabrication at Cameco Fuel Manufacturing in Cobourg, Ontario. In 2026, Fuel services produces 13-14m kgU at an average unit cost of sales of $31.50-33.50/kgU.

Westinghouse (the nuclear OEM business) is held through a 49/51 partnership with Brookfield Renewable, acquired in November 2023 for $7.9bn enterprise value (Cameco’s share: roughly $2.2bn equity). Cameco’s share of Westinghouse adjusted EBITDA is guided at $370-430m for 2026, with the back half of the year heavily weighted given Westinghouse’s contractual cadence.

Asset quality - the Tier-1 moat:

Cameco’s asset moat is geological and not replicable. The Athabasca Basin in northern Saskatchewan hosts the world’s highest-grade uranium deposits, with ore grades 10-100x the global average:

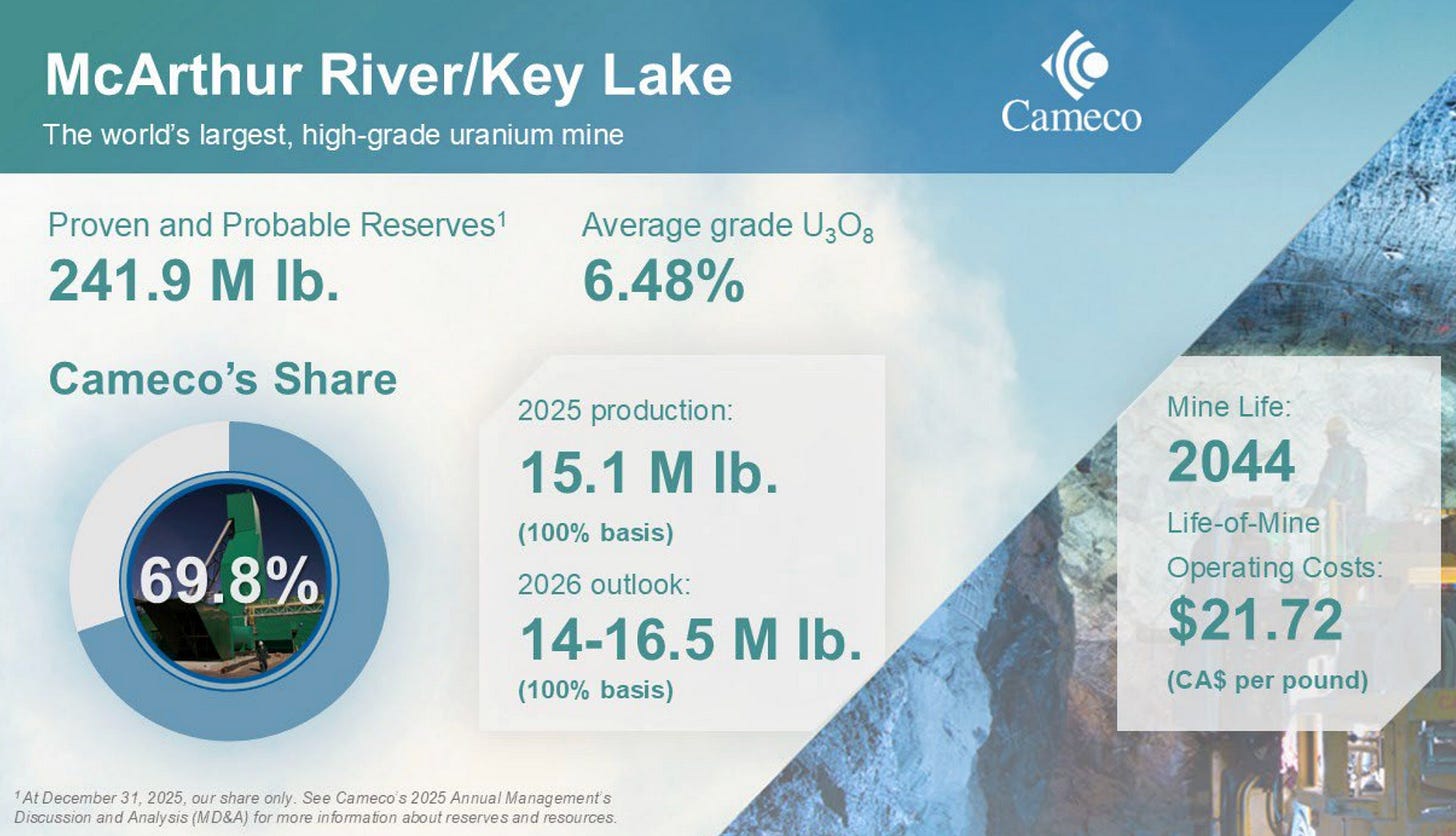

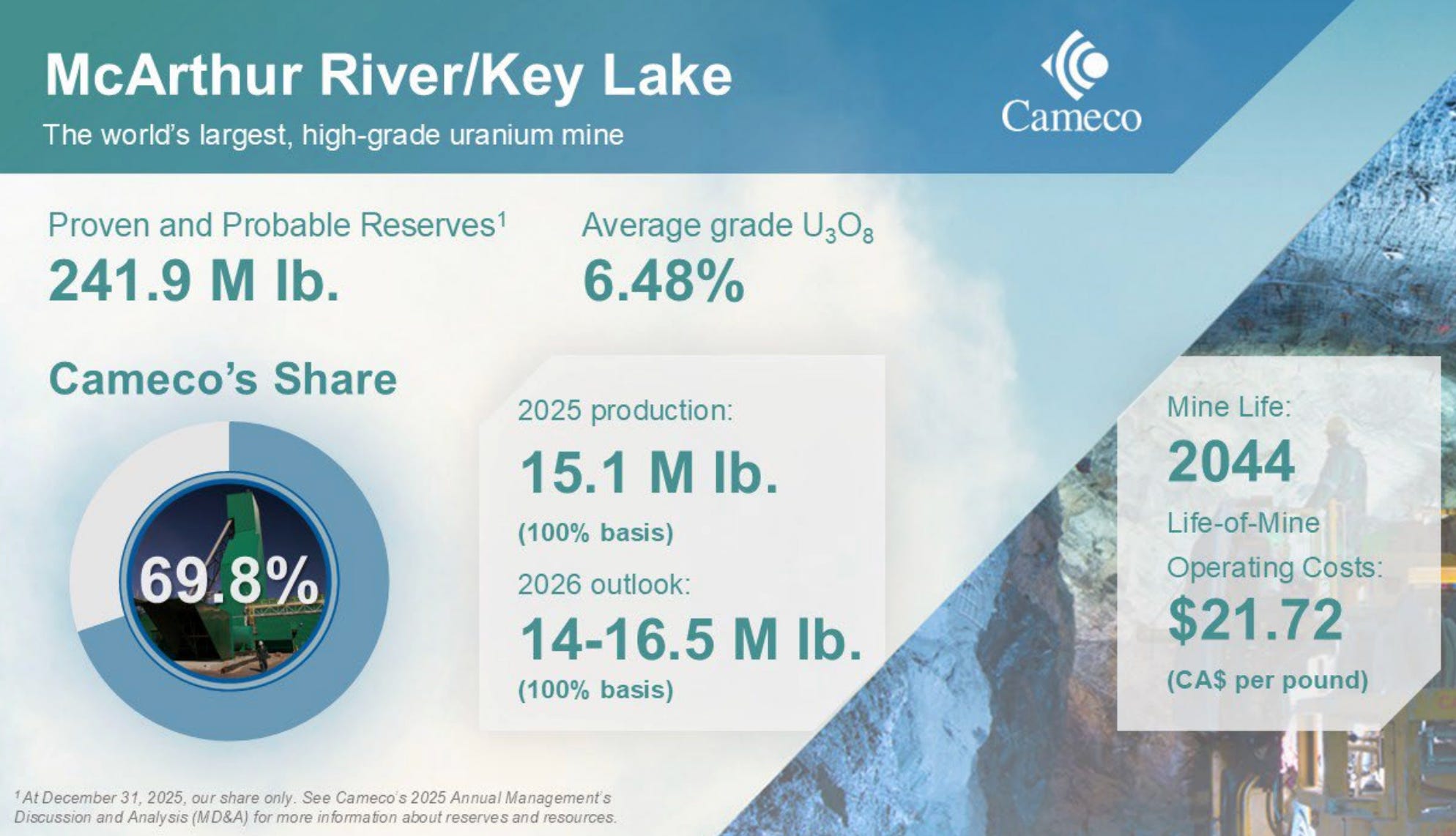

McArthur River, the world’s largest high-grade uranium mine, has 390m lb of resource and reserve supporting annual production of up to 18m lb.

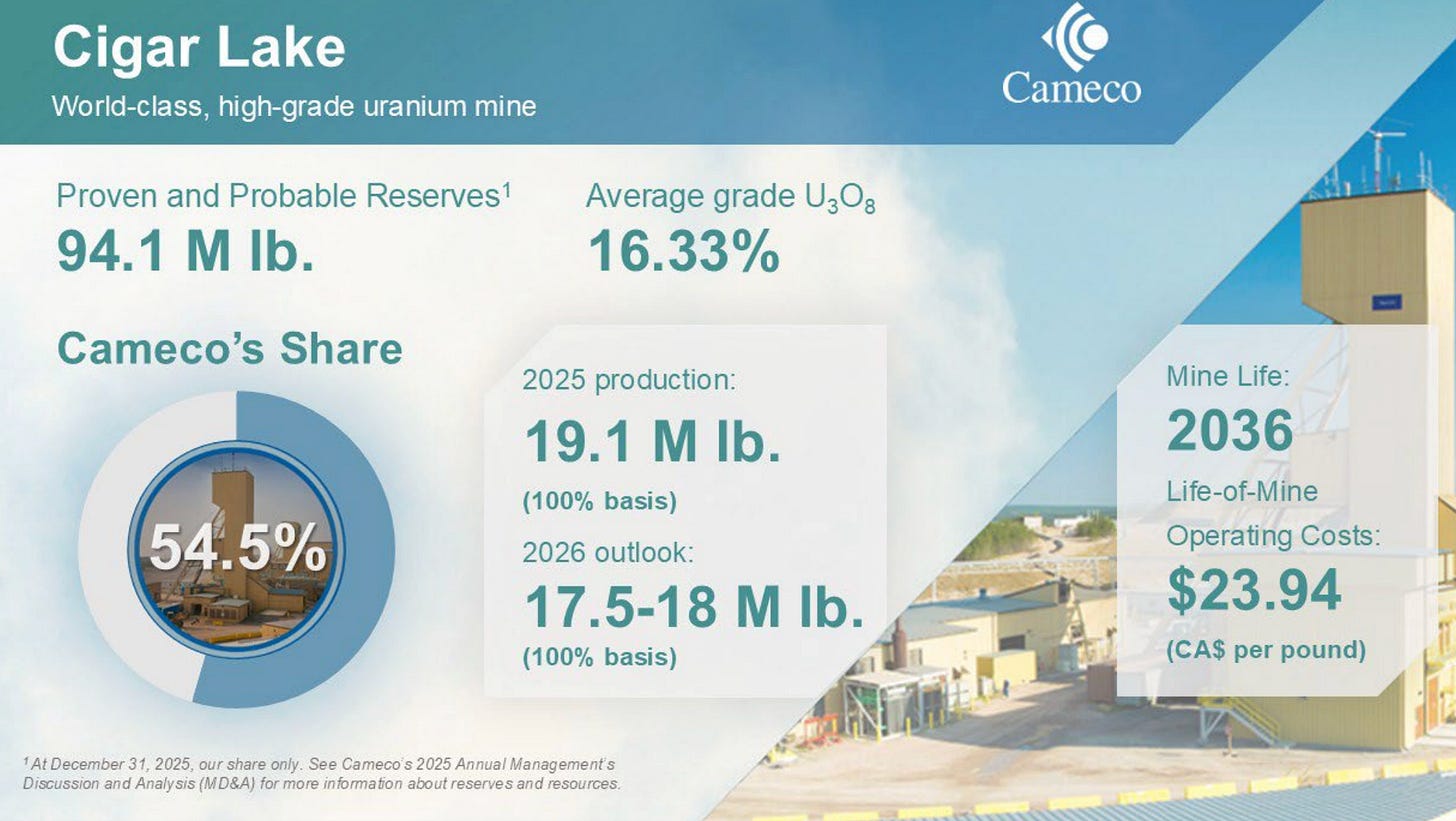

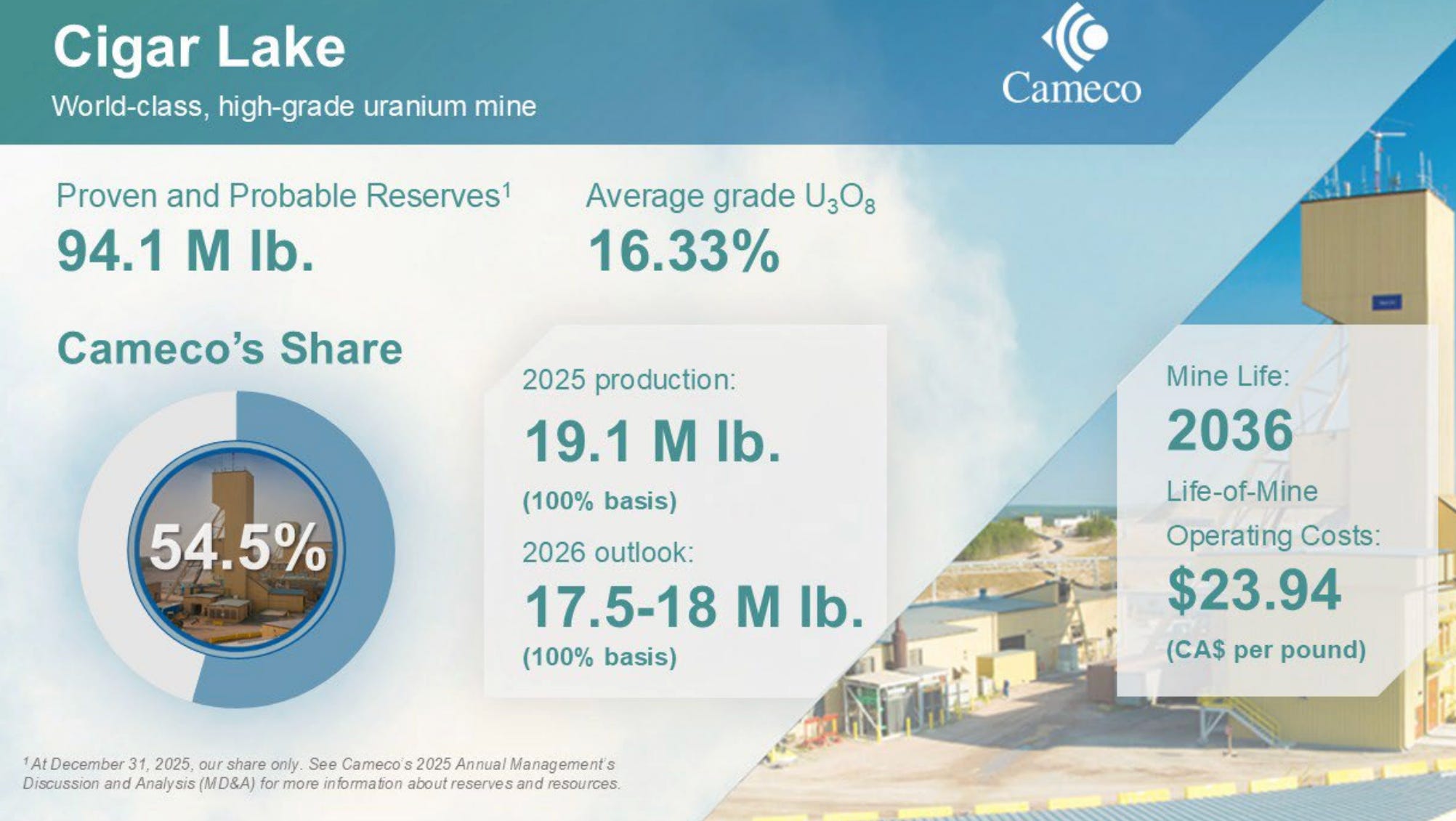

Cigar Lake, a JV with Orano (50.025% Cameco / 37.1% Orano / 12.875% Idemitsu), is the world’s second-highest grade uranium mine, with 250m lb of resource supporting another 14 year mine life from current production.

The Q1 2026 reported life-of-mine cash operating costs are $21.72/lb at McArthur River/Key Lake and $23.94/lb at Cigar Lake, numbers that sit firmly in the first quartile of the global uranium cost curve and that make these assets profitable at virtually any uranium price regime contemplated in the next decade.

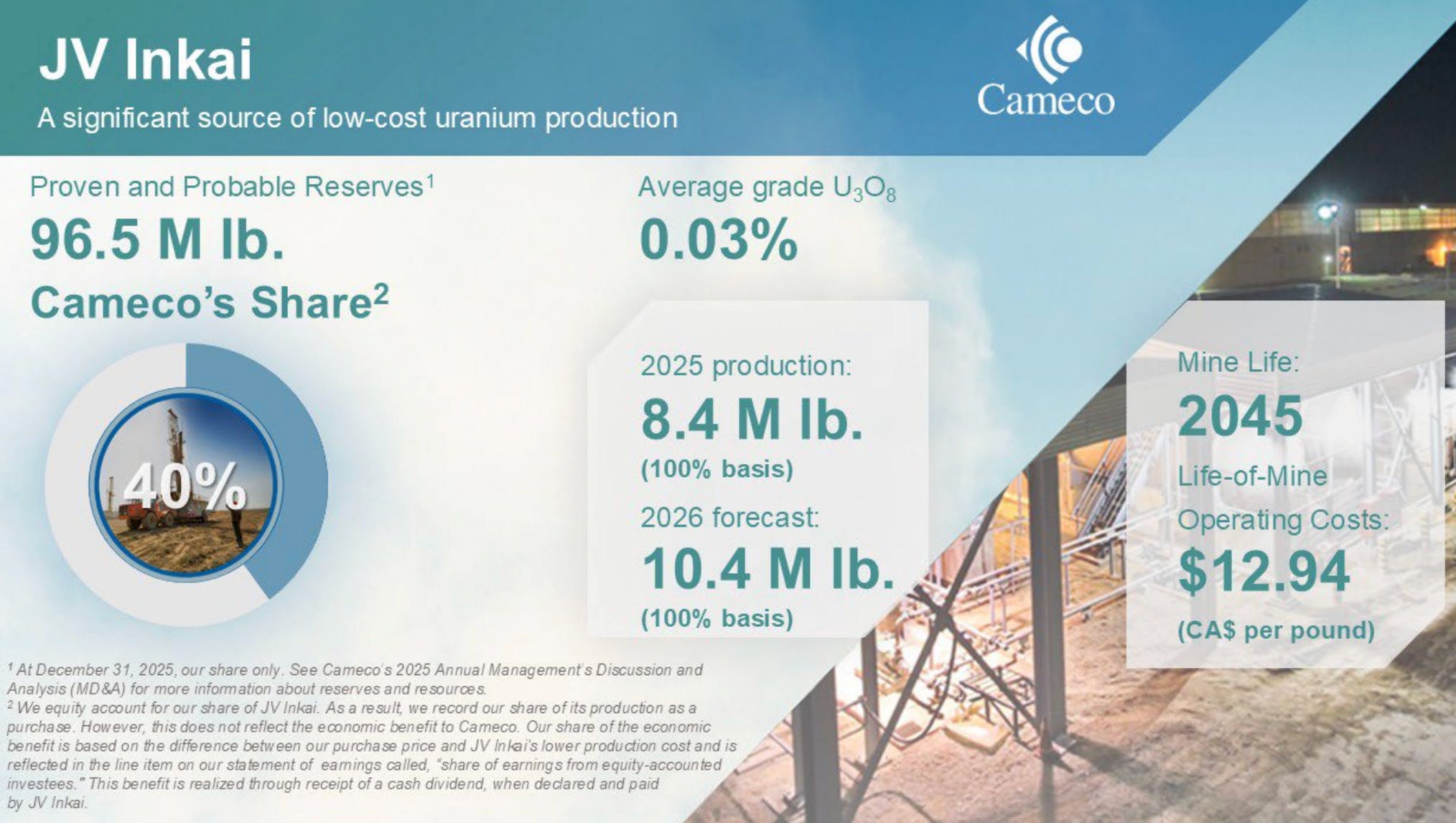

JV Inkai is structurally different but strategically valuable:

It is an in-situ recovery (ISR) operation in southern Kazakhstan, jointly owned with Kazatomprom (60%), producing approximately 10.4m lb (100% basis) in 2026 with Cameco’s share at 4.2m lb.

Inkai’s life-of-mine cash cost is $12.94/lb, the lowest in the Cameco portfolio, but the geopolitical and logistics risk is real: Russian transit issues since 2022 have forced the Trans-Caspian routing to grow in importance, and sulfuric acid availability remains a recurring concern across the Kazakh ISR base. Cameco’s management has been candid that Inkai is treated as one supply lever among several and not as a production guide, the company sources its sales commitments from a mix of production, inventory, market purchases, and product loans (4.1m lb of U3O8 currently drawn against 6.8m lb of standby loan capacity).

Cameco’s asset map (2026)

Cameco is the #2 global uranium producer and the #1 Western producer. The combined Western share (Cameco + Orano) is 28%, against 33% for Russian-influenced (Kazatomprom + Uranium One) and 15% for Chinese (CNNC/CGN) capacity. The Western producers operate in stable jurisdictions with high regulatory barriers to entry, which is the geological and political moat that underwrites the Cameco premium.

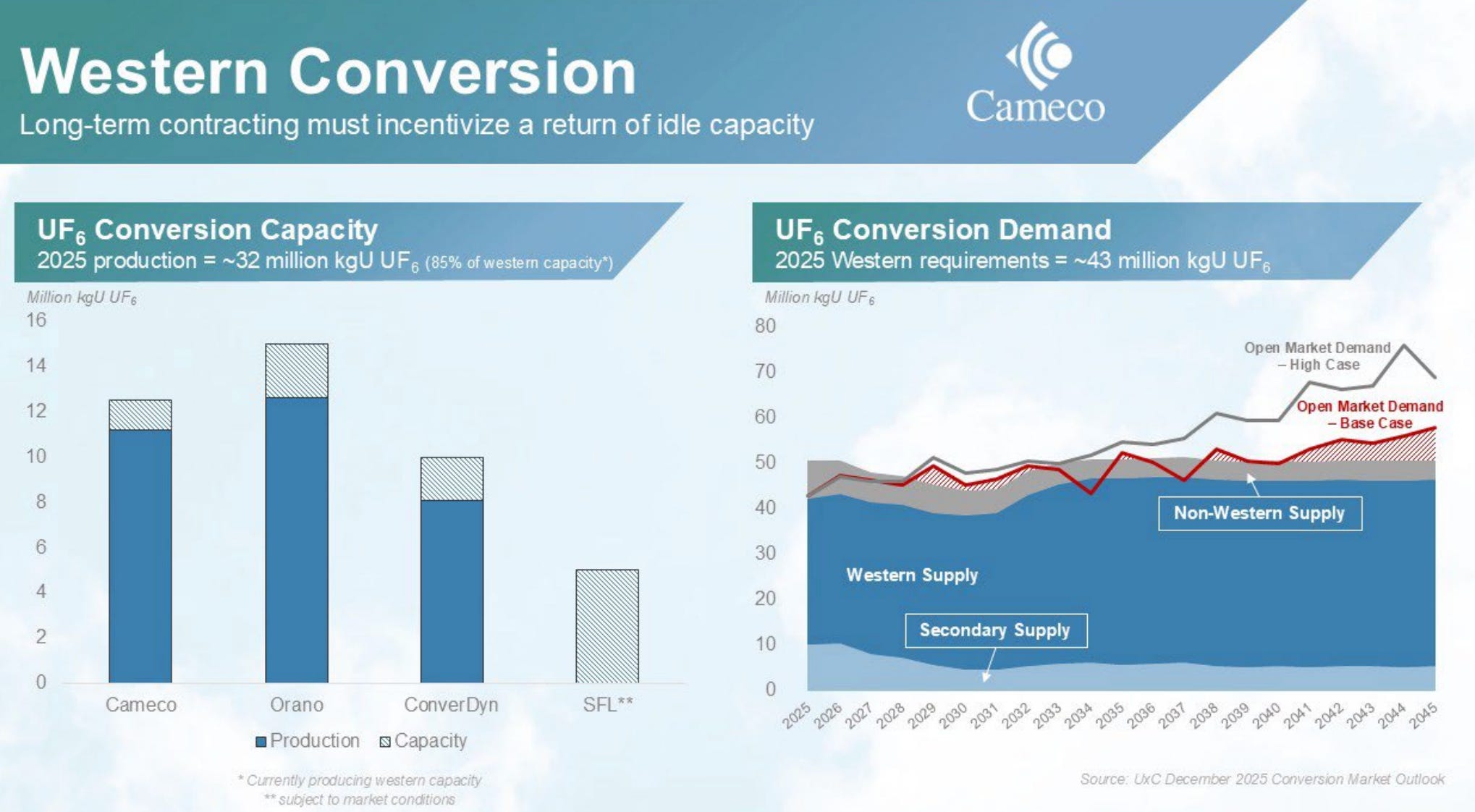

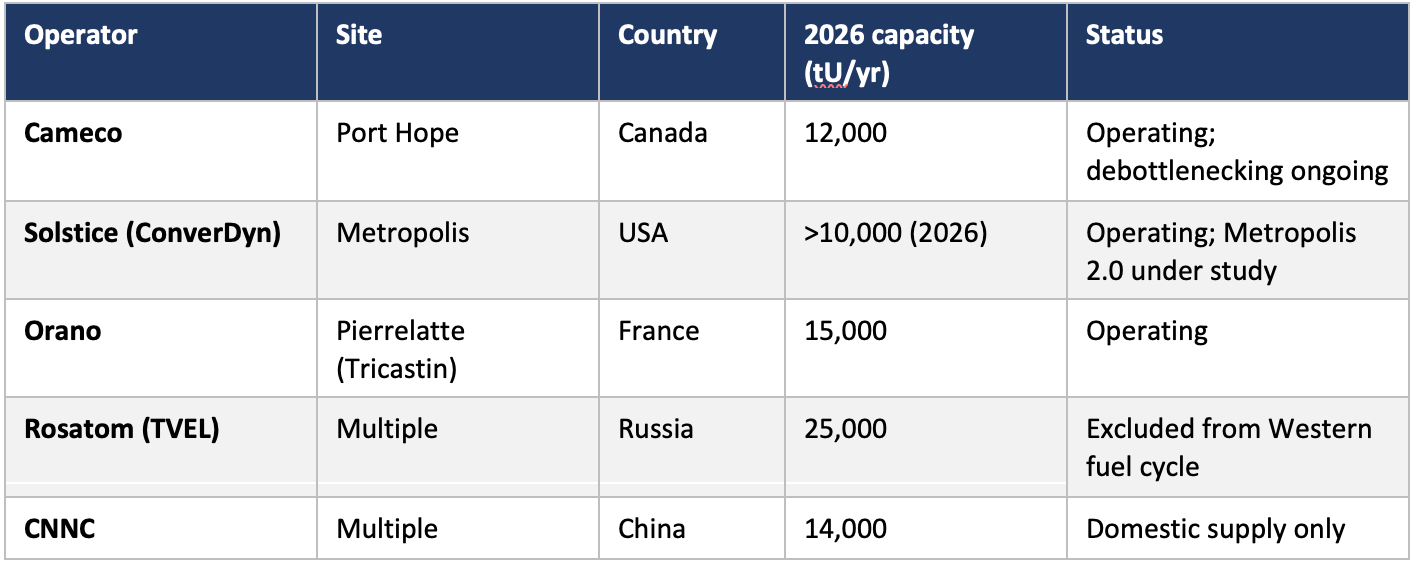

The conversion choke point - Port Hope is Cameco’s most underappreciated asset:

UF6 conversion is the second step of the nuclear fuel cycle (after mining and milling, before enrichment), and the Western capacity stack is concentrated in just three commercial operators: Cameco at Port Hope (Canada), Solstice Advanced Materials (formerly Honeywell ConverDyn) at Metropolis (USA), and Orano at Pierrelatte (France). Russia’s Rosatom retains substantial conversion capacity but has been progressively excluded from Western fuel cycles since 2022.

The Q1 2026 spot conversion price was $62.50/kgU and the long-term price $55.25/kgU, down from the post-Ukraine war peak of $97/kgU but still 5-6x the pre-2022 normal.

This is a structurally tight market, and Cameco’s Port Hope licensed capacity (which is being progressively debottlenecked toward a 12,000 t/yr UF6 run-rate) is a multi-decade asset that throws off high-margin cash and acts as a strategic gateway for the company’s contract negotiations with utilities seeking integrated front-end packages.

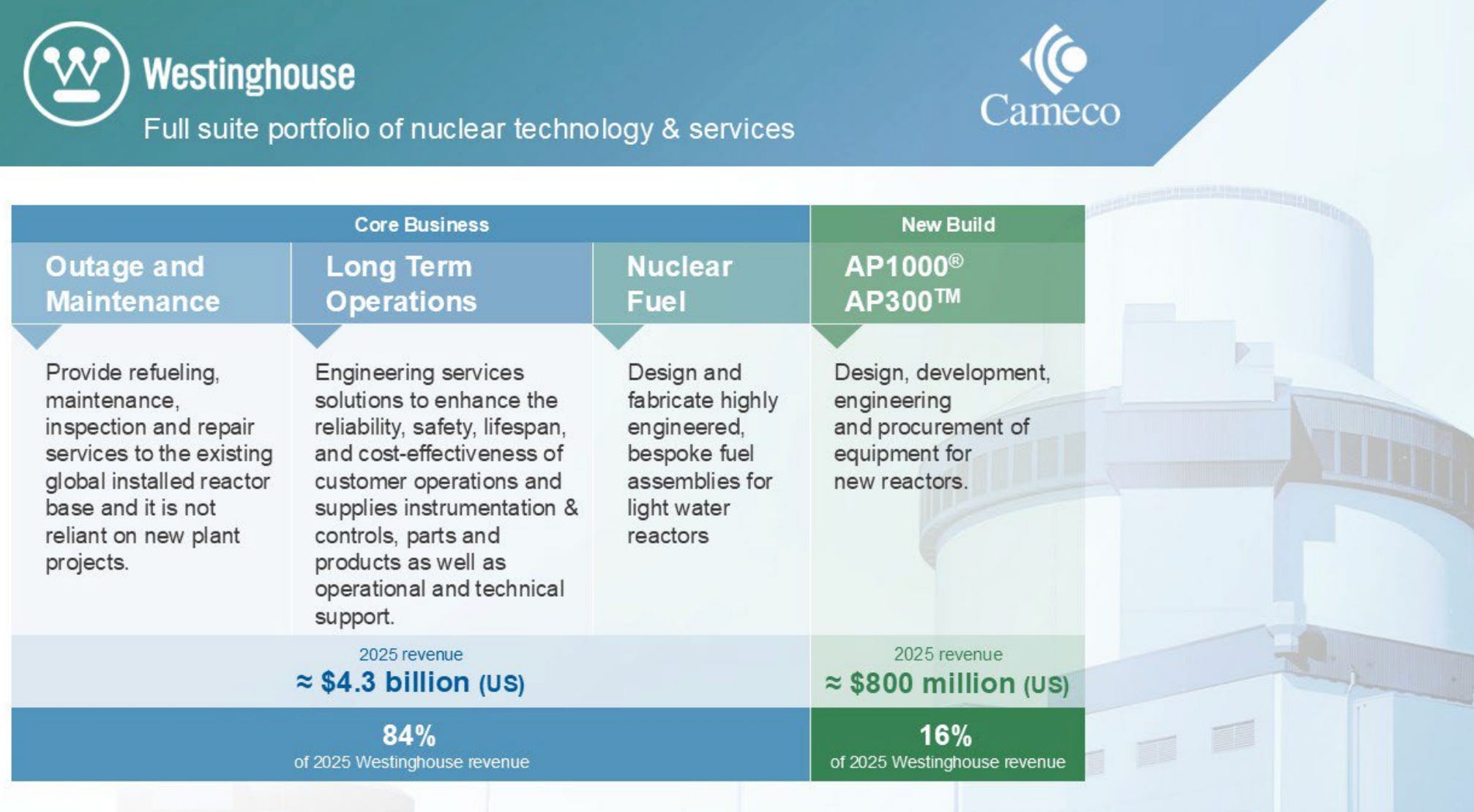

Westinghouse - the 49% optionality engine:

Cameco and Brookfield closed the Westinghouse acquisition in November 2023 at $7.9bn enterprise value, financed with a mix of equity and Cameco-issued debt:

At the time, the deal was met with significant scepticism about Westinghouse’s legacy issues, the price paid, and the fit with Cameco’s commodity DNA.

Two years later, the strategic logic looks materially better.

Westinghouse is the only Western reactor OEM with a proven, NRC-licensed Gen III+ design (the AP1000).

A global installed base of approximately 200 reactors built under Westinghouse or Westinghouse-licensed designs (roughly half the world’s operating fleet).

A recurring services and fuel fabrication business that generates predictable cash flow regardless of new build cadence.

The 2024 baseline was $4.3bn revenue and $483m adjusted EBITDA. Management guides to 6-10% EBITDA CAGR over five years on the existing services book alone, with new build revenue treated as upside optionality.

In October 2025, the US administration announced an $80bn strategic partnership with Cameco, Brookfield and Westinghouse to underwrite the build-out of AP1000 reactors in the United States, structured as a Department of Commerce framework with a participation interest mechanism that allows the US government to capture up to 8% of Westinghouse’s equity if two vesting conditions are met:

A minimum $80bn deployed against AP1000 final investment decisions

A Westinghouse equity value reaches $30bn before January 2029, verified by an underwritten IPO valuation.

This is the framework that has re-rated the Westinghouse stake from a quietly accretive M&A deal to potentially the largest single source of value creation in the Cameco story over the next 36 months.